TODAY’S S&P 500 SET-UP – December 14, 2012

As we look at today's setup for the S&P 500, the range is 25 points or 0.67% downside to 1410 and 1.10% upside to 1435.

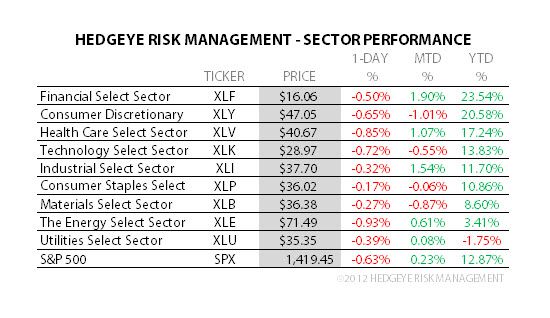

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.49 from 1.48

- VIX closed at 16.56 1 day percent change of 3.82%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Consumer Price Index M/m, Nov. est. -0.2% (prior 0.1%)

- 8:30am: CPI ex-Food & Energy M/m, Nov. est. 0.2% (prior 0.2%)

- 8:58am: Markit US PMI Preliminary, Dec. est. 51.8 (prior 52.4)

- 9:15am: Industrial Production, Nov. est. 0.3% (prior -0.4%)

- 9:15am: Capacity Utilization, Nov. est. 78.0% (prior 77.8%)

- 11am: Fed to buy $1.5b-$2.25b notes due 2/15/36-11/15/42

- 1pm: Baker Hughes rig count

- 3pm: Fed holds open meeting in D.C. on foreign bank standards

GOVERNMENT:

- Elisse Walter succeeds Mary Schapiro as chairman of SEC

- Federal Reserve Board will hold open board meeting to discuss standards for foreign banks operating in the U.S., 3pm

- Deadline for state governors to tell federal government whether they plan to build health exchanges, control sale of health insurance in their states after 2013

- Deadline set by FERC for Barclays to respond to show-cause order in market manipulation case, $470m penalty

WHAT TO WATCH

- Obama meets with Boehner as pressure builds for U.S. budget deal

- PPG buys Akzo’s U.S. household paints unit for $1.05b

- Hostess said to attract first-round bids from Wal-Mart, Kroger

- S&P ordered by Japanese regulator to improve ratings system

- GE may boost its qtr dividend to 20c/shr from 17c/shr

- Alcatel wins $2.1b loans from Goldman, Credit Suisse

- UBS said to face fines of over $1b in Libor-fixing probes

- Another Facebook lockup expires; FB shrs up 34% since Oct. 31

- Schulze seen making bid for Best Buy; faces Dec. 16 deadline

- FTC may rule on Google search in coming days: reports

- Europe Nov. car sales fall as EU demand at 19-year low

- Manufacturing in China may grow at faster pace in Dec., HSBC data show

- Liberty Media contacts possible buyers for Starz: NY Post

- ITC judge to issue findings in patent-infringement case against Intel brought by X2y Attenuators

- Bank of America says MBIA defaulted on contested securities

- Southwest Airlines, Illinois Tool Works host investor mtgs

- Japan Elections, S. Korea, U.S. Housing: Week Ahead Dec. 15-22

EARNINGS:

- North West (NWC CN) C$0.38

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COMMODITIES – CRB Index down another -1% on the wk to 292 and Gold down again this morning is a very good thing for #GrowthStabilizing, globally, on the margin. Economic recoveries don’t occur w/ $150 Oil and $1900 Gold, fyi. Sets up great for our LONG Consumption vs SHORT Commodities theme.

- Oil Heads for Weekly Gain on China, U.S. Manufacturing Outlook

- Wheat Bulls Retreat as U.S. Estimates Roil Markets: Commodities

- Copper Extends Fifth Weekly Gain After China Data Boost Outlook

- Gold Swings Between Gains and Drops on Stimulus, Budget Concerns

- SHFE Copper Stockpiles Climb as Lead Jumps to 14-Month High

- Soybeans Advance to One-Week High as U.S. Export Sales Increase

- OPEC Status Reduced to Sentiment Driver as Oil Share Wanes

- Rebar Climbs to Five-Month High as China Data Boost Outlook

- Sugar Exports From Pakistan May Miss Target on Global Surplus

- Oil May Drop on Uncertainty in Budget Talks, Survey Shows

- Ethanol’s Discount to Gasoline Narrows on U.S. Budget Stalemate

- Air Cargo Slowdown Puts Squeeze on Specialist Carriers: Freight

- China’s 2012-2013 Corn Imports to Decline, Sinograin Says

- Rubber Jumps to Six-Month High on China’s Manufacturing Outlook

CURRENCIES

EUROPEAN MARKETS

GERMANY – now the DAX (which is crushing the Dow) is A) making higher-highs vs the SEP highs (US stocks haven’t, yet) and B) the high-frequency economic data supports it (Germany’s Service PMI reading for early DEC 52.1 vs 49.7 NOV, finally signaling some expansion – the ZEW was solid earlier this wk as well). Both China and Germany going the right way at the same time – that’s new.

ASIAN MARKETS

CHINA – massive melt-up in Chinese stocks overnight; +4.3% taking the Shanghai Comp to +9.6% in 2 weeks – that’ll get the machines’ attention; so will a breakout > 2095 TREND resistance (now support) for the Chinese A-shares Index. China has had its best moves in the last 5 years when commodity deflation starts to take hold – time for Bernanke to get out of the world’s way.

MIDDLE EAST

The Hedgeye Macro Team