We think investors buying BWLD in anticipation of the share price reaching the consensus twelve-month price target are likely to be disappointed.

Buffalo Wild Wings has been one of the more volatile restaurant stocks in 2012. We believe that buyers of the company’s shares risk less-than-expected returns in 2013. That the company is taking 6% of pricing as we near the end of the year is very concerning from the perspective of the consumer’s perception of the brand. Stubbornly high chicken wing prices are forcing management’s hand and, if Sanderson Farm’s commentary from 12/18 is anything to go by, the company’s input costs could remain elevated in 2013.

While we believe the stock is a decent short here and now, we would find it increasingly compelling if the price were to rise closer to $80.

Notable Commentary from SAFM

“As many of you know, the Georgia Dock price is a good indicator of the supply and demand dynamics for products sold to retail grocery stores. The balance of supply and retail grocery demand has held relatively steady through most of the past three fiscal years. The Georgia Dock price needs to move higher still, however, to offset current grain costs.”

“In the past when wings got really truly hot and high, other products found themselves on to menus like boneless wings, boneless breast, chicken tenders. High prices will cure high prices. And I don't know what the ceiling is, but I am guessing that these restaurant owners will find something else put on the menu if they're not making margins. They might go to $2, but my guess is they won't stay there very long.”

Fundamental Outlook

The company’s top-line is likely to be a concern for the next couple of quarters. We see two issues, one specific and one potential, facing the company over the next couple of quarters:

- The company taking 6% price could lead to a greater-than-anticipated slowdown in traffic

- Testing is ongoing of a strategy to sell wings by weight, not number, in several markets

We are cautious on BWLD’s ability to maintain the magnitude of its same-restaurant sales “Gap-to-Knapp” in 2013, particularly if the testing of serving wings by weight becomes the company’s system-wide policy.

Changes in the company’s cost of sales are mainly driven by fluctuations in spot wing prices. Bone-in wings comprise 20% of the company’s basket. Below is a table that we first published at the start of 2012 outlining the sensitivity of BWLD’s earnings per share to 10% of wing price inflation. While boneless wings do offer some shelter from spot market price, since the company contracts boneless wings, the mix shift that the company has managed to bring about during prior bouts of inflation has not been substantial (3% increase in boneless mix in 2009).

