We believe the bottoming process in McDonald’s will take longer than some are anticipating. This morning’s upgrade is pushing the stock higher but we see reasons to avoid McDonald’s on the long side for now.

Reasons to Become More Constructive:

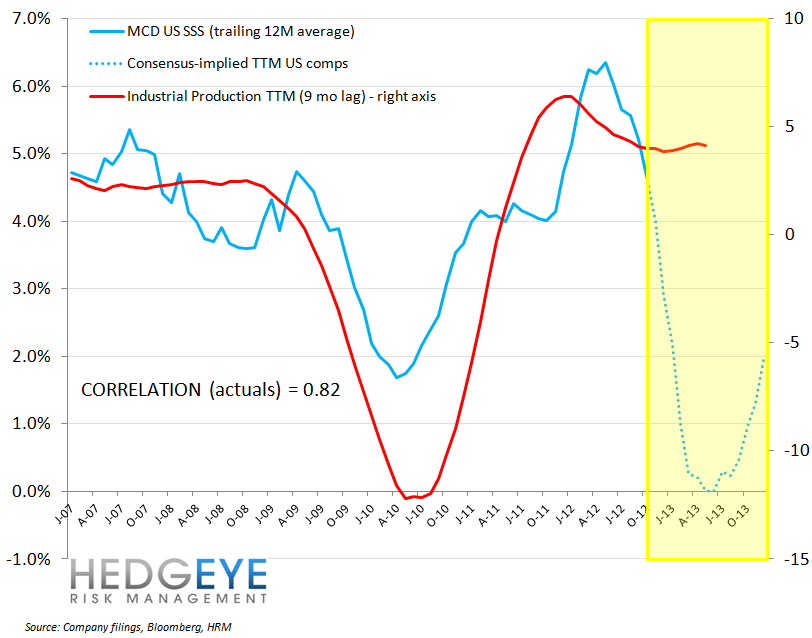

The Yield: This is the #1 reason we hear for people to get bullish on MCD. While we agree that the 3.47% yield is attractive, we believe that buying MCD here for anything more than a short-term TRADE is fraught with risk. Consensus is expecting a “hockey-stick” recovery in earnings growth that we do not expect to materialize.

Sentiment Has Reset: There is an argument to be made that consensus has become too bearish on the immediate-term TRADE but we believe that mistakes on MCD’s part, yet to be acknowledged by management, will continue to hamper same-restaurant sales growth in the important US market.

Compares Will Begin To Ease Post-1Q13: Several weeks ago, we were eyeing this thesis as a potential reason to get long MCD in late FY12/early FY13. We have come to the conclusion that there are self-inflicted wounds impacting McDonald’s sales performance that management has not yet owned up to. The aggressive move to value has not been effective and we do not believe it will be effective next year, despite easing compares. Stiffer competition in the QSR segment in the US makes forecasting FY13 comps difficult. For instance, yesterday at the YUM Analyst Day, we learned that Taco Bell is increasing its target rating points (TRPs) by 44% year-over-year as it transitions to an exclusively nation-wide marketing strategy (no regional advertising).

Reasons to Look Elsewhere:

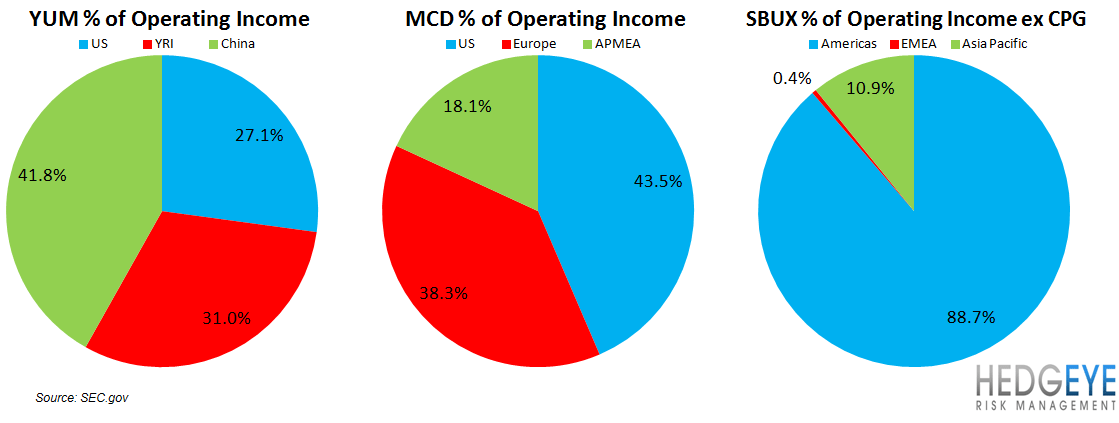

MCD Not the Restaurant Cockroach: We read an interesting paper recently on the long-term resilience of “cockroach” portfolios that yield stable returns through economic cycles. There is a perception that MCD is the “safety trade” in restaurants. We would argue, from an operating income perspective, that YUM is more attractive in this regard given its geographical diversification and best-in-class growth profile.

