I’m convinced that supply chain pressure of the past 2 yrs will ease. Perhaps temporarily…but it will ease. And Soon. Add SG&A/capex cuts, positive sales delta and cheap stocks… You get the picture.

This might be the longest note I’ve ever posted, but the narrative must be spelled out in every detail. To ignore this will be to ignore a potentially meaningful second leg of a retail rally (but this time driven by fundamentals – augmenting my 3/5 call).

China accounts for 87% of US footwear consumption, and 30% of apparel (and growing). Let’s think about history for a minute…

2000-2007

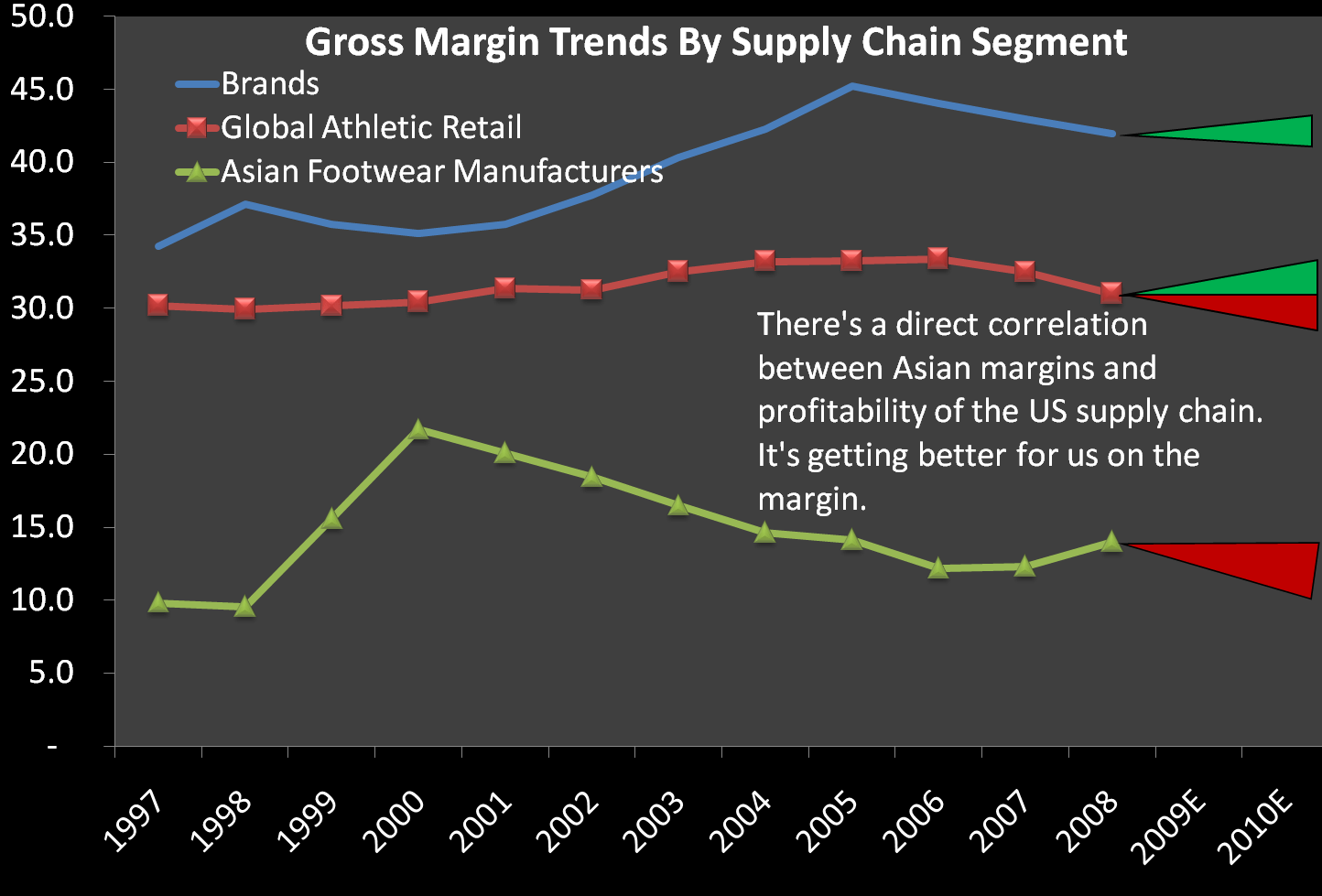

1) From 2000-2007, margins for Asian manufacturers went down by 8 points. Margins for the brands went up by 8 points. Retail margins have been flat. There's only so much margin to go around, so the direct inverse correlation is no coincidence.

