Darden Restaurants released its full 2QFY13 results this morning. There were few surprises in the press release but the earnings call made for some interesting listening.

“There will be more rejoicing in heaven over one sinner who repents than over ninety-nine righteous persons who do not need to repent.

-Luke 15:7

First Thing’s First

The big news from this morning’s earnings call is that the company is cutting its capex budget for FY14 by ~10%, driven mainly by a reduction in new unit growth. FY13 new unit growth is now expected to be 100 units, versus prior guidance of 100-110. The reduction in capex is being carried out to ensure the maintenance of “solid debt metrics that preserve our investment grade credit profile”.

The company is still guiding to $1 billion in operating cash flow this year. This will be helped by working capital turning to a source, from a use, of cash this year versus last year. It should also be a source next year. We believe it could be difficult to achieve this level of cash flow, given current fundamentals at the “Big Three”, and believe that investors’ expectations of the dividend’s growth trajectory may be at risk.

For the long-term, is this slide from the company’s most recent Annual Report still representative of management’s expectations? The blade on that hockey stick seems to be getting longer. We will be seeking more specificity on this going forward (chart below).

On the point of capital budget reductions for 2014, there seemed to be some incongruity in the message being delivered to shareholders. Brad Richmond, Darden’s CFO, said that FY14’s capital budget is likely to come down by “as much as 10%”. In response to the first question of the Q&A segment of the call, Clarence Otis, Darden’s CEO, stated that this figure would be “at least 10%”. We can only deduce from this that 10% is, as the questioner suggested, the “opening bid” and a more drastic reduction in growth is possible if restaurant-level performance does not improve.

Top-line Numbers Speak to Greater Strategic Issues

Recognizing the need to slow growth is one step on the path to redemption for this company but this quarter did not represent a full mea culpa.