Valuation Is Not A Catalyst: Valuation is being cited as one reason to get long MCD but, on the contrary, we would argue that it remains a reason to look elsewhere. The Street is valuing the stock at 15.3x FY13 EPS and, while this is not a rich multiple historically, we would take issue with the Street’s earnings estimate. Our FY13 EPS estimate of $5.29 implies a much less attractive multiple of 16.8x. Ultimately,

MCD November Sales Preview

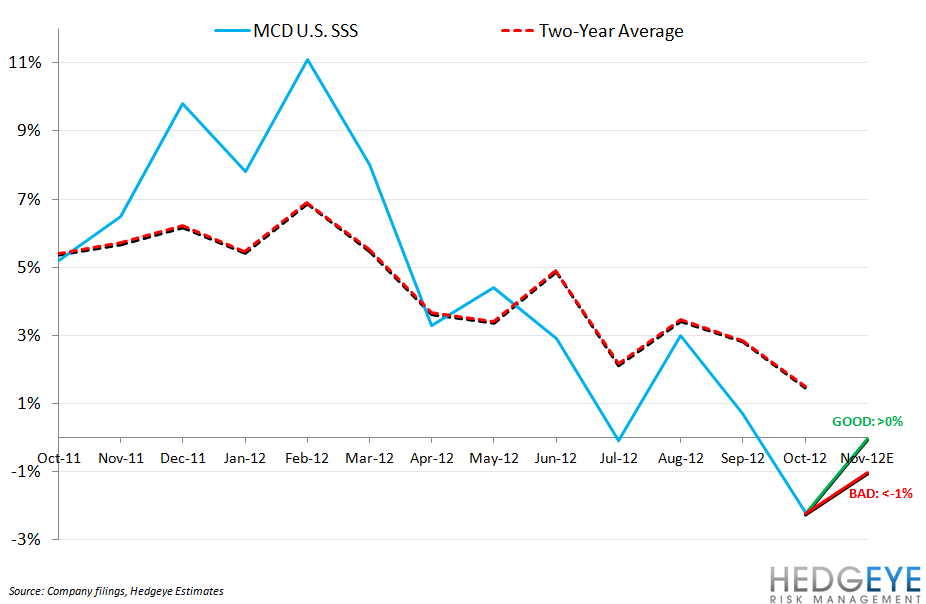

McDonald’s reports November sales on Monday morning before the market open. Consensus is calling for a sequential acceleration in two-year average trends in November.

Below we go through what we would view as good, bad, or neutral comparable restaurant sales numbers for McDonald’s three regions in November. For comparison purposes, we have adjusted for historical calendar and trading day impacts (but not weather).

Compared to November 2011, November 2012 had one additional Thursday, one additional Friday, one less Tuesday, and one less Wednesday. We expect this to have a modestly positive impact on the headline numbers for November although some negative impact will be felt in the U.S. from Sandy.

United States – facing a compare of 6.5%, including a calendar shift of 0.3%, varying by area of the world:

GOOD: A positive print would be received as a strong result as, on a calendar-adjusted basis, it would imply acceleration in two-year average trends from October. In October, performance in the U.S. was negatively impacted, according to management, by “modest consumer demand and heightened competitive activity offset the impact of local Dollar Menu advertising, the Monopoly promotion, and the recent launch of the Cheddar Bacon Onion premium sandwiches.” We believe that the heightened competitive activity in QSR is likely to ramp further over the coming months and quarters.

NEUTRAL: A print between -1% and 0% would imply calendar-adjusted two year average trends roughly flat versus October. While the first chart of this post implies an over-bearishness on the part of consensus, self-inflicted wounds on MCD’s part lead us to conclude that slower same-restaurant sales growth is possible from here.

BAD: Same-restaurant sales growth less than -1% would imply a sequential deceleration in two-year average trends in the U.S. from what was a disappointing month in October. We would expect the stock to react negatively to this print.

Europe – facing a compare of 6.5%, including a calendar shift of 0.3%, varying by area of the world:

GOOD: A positive print would be received as a strong result as, on a calendar-adjusted basis, it would imply acceleration in two-year average trends from October. Performance in Europe was hampered by economic uncertainty in November that has continued, if not worsened, in November. This morning, the Bundesbank slashed a percentage point off its forecast for economic growth in Germany next year. We expect broad-based sluggishness to persist in Europe for MCD.

NEUTRAL: A print between -1% and flat would be received as neutral by investors as it would imply calendar-adjusted two year average trends roughly flat versus October.

BAD: Less than -1% same-restaurant sales growth would imply, on a calendar-adjusted basis, trough two-year average trends for the year in Europe.

APMEA – facing a compare of 8.1%, including a calendar shift of 0.3%, varying by area of the world:

GOOD: A print of -0.5% or better in APMEA would be a positive result for MCD. We are not expecting much from APMEA this month given the worse-than-expected commentary from YUM on its China business.

NEUTRAL: A print between -1.5% and -0.5% would be received as neutral by investors as it would imply calendar-adjusted two year average trends roughly flat versus October.

BAD: Same-restaurant sales growth slower than -1.5% in November would imply sequential deceleration in two-year average trends in APMEA and would likely be received negatively by investors.

Howard Penney

Managing Director

Rory Green

Analyst