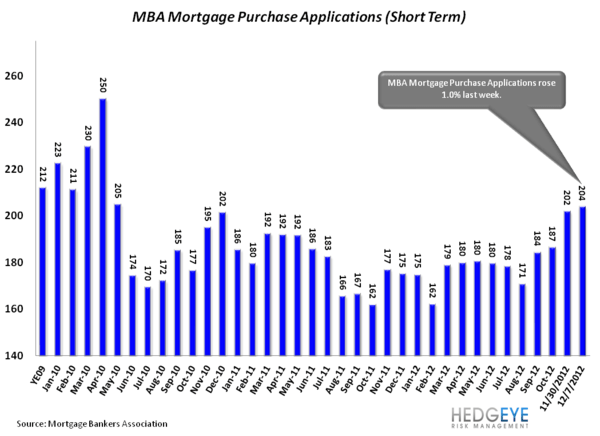

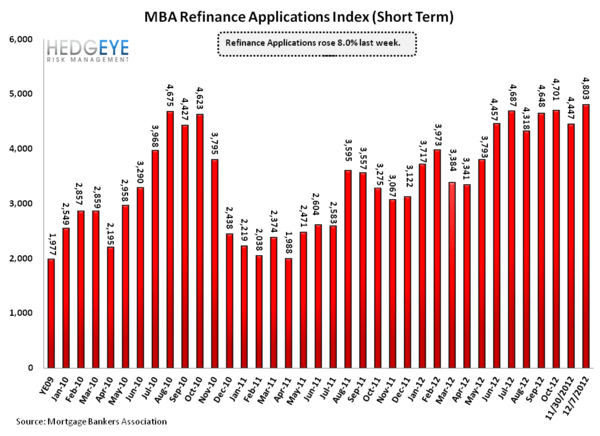

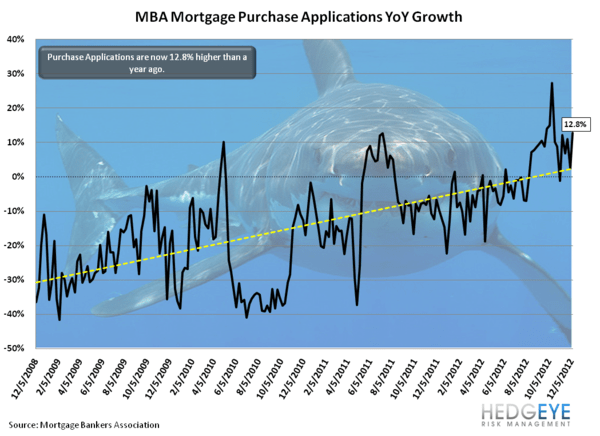

The MBA Mortgage Purchase Applications Index rose 1% last week, the fifth consecutive week of gains for the index; purchase applications are now 12.8% higher than they were a year ago. Refinance applications rose 8% last week as rates fell to 3.39%. Demand to buy homes continues to rise rapidly on a week-over-week basis as recovery in housing strengthens.