Back to Normal / Tailwinds Ahead

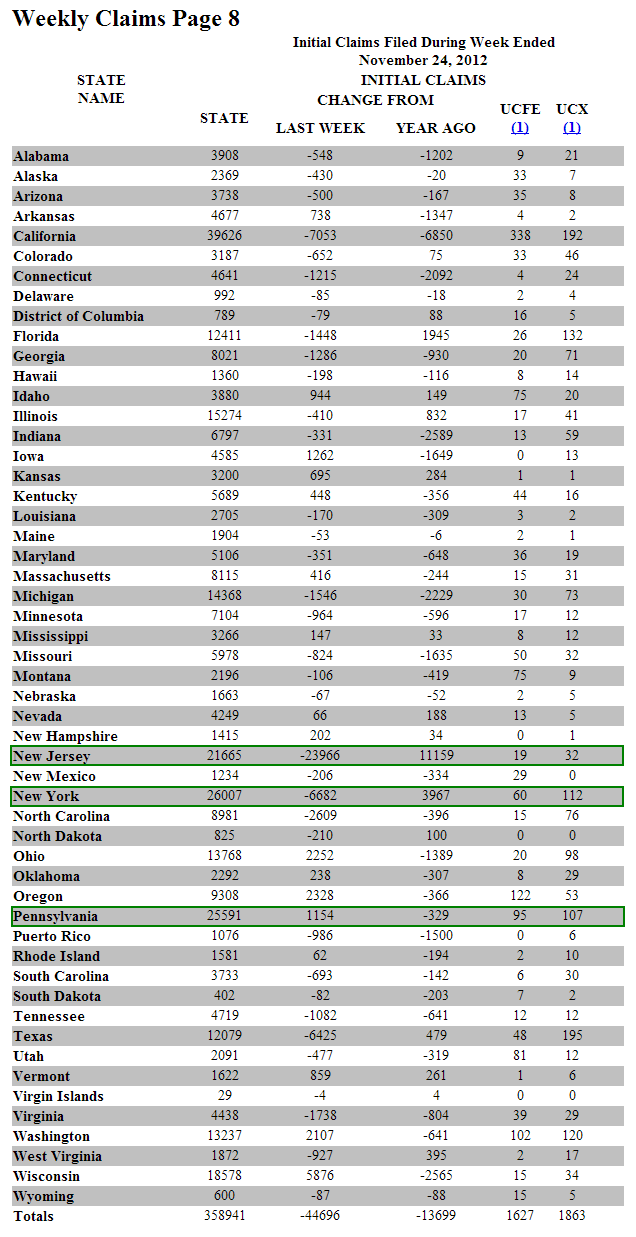

Initial claims are now essentially back to pre-Sandy levels. We show this in the first chart below. For the last few weeks we've been looking at state level claims data for NY, NJ and PA. State level data is released on a one-week lag relative to the national data. Two weeks ago, NY, NJ and PA accounted for 20.3% of total jobless claims, while accounting for 13.0% of the population. That difference, 7.3%, is down from 12.4% in the previous week. If we adjust the claims number from two weeks ago, 393k, for this over-representation we find normalized claims should be around 366k (393k / 1.073). This morning's print of 370k is consistent with that estimation.

We expect that claims should start to resume their normal behavior in the coming weeks. As a reminder, we continue to expect a seasonality-driven tailwind to benefit the data through the end of February. This, combined with our bullish view on housing, should provide an ongoing top-down tailwind for the sector.

