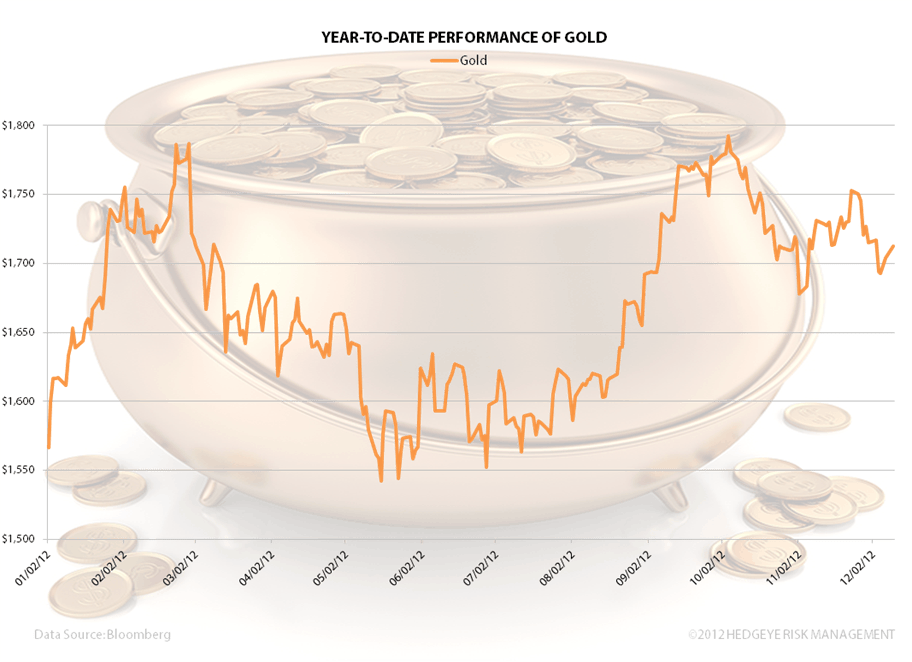

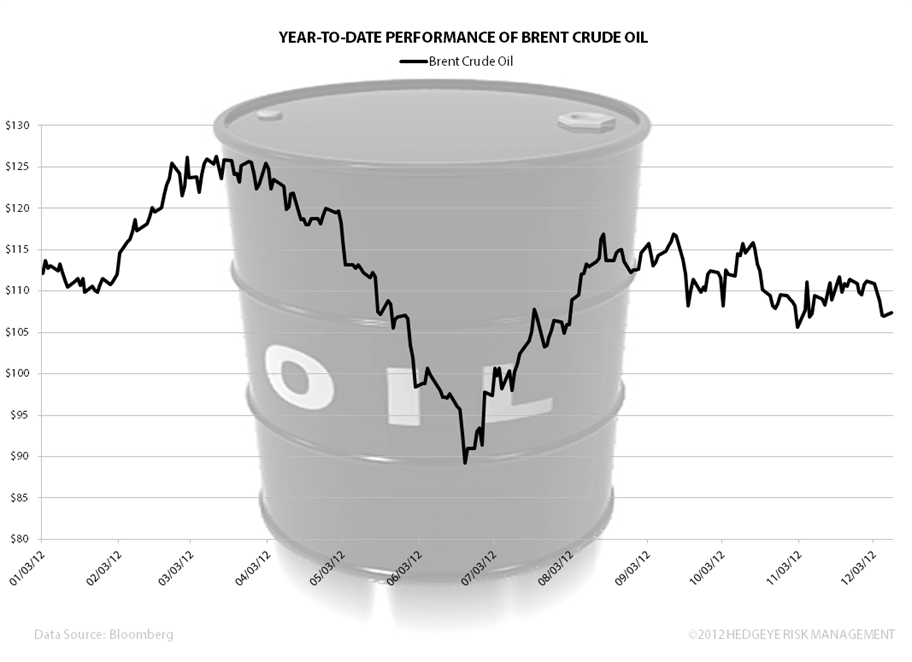

With 2013 less than a month away, let's review where we're at in 2012 thus far. It's become clear that the game of printing money at the Federal Reserve (i.e. quantitative easing) isn't working the way many had hoped it would. The S&P 500 is up 13.5% on a year-to-date basis but has yet to reclaim the levels seen since the Bernanke Top (September 14). Gold continues to remain inflated courtesy of the Fed having also declined in price since September. Brent crude oil is down significantly since its February highs and we expect it to head lower into the new year. 2013 will largely be affected by the outcome of the fiscal cliff. Should Congress get its act together, we can, at least for the short-term, expect a buyer's rally across multiple asset classes.