Macau generated average daily table revenue of HK$775 million in the past week, down from HK$930 million in the first 10 days. ADTR actually fell 1% from the similar week of 2011. As we learned from our Macau trip last week, hold percentage ran high in the first 10 days (with the exception of Wynn) but seems to have been normal in the past week. Our YoY projection is for GGR (including slots) YoY growth of 10-14%.

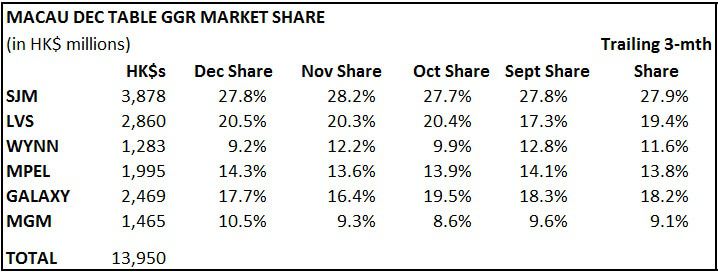

While still above trend, LVS’s share has moderated to where we would project it to be. Absent hold fluctuations, we believe LVS will be a consistent market share gainer over the next 12 months. MPEL’s share has also moderated but still above trend. MPEL remains on track for an estimated beating Q4, in our opinion. Surprisingly, Wynn picked up very little share in the past week and remains >200bps below trend. Galaxy is almost back to normal while MGM is definitely having a good month.