TODAY’S S&P 500 SET-UP – December 20, 2012

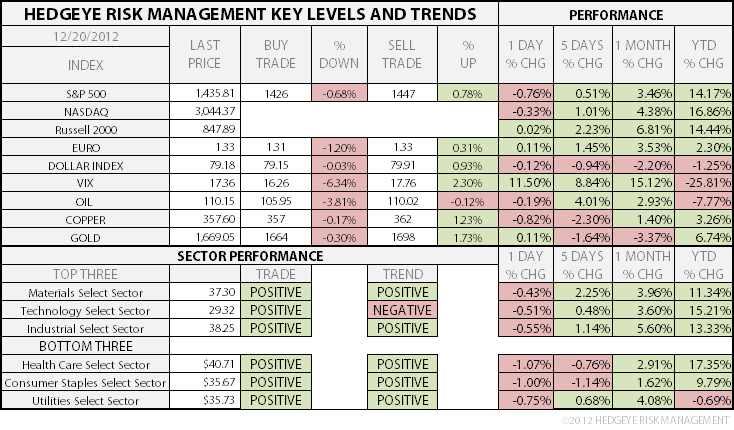

As we look at today's setup for the S&P 500, the range is 21 points or 0.68% downside to 1426 and 0.78% upside to 1447.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.51 from 1.53

- VIX closed at 17.36 1 day percent change of 11.50%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: 3Q GDP, est. 2.8% (prior 2.7%)

- 8:30am: Personal Consumption, 3Q, est. 1.4% (prior 1.4%)

- 8:30am: Core PCE, 3Q, est. 1.1% (prior 1.1%)

- 8:30am: Init. Jobless Claims, Dec. 15, est. 360k (prior 343k)

- 8:30am: Cont. Claims, Dec. 8, est. 3.200m (prior 3.198m)

- 9:45am: Bloomberg Consumer Comfort, Dec. 16 (prior -34.5)

- 9:45am: Bloomberg Economic Expectations, Dec. (prior 4)

- 10am: Freddie Mac mortgage rates

- 10am: Philadelphia Fed., Dec., -3.0 (prior -10.7)

- 10am: Existing Home Sales, Nov., est. 4.90m (prior 4.79m)

- 10am: Leading Indicators, Nov., est -0.2% (prior 0.2%)

- 10am: House Price Index, Oct., est. 0.3% (prior 0.2%)

- 10:30am: EIA natural gas storage change

- 11am: Fed to purchase $1.5b-$2.25b notes in 2023-2031 sector

- 1pm: U.S. Treasury to sell $14b 5Y TIPS in reopening

- 2pm: Fed to sell $7b-$8b notes in 2015-2016 sector

GOVERNMENT:

- Washington Day Ahead

- House, Senate in session

- Senate Banking panel holds hearing on rebuilding after Hurricane Sandy, 11am

- House Intelligence hold closed meeting to consider national security issues posed by Chinese telecommunications companies Huawei, ZTE, 9am

- SEC holds closed meeting on enforcement matters, 2pm

- FERC holds monthly meeting on power-grid reliability, 10am

WHAT TO WATCH

- IntercontinentalExchange said in talks to buy NYSE Euronext

- Budget talks deteriorate amid Republican identity shift on taxes

- AMR said to take steps moving closer to merger with US Airways

- BofA’s Moynihan said to kill proposal to cut payouts for brokers

- Google to sell Motorola Home to Arris for $2.35b

- 3 former Swiss bank advisers charged by U.S. with conspiracy

- U.S. housing values rose 6% in 2012 for 1st gain in 6 yrs: Zillow

- Bank of Japan expanded its asset-purchase program for 3rd time in 4 mos.

