TODAY’S S&P 500 SET-UP – December 17, 2012

As we look at today's setup for the S&P 500, the range is 23 points or 0.39% downside to 1408 and 1.23% upside to 1431.

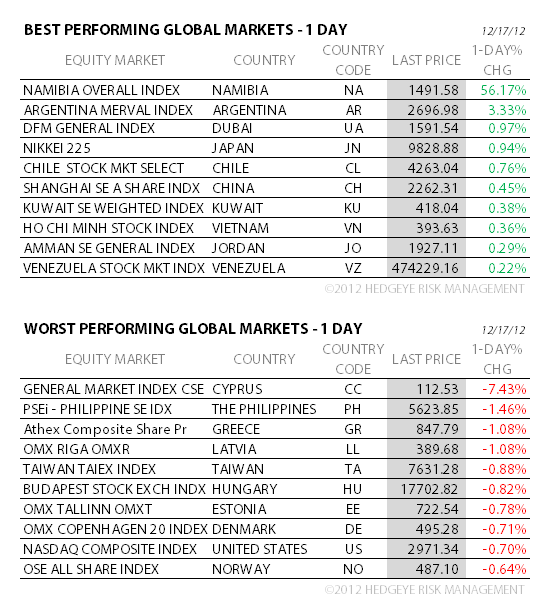

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.49 from 1.47

- VIX closed at 17.0 1 day percent change of 2.66%

- UST 10YR – more commodity deflation this morning is good for #GrowthStabilizing expectations (consumption), globally. 10yr yield is +2bps this morning to 1.72%, 3bps above my TREND line (was resistance) of 1.69%; #1 way to get people to buy equities for real is get the flows back (they’re in bonds).

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Empire Manufacturing, Dec., est. -1.0 (prior -5.22)

- 9am: Total Net TIC Flows, Oct. (prior $4.7b)

- 9am: Net L-T TIC Flows, Oct., est. $25.0b (prior $3.3b)

- 11am: Fed’s Stein speaks on dollar funding in Frankfurt

- 11am: Fed to buy $4.25b-$5.25b notes in 2018-2020 sector

- 11:30am: U.S. Treasury to sell $32b 3M, $28b 6M bills

- 1pm: U.S. Treasury to sell $35b 2Y notes

- 1pm: Fed’s Lacker speaks on economy in Charlotte, N.C.

GOVERNMENT:

- House, Senate in session

- Federal Retirement Thrift Investment Board meets, 10am

- Defense Secretary Leon Panetta discusses U.S. policy, 1pm

WHAT TO WATCH

- Apple downgraded at Citigroup; drops below $500 pre-mkt

- Boehner offers Obama tax-rate-boost deal w/ entitlement cuts

- Google said to end FTC probe with letter promising changes

- AIG offers to sell as much as $6.5b of AIA shares

- First Quantum again raises offer for Inmet Mining

- UBS said to face $1.6b penalty as Libor settlement looms

- Starwood Capital nears buy of Principal Hayley: Sunday Times

- China signals tolerance of slower growth after annual mtg

- Abe’s LDP wins victory over Noda in Japan election rout

- Novartis therapy wins U.S. backing for Cushing’s Disease

- Cisco said to hire Barclays to sell Linksys routers unit

- Jackson’s “Hobbit” tops weekend box office at $84.8m

- Holiday spending “modest” through Dec. 8: SpendingPulse

- SAC e-mails show Cohen consulted on Dell trade

- Akamai Says co-founder Leighton to become CEO effective Jan. 1

- Spending probably rose, home sales climbed: U.S. eco preview

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

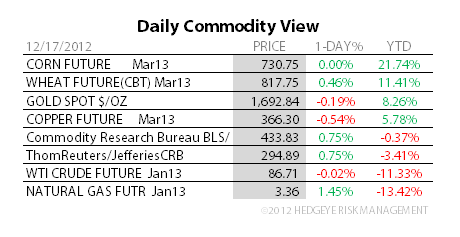

GOLD – gold just doesn’t like rising rates - never has – and that makes sense as absolute return (up for 12 straight yrs) on gold looks less exciting when risk free rates move higher. Gold remains bearish TRADE and TREND in our model with a big zone of resistance up at $1/oz.

- Hedge Funds Reduce Bullish Bets by Most in a Month: Commodities

- Rubber Surges to Seven-Month High as Yen Weakens on Abe Victory

- JPMorgan Wins SEC Approval for Physically-Backed Copper ETF

- Gold Drops on U.S. Fiscal Cliff Talks as ETP Holdings at Record

- Soybeans Jump to Five-Week High as U.S. Crushes Most Since 2010

- Rebar Extends Gain on Demand Outlook as China Flags Urban Growth

- Oil Bulls in Biggest Retreat in Seven Months: Energy Markets

- China Cuts Natural Rubber Import Taxes to Boost Local Supplies

- Malaysia Sets Zero Export Tax for Crude Palm Oil to Cut Reserves

- India Cuts Benchmark Import Price of Gold to $550 Per 10 Grams

- Malaysia Sets Crude Palm Oil Export Tax at Zero for January

- Natural Gas Prices Need Cold Winter to Get Off Floor: Outlook

- HKEx May Allow Chinese Cos. as LME Category 1 Members, HKET Says

- Brent Crude Futures Drop Amid Disagreement in U.S. Budget Talks

CURRENCIES

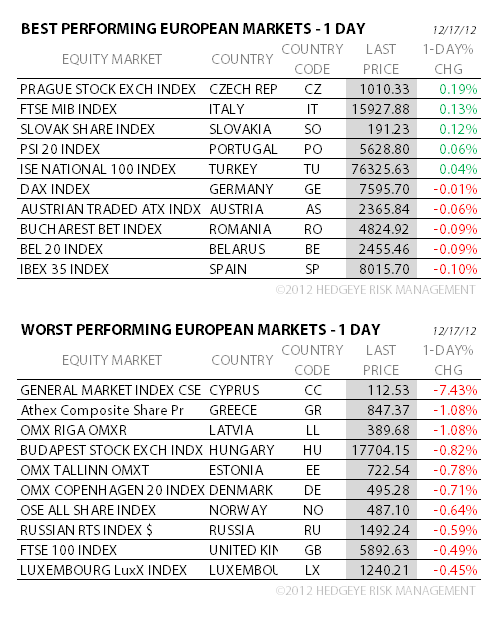

EUROPEAN MARKETS

ASIAN MARKETS

JAPAN – the Japanese begged for a bailout bureaucracy and got it with a big LDP win over the weekend and follow through buying in the Nikkei (up another +0.94% to 9828, up +13.5% since mid November!). Probability continues to rise that Japan becomes 1st modern economy to fall on the sword of Keynesian economic policy (burning currency). Economic data is awful.

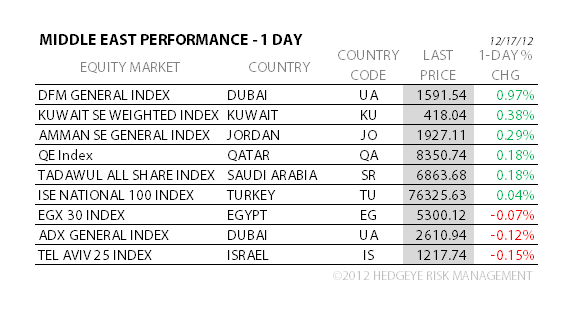

MIDDLE EAST

The Hedgeye Macro Team