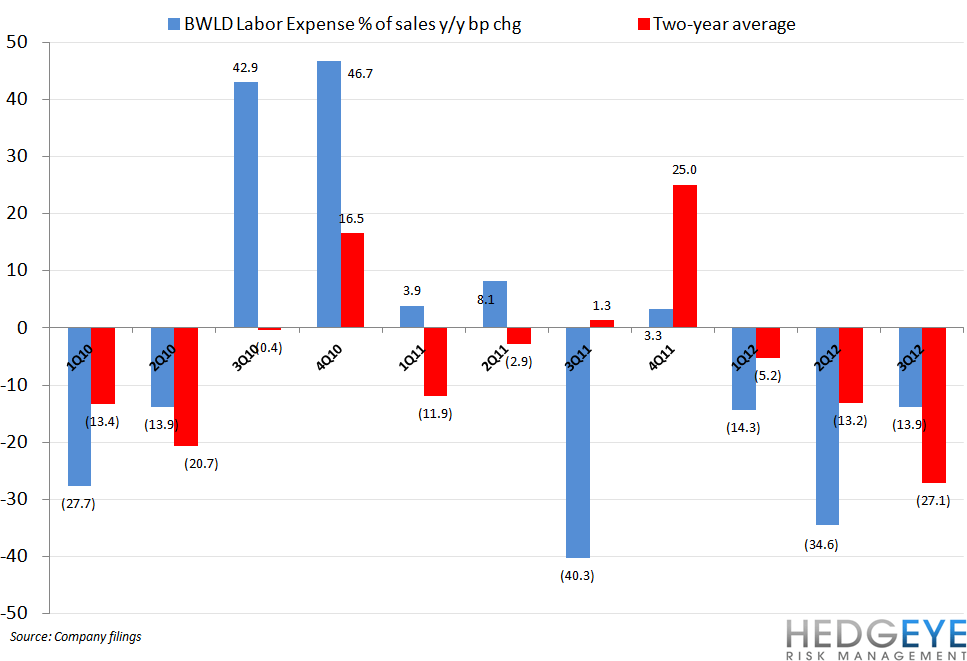

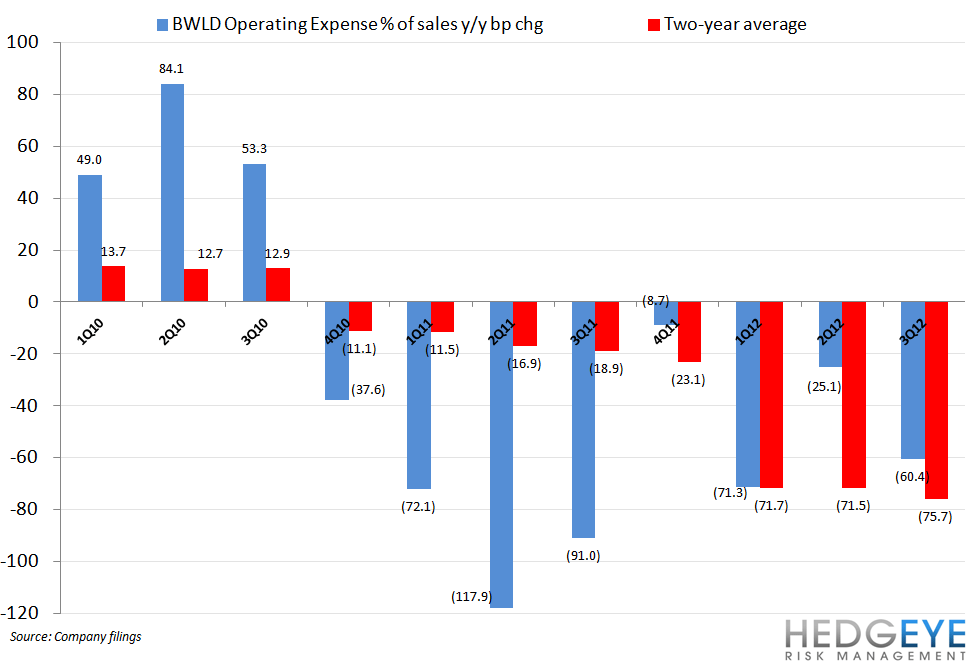

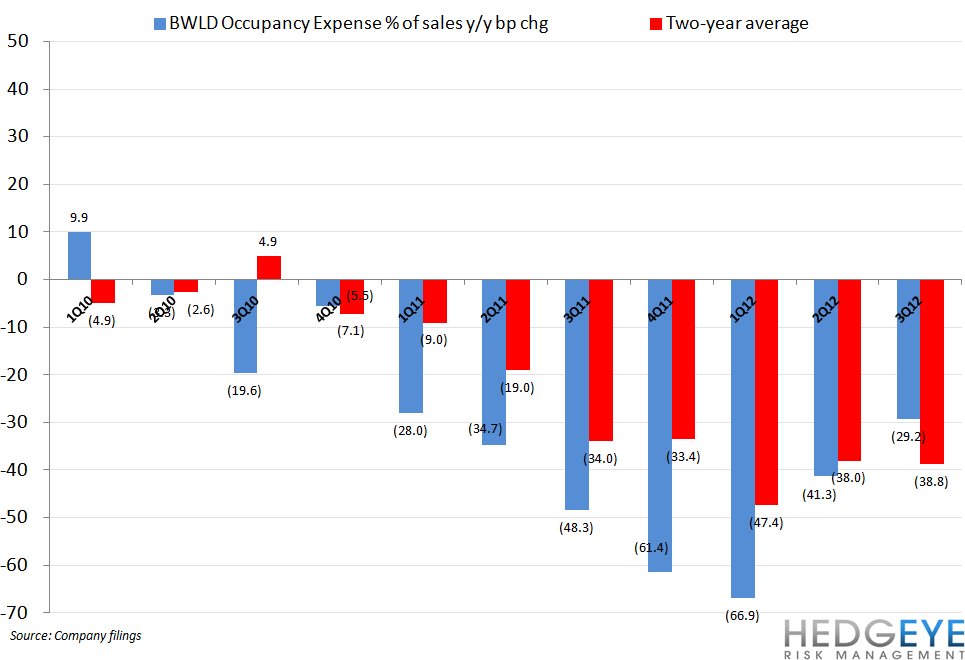

Other operating expenses – Labor, Operating, and Occupancy – have been declining as a percentage of sales for some time. Considering that comps are decelerating and, by these metrics, the company has become more efficient over the last couple of years, it could be a challenge to gain margin from these line items in FY13. Management guided to higher labor costs, as a percentage of sales, in the fourth quarter but consensus is still modeling a year-over-year decline in labor costs as a percentage of sales.

Howard Penney

Managing Director

Rory Green

Senior Analyst