- U.K. Nov. retail sales unchanged, median est. 0.4% increase

- Roche may agree to buy Illumina for $66/shr, L’Agefi says

- Carl Icahn’s American Railcar sweetened its offer for Greenbrier by 10%, set a deadline of tomorrow

- Allscripts replaced CEO, said no longer planning to sell itself

- Pershing’s Ackman to speak at Ira Sohn special event on Herbalife

- Accenture falls after longer consulting projects crimp rev.

EARNINGS:

- Darden Restaurants (DRI) 7am, $0.30

- ConAgra Foods (CAG) 7:30am, $0.55

- CarMax (KMX) 7:35am, $0.39

- KB Home (KBH) 8am, $0.06 - Preview

- Discover Financial Services (DFS) 8:30am, $1.13 - Preview

- Neogen (NEOG) 8:45am, $0.27

- Carnival (CCL) 9:15am, $0.11

- Micron Technology (MU) 4pm, $(0.20)

- Red Hat (RHT) 4:04pm, $0.29

- Tibco Software (TIBX) 4:04pm, $0.37

- Research In Motion (RIM CN) 4:05pm, $(0.35) - Preview

- Nike (NKE) 4:15pm, $1.00

- Cintas (CTAS) 4:15pm, $0.62

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – we re-shorted Oil yesterday as it tested immediate-term TRADE resistance of $110.02 Brent; it’s a long way down from here for Oil, especially if the USD holds higher long-term lows here – Down Oil is the bull case for Long Consumer Stocks (we bought back XLP, Consumer Staples) on red yesterday.

- Brent Crude Trades Near Two-Week High as North Sea Exports Drop

- Silver Vaults Stuffed Means Price Rising 30% in ’13: Commodities

- Copper Declines for a Fourth Day in New York on U.S. Budget

- Gold Climbs in New York After Two Days of Declines; Silver Gains

- Coal Rebound Seen From Biggest Drop Since 2005: Energy Markets

- Ethanol Fuel Blend Wall Can Be Eased With Higher Blends, Exports

- Palm to Test 1,950 Ringgit in Bearish Trend: Technical Analysis

- Rubber Declines From Seven-Month High on U.S. Budget Concerns

- Vale Seen Paying $158 Million More for Shipping by Alphabulk

- Wheat Drops Below $8 a Bushel for the First Time in Five Months

- Uralkali Sees 2013 Potash Supplies Recovering to 55 Million Tons

- India Sugar Imports Seen Surging as Global Glut Cuts Prices

- Chaebol Founder Dismantles Life’s Work as Slump Deepens: Freight

- Lumber Is Top Pick by Scotiabank Leading 2013 Commodities Rally

CURRENCIES

EUROPEAN MARKETS

ITALY – Italian Retail Sales -3.8% y/y in OCT vs -1.6% SEP continued to worsen and the MIB Index looks very different than the DAX now (DAX making higher-highs vs SEP, MIB making lower-highs); we haven’t been short anything Europe for a while, but Italian stocks looking more interesting now, short side. Timing matters.

ASIAN MARKETS

JAPAN – hello my old friend volatility! The Japanese are pulling a Bernanke here and getting the same results (inflated stock market and no economic recovery); Japanese Exports down -4.1% y/y in NOV is a certified economic disaster and they just upped their asset purchase fund to 76 TRILLION Yens (from 66T) and the market didn’t think that was enough!

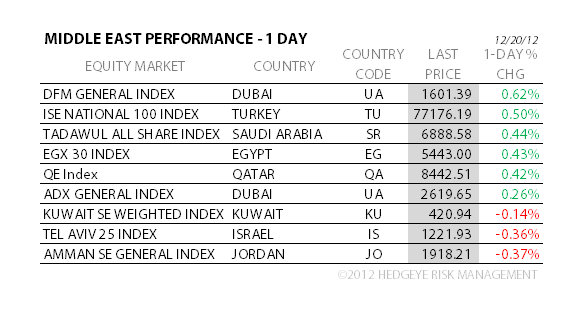

MIDDLE EAST

The Hedgeye Macro Team