The Numbers

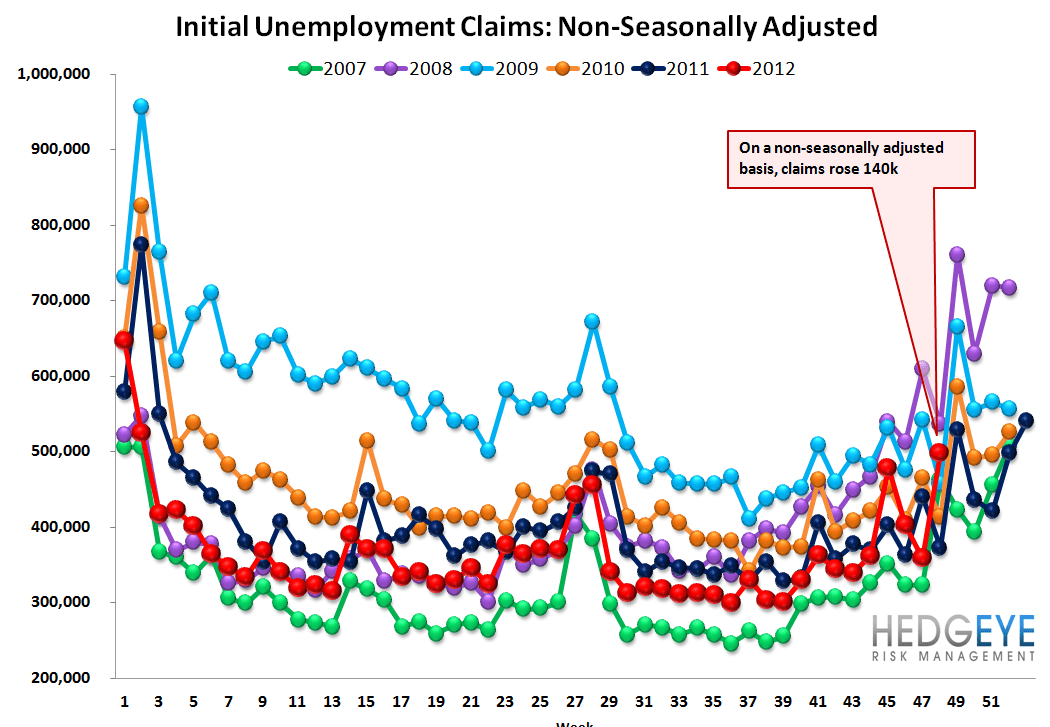

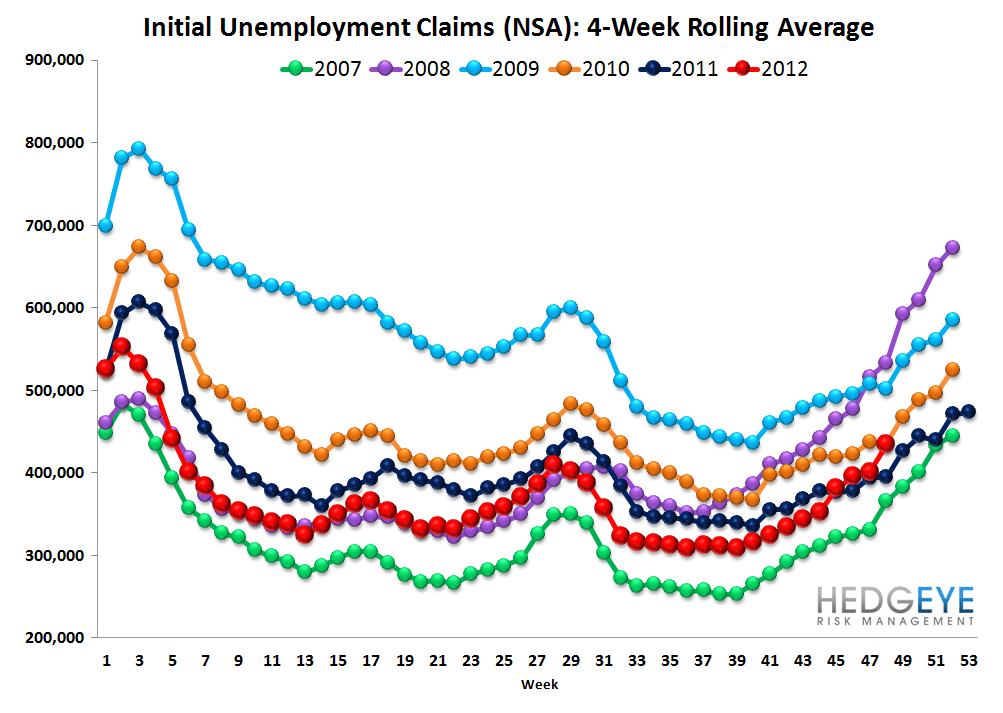

This week initial jobless claims fell 23k to 370k from 393k. The prior week's number was revised up by 2k to 395k. Incorporating this upward revision, claims were lower by 25k. Rolling claims, meanwhile, rose 2.25k WoW to 408k and non-seasonally adjusted claims rose 140k to 499k. The rolling series, both SA and NSA, are obviously reflecting the Sandy distortion on a lag. We expect that one month from now they will fully normalized.

Yield Spreads

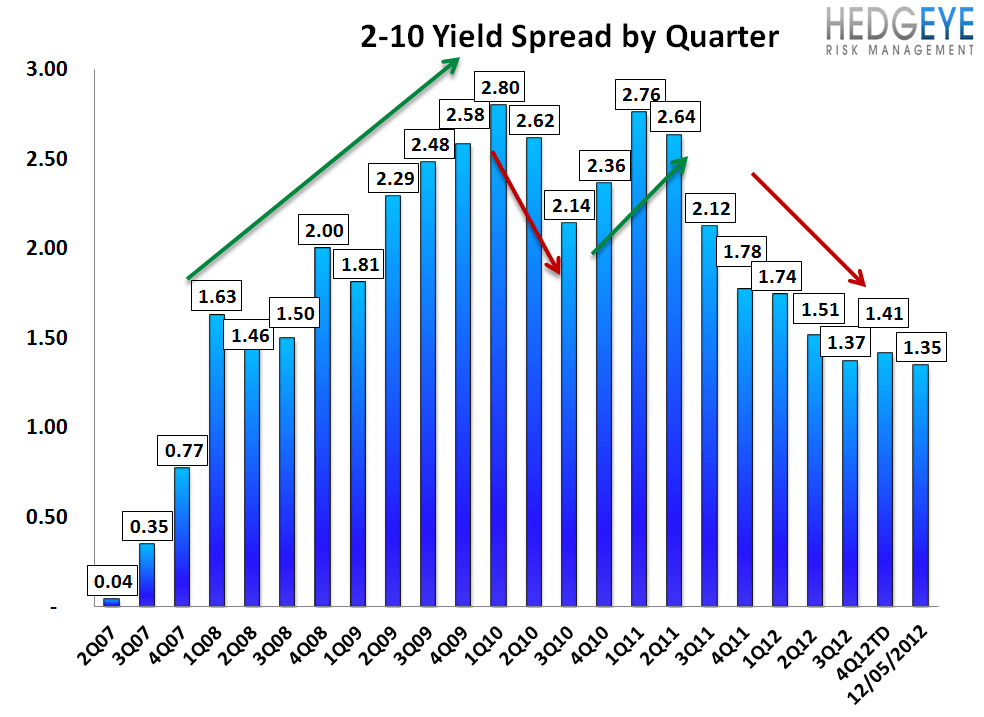

The 2-10 spread fell 1 basis point WoW to 135 bps. 4QTD, the 2-10 spread is averaging 1.41%, which is up 4 bps relative to 3Q12.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over multiple durations.

Joshua Steiner, CFA

Robert Belsky