This note was originally published at 8am on December 06, 2012 for Hedgeye subscribers.

“Few soldiers knew the history, and most didn’t give a damn.”

-Michael Sallah

Sound familiar? History matters. And that doesn’t just hold for the Geneva Conventions (1949). It holds for the Constitutional and economic history of the United States of America too. We shouldn’t give a hall pass to the willfully blind.

The aforementioned quote comes from a chilling book that I am reading right now about Vietnam: Tiger Force - A True Story Of Men and War, by Michael Sallah and Mitch Weiss. It won the Pulitzer Prize in 2004 and is a glaring example of how groupthink can dominate decision making by men abusing authority.

When it comes to the big rules in life, most of us follow them. Some don’t. But when we catch them, they pay the price. What is the free-market price we are willing to pay the #PoliticalClass in this country? Giving up our children’s liberties violates the US Constitution. It may not matter in the moment. But I am guessing that if we keep this up, it eventually will.

Back to the Global Macro Grind…

After the market close yesterday Timmy Geithner proclaimed his mystery of faith that “we’ll fall off the cliff if taxes don’t rise.” Really? Is that a threat? Or is he abusing his political power to do more of what many men and women before him have? Fear monger.

Geithner is one of the more unique authorities of the US #PoliticalClass because he has spent 54% of his born life working for the US government. That’s a long time – and boy has he raised a lot of debt and government spending along the way.

As a reminder, this generational (and Constitutional) debate in America isn’t just about raising the #PoliticalClass’ “revenues”:

- It’s about DEBT (raising the Debt Ceiling requires Congressional approval – yes, that’s a rule)

- It’s about SPENDING (real US government spending just ripped at an annualized rate of +9.5% in the last 3 months)

- And, of course, it’s about TAXES (Geithner calls them revenues because that’s how he gets paid)

Marxists wanted this – so now they have it. This is class war. The #PoliticalClass vs. The Rest of Us.

And if Geithner wants to try to scare the hell out of us threatening to “go off the cliff”, he can go ahead and try – but I for one am not scared of this man. If he was “deeply” worried about this, why in God’s good name was he ramping Government Spending (for the 1st time in 5 quarters) in the last 3 months? Why did he and Obama cheer Bernanke on, printing money and monetizing more US Debt?

Sadly, we all know the answers to these questions.

In other central planning news, Citigroup (C) pulled the ole bait and switch on Geithner and Co. and decided to fire 11,000 people yesterday. If you didn’t know how crony socialism works, here’s the deal: Geithner bails out his boys with your tax dollars, they grease each-other politically saying that they “saved” jobs, then fire everyone so that they can keep getting paid.

The Financials (XLF) liked that yesterday. Meanwhile Apple (AAPL) was collapsing (you only need to be up +30% from here to get back to September’s price to break-even). Now that growth and earnings have slowed, maybe that’s the new bull case – firing people.

What’s a better bull case?

From a US Economic Growth perspective, the only bull case that I can see as sustainable remains Strong Dollar, Down Commodities. Bernanke’s Bubbles (Commodities) are popping, and that’s potentially a very good thing for both US and Global Consumers if Obama just tells Bernanke to get out of the way.

What are the odds of that happening? Low.

Morgan Stanley (MS) is out with a version of the call Goldman (GS) made yesterday (Bloomberg: “Morgan Stanley Backs Gold, Corn, and Beans as Best Picks for 2013”). I smiled when I read that. Our call remains the exact opposite – has been since March 2012.

Despite Goldman pleading that the commodities “super cycle isn’t ending”, it’s pretty clear to us that it has already ended. Whether it’s Freeport McMoran (FCX) or the Gold Miners (GDX) getting blasted yesterday, it’s all one and the same thing to us – over-owned.

The other side of commodities (and their related equity “plays”) melting down since The Bernanke Top (SEP 2012) is of course buying consumption oriented exposures.

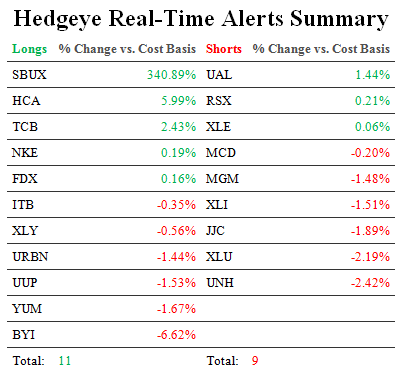

That’s why we bought US Housing (ITB) on red yesterday, and reiterate our favorite big cap Consumer long ideas: Starbucks (SBUX), Nike (NKE), and Yum Brands (YUM) this morning.

Our Financials and Housing Sector Head, Josh Steiner, will be hosting a housing call tomorrow at 11AM EST titled: "Could Housing's Recovery Go Parabolic in 2013?" If you’d like access to the call, please ping Sales@Hedgeye.com.

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1684-1711, $108.61-110.05, $3.54-3.68, $79.61-80.19, $1.29-1.31, 1.58-1.66%, and 1404-1419, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer