CAT Idea Alert: It Hasn’t Started, So It Isn’t Over

Levels: Long-term TAIL resistance = 89.74; TRADE support = 85.79

We have highlighted a number of the reasons that we are bearish on CAT’s share price. Some investors may think that the worst is over, but capital equipment cycles tend to be multi-year affairs. The resource investment down-cycle hasn’t even started yet for CAT, in our view.

- Mining Capex: While the pending declines in mining capital investment have just started to enter guidance, they have not entered CAT’s reported results yet. Miners like Fortescue (Capex of $3.7 billion in 1H 2012 vs. $1.2 billion in 1H 2012) and Vale (Capex of BRL 10.7 billion in 3Q 2012 vs. BRL 6.1 billion in 3Q 2011) are still reporting massive increases in capital expenditures. Caterpillar has not reported a single quarter reflecting lower mining capital expenditures since the financial crisis, even though the miners have started to discuss the cuts. Instead, CAT’s results still reflect big mining investment increases.

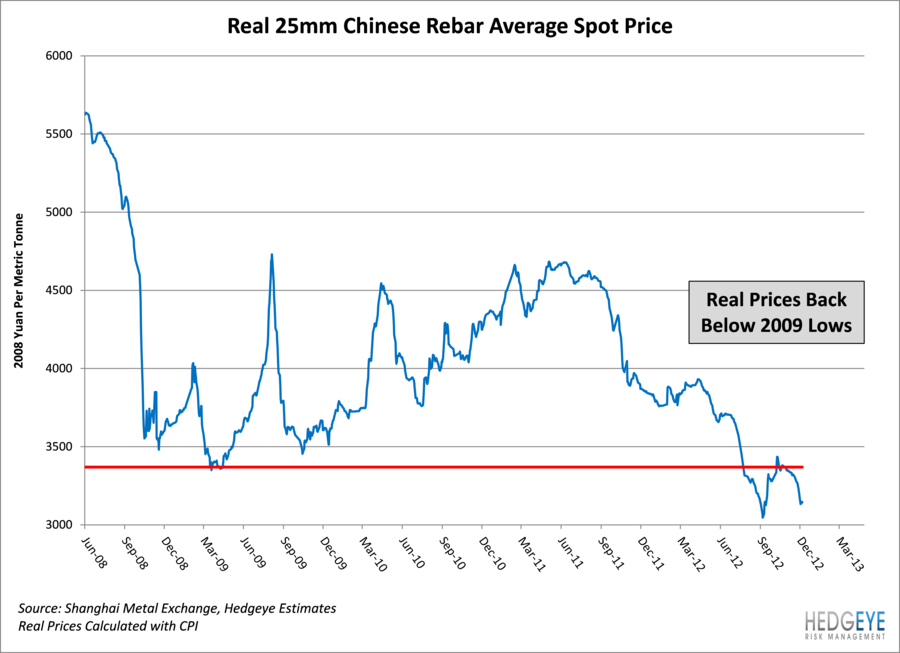

- Chinese Metal Demand: Chinese fixed asset investment has been a big driver of mine expansions. Local construction related commodity prices suggest that party is over for now.

- Inventories High, Capacity High: CAT dealers and CAT BOTH have too much inventory, and not by a small amount. Depending on where demand shakes out, the two probably have $5-$7 billion in excess inventory. CAT has not reported a quarter in which inventories have corrected, yet, and reducing inventories is likely to pressure results. The company will also need to rationalize capacity, which has not happened yet, and will likely also depress results, too, in our view.

- Coal CapEx Cuts: We have not seen coal capital expenditures down this year, although it looks like the cuts will bite this quarter. Coal is a major end-market for CAT and prices have been under pressure globally.

- VERY Early: We believe we are just at the beginning of the correction in resources capital investment. CAT has yet to report a single quarter with the expected declines, so it is probably safe to assume that it isn’t “over.” Investors extrapolating results from recent quarters (by using P/Es, for example) are making a mistake, in our view. Investors are unlikely to “look through” what we expect to be a very long period of adjustment to inventories, capacity and end-markets with any clarity.