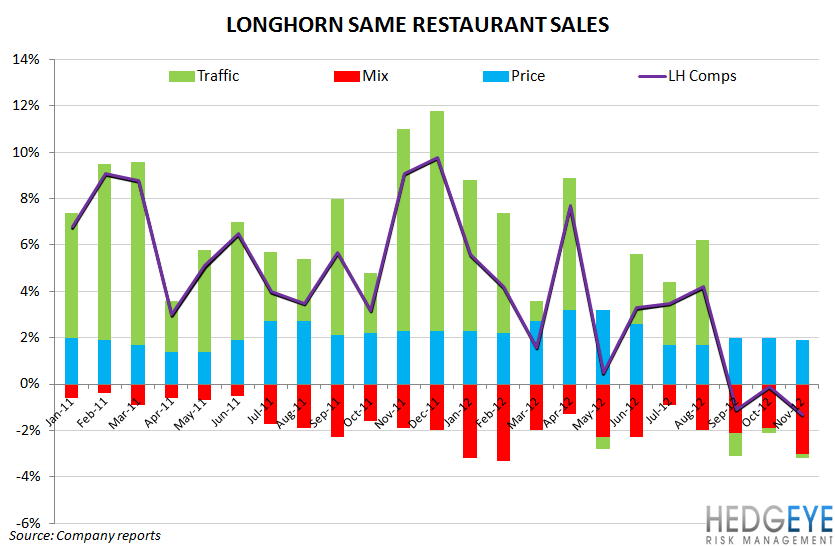

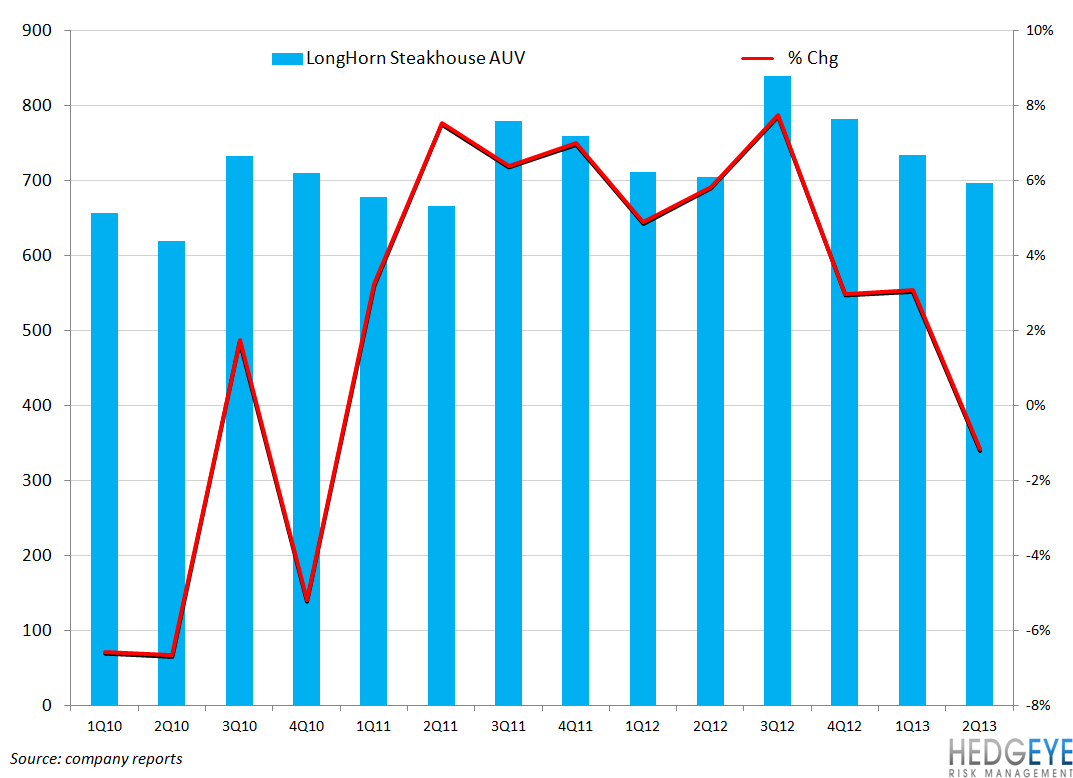

The pre-announced same-restaurant sales numbers highlight significant challenges being encountered at OG, RL, and LH. This morning’s earnings call brought us more of what we have heard before: unclear and meandering statements that fall well short of reassuring investors of the company’s position. While the capex budget will be cut, management’s repeated claim that there has been “meaningful progress” made at each brand over the last three years is not supported by the facts. The effectiveness of management’s promotions has, as we have been arguing for several quarters, been hit-or-miss at best. The company’s ability to discern what products will perform well at market is under much doubt this morning:

“We've got a much more dynamic market than we have historically. And so, consumer confidence moves around a lot more. The competitive dynamic is such that people are in and out with things a lot more than they used to be. And so for sure, as we test something, we have to discount those results more than we've had to do in the past because the environment where we launch may have some pretty important differences from the environment where we tested and so, we recognize that.”

-Clarence Otis, CEO of Darden, 12/20/12

Recognizing that the margin profile of the company needs to change is also an important step for the company to regain its footing. Olive Garden’s value leadership position has been eroded over the last few years but, clearly, repositioning a system as large as Olive Garden will take time. The turnaround will likely involve recalibrating the consumer’s perception of the brand and this could take time.

The “Big Three” Are What Matters For Now; The Rest Is Noise

This is a company that derives roughly 87% of its revenue from its three largest concepts: Olive Garden, Red Lobster, and LongHorn Steakhouse. While yesterday’s article in The Wall Street journal highlighted the Specialty Restaurant Group, which constitutes 12% of the consolidated revenue, and its growth potential for Darden, clearly the company’s share price will continue to be primarily driven by the performance of Olive Garden (OG), Red Lobster (RL), and, to a lesser extent, LongHorn (LH), over the next number of years.

What Now?

We believe that the takeaway from this earnings call is that casual dining is embarking on a period of war between the largest chains. Nobody wins in a nuclear war and we expect lower prices at Darden’s chains to have a significant impact on all of casual dining.

We remain unconvinced that Darden’s dividend is safe or, indeed, that the question about the dividend is how much it will grow by, as Clarence Otis suggested this morning. Tough times lie ahead for Darden and, while we are not stating that we believe the dividend is definitely getting cut, we are placing the burden of proof squarely on management’s shoulders.

This stock, for us, has been a “show me” stock for several quarters as the company’s reactionary strategies have yielded disappointing results. Confirmed by the line of questioning on today’s call, we believe that the investment community is adopting a similar stance, becoming less and less willing to give management the benefit of the doubt.

For much of calendar 2012, earnings revisions have been negative. The stock price has largely ignored this as some analysts touted the yield and “stable cash flows” of the company as reasons to buy. If confidence erodes further in the security of the dividend, expect the share price to correct significantly.

Howard Penney

Managing Director

Rory Green

Senior Analyst