McDonald’s reported Global SSS growth of +2.4% in November versus Consensus Metrix -0.1%. Importantly, the US posted +2.4% SSS versus consensus of -0.8%. Europe grew SSS 1.4% in November, 130 bps ahead of consensus, and APMEA grew comps +0.6% versus consensus of -0.4%.

United States

The US business reported +2.5% same-store sales growth, far in excess of -0.8% consensus. The US division was benefiting from a calendar shift and a heavy value push. On a two-year average basis, trends improved to +4.5% from 1.5%. October was negatively impacted by calendar shifts; the chart below, on the right, shows calendar adjusted trends which illustrate a more modest improvement in November from the previous month’s trend.

November was driven by a heavy focus on the Dollar Menu. Looking forward, the McRib makes its comeback on December 17th (pushed back from original relaunch date in late October) but 4Q12 trends are still facing an uphill battle as MCD faces its toughest compares of the year in December. Heading into 1Q13, compares will remain very difficult and the competition will also be heating up with Taco Bell ramping up its national voice.

Europe

MCD Europe reported 1.4% comps in November, beating +0.1% consensus. The calendar shift impact helped business in Europe with many previously-negative markets turning positive in November. The UK continued to see positive organic growth in its business. Germany, one of the most important markets in Europe, continues to act as a drag on overall results. Margins in Europe are tracking lower-than-planned this quarter as promoting value has taken a toll.

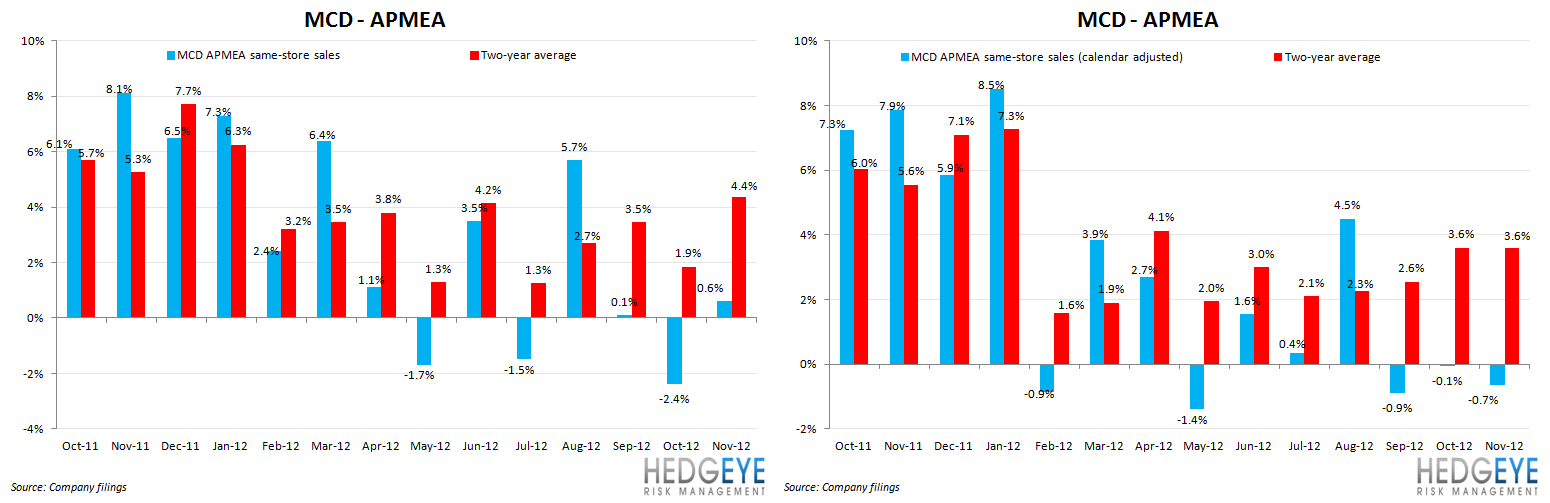

APMEA

The APMEA business grew same-store sales +0.6%, led by Australia, despite ongoing weakness in Japan. A significant portion of the headline improvement in two-year average trends in APMEA was due to the calendar shift. The value message continues to resonate in Australia but trends in China continue to decelerate with trends roughly flat in November.

Takeaway

November was a decent month for McDonald’s but, combining October and November to smooth out calendar-shift impacts shows a trend roughly level with September. We believe that the business, on a global basis, did improve sequentially but by much less than the headline numbers might suggest. The true improvement was modest, in our view, and we would need to see several months of improvement for our skepticism to reverse. We continue to expect margin pressure in 2013 and view FY13 consensus EPS estimates of $5.80 as overly bullish. Until expectations come in, we are not advising clients to buy this stock.

Howard Penney

Managing Director

Rory Green

Senior Analyst