2) In the early 2000s Asian manufacturers had around a 15-20% gross margin, which was more than enough to offset the roughly 10% in SG&A and capital costs to turn a profit. This was especially the case given that the Chinese government rebated the VAT tax, which added between 3-7% in net profit for the manufacturers. All said, life was good as a manufacturer, which is why capacity grew at a mid-single-digit clip. Excess capacity = more pricing leverage on the part of the front-end of the supply chain.

3) Starting in early 2007, factory gross margins approached the break-even hurdle, Chinese VAT tax rebates were phased out to stimulate local consumption as opposed to export, and costs headed higher across the board.

4) The result? Capacity growth slowed meaningfully, and was flattish by the end of the year. This meant that the pendulum swung back into the hands of the US supply chain with $3-4bn annually to pad the supply chain.

2008

Then came last year, which caused a massive reversal in the Asian side of the equation – and came alongside (and intermingled with) the US Great Recession.

1) 2008 started out with the biggest snowstorm in China in 100 years. It completely shut down the Eastern provinces and the logistical infrastructure of the country was put to (and failed) the stress test. Factories were boxed into a corner.

2) The tragic earthquake in the spring was a double whammy. Not only did this test the infrastructure once again, but the ‘human factor’ prompted migrant workers – that account for about a third of production in the Pearl River Delta factories – to simply not show up. Migrant workers that don’t migrate? Yes, that’s a problem.

3) A third important point is that in advance of the Olympics, the Chinese government cracked down on sweat shops, and started to mandate that factories pay employees back-pay for unused vacation time. You know how Americans take 2-3 weeks of vacation per year at best? And how the Brits will commonly ‘go on Holiday’ for a 5-week clip at a time? Trust me; compared to the under-vacationed US workforce, the Chinese factory-worker culture makes us look like Americans are on permanent vacation.

4) What does all this mean? Natural disasters stressed output and tightened prices for exports in aggregate. Then the government decided to wipe out the ‘sweat shop’ factor to appease human rights activists. You might say ‘the Chinese don’t ‘appease’ anybody.’ Well, in the months alongside the Olympics – otherwise known as China’s coming out party – I’m willing to bet that China reigned in its pride and cleaned itself up a bit.

5) Oh yeah…did I mention that not only did the VAT tax rebate come down, but absolute export taxes went up at a steady clip in 2007/08 as China changed its tax system to encourage local consumption over export?

6) China went through a 2-year capacity tightening phase, which pressured pricing in the US supply chain for this industry (and others). Using footwear as an example, there were 12,000 factories in the Pearl River Delta 2-years ago. Now there are about 6,000.

2009

Ok smarty pants…so now what?

1) We’re looking at a teens rate of import taxes…that has been recently reduced to zero. Yes, a donut.

2) Today China announced that its VAT (Value Added Tax) tax rebates on garments go up to 16%. Yes, this means that local factories are incentivized again to export product as the government funds enough of their P&L so they can sell product at a break even rate and still be cash flow positive.

3) Within hours of China’s announcement, Vietnam proposed to cut its Value Added Tax (VAT) on VAT on yarn, fabric, and garments, as well as reduce the corporate income tax rate by 30 percent for textile, garment and footwear industry.

4) As a kicker we see Nike pulling out of four Asian factories – three in China and one in Vietnam. This is part of Nike’s restructuring, but is pretty darn well timed given geo-political events. I guess Nike ‘does macro.’

The bottom line: I am convinced that the supply chain pressure we’ve been feeling over the past 2 years will ease. Perhaps temporarily…but it will ease. Add on SG&A/capex cuts, a positive sales delta and cheap valuations… You get the picture. Names I like best in retail include BBBY, RL, LULU, LIZ, UA, and DKS. I don’t like those who are cutting into bone to print profit, such as Ross Stores, Iconix, Sears, Carter’s, Jones and Gildan. The challenge here is that this latter basket of companies will also show a reversal in cash flow trends, temporarily masking the damage they are doing to their base business.

I’ll be working closely with Keith to game the sizing and timing on these fundamental ideas when the group looks more ‘shortable’ and/or when the near-term fundamentals for each of these names present an opportunity.