TODAY’S S&P 500 SET-UP – December 6, 2012

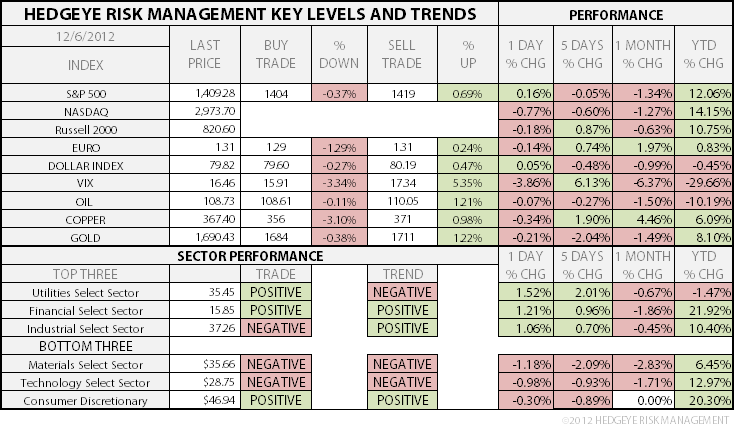

As we look at today's setup for the S&P 500, the range is 15 points or 0.37% downside to 1404 and 0.69% upside to 1419.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.34 from 1.35

- VIX closed at 16.46, 1 day percent change of -3.86%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: Bank of England interest rates announcement

- 7:45am: ECB interest rate announcement

- 7:30am: Challenger Job Cuts Y/y, Nov. (prior 11.6%)

- 8am: RBC Consumer Outlook Index, Dec. (prior 48.9)

- 8:30am: Initial Jobless Claims, Dec. 1 est 380k (prior 393k)

- 8:30am: ECB’s Draghi holds news conference

- 9:45am: Bloomberg Consumer Comfort, Dec. 2 (prior -33)

- 11am: U.S. Treasury to announce plan for auctions of 1Y bills, 3Y notes, 10Y notes, 30Y bonds

- 11am: Fed to purchase $1.5b-$2.25b notes due 2/15/36 11/15/42

- 12pm: Household Change in Net Worth, 3Q (prior -$322b)

- 2:00pm: Fed to purchase $4.25b-$5.25b notes due 12/31/18 11/15/20

GOVERNMENT:

- Obama, first family attend National Christmas Tree lighting

- Obama, Romney presidential campaigns file last spending reports

- Senate Judiciary to vote on collection of location data from companies such as Apple, Google

- FedEx CEO Frederick Smith speaks at Economic Club of Washington

- Recreational marijuana legalized in Washington state

WHAT TO WATCH

- Euro area pushed into recession as trade slows, spending drops

- France sells bonds at record-low yields

- HTC to make quarterly royalty payments to Apple based on vol.

- Zynga files with Nevada to operate online games w/ real money

- UPS said to offer remedies in 13 countries to save TNT deal

- FTC says Motorola Mobility shouldn’t get injunction in patent suit against Apple

- Carl Icahn reports lowered stake in Oshkosh

- Garmin to replace R.R. Donnelley on S&P 500

- Boeing says 787 Dreamliner didn’t lose power during generator failure

- Intel CEO says favors internal candidate to take over top spot

- Apple may try to get ban on future Samsung smartphone products; patent infringement case to be heard by judge today

- China Mobile says Apple must discuss benefit sharing on IPhone

- SAC’s Steinberg said to be unindicted co-conspirator at trial

EARNINGS:

- Canadian Imperial Bank of Commerce (CM CN) 5:35am, C$1.99

- Smithfield Foods (SFD) 6:00am, $0.43

- Toronto-Dominion Bank (TD CN) 6:30am, C$1.81

- H&R Block Inc (HRB) 7:00am, $(0.41)

- Lululemon Athletica (LULU) 7:15am, $0.37

- Dollarama Inc (DOL CN) 7:30am, C$0.70

- National Bank of Canada (NA CN) 7:30am, C$1.93

- Uti Worldwide (UTIW) 8:00am, $0.24

- Esterline Technologies Corp (ESL) 4:00pm, $1.59

- Cooper Cos (COO) 4:01pm, $1.55

- Forest City Enterprises (FCE/A) 4:02pm, $0.01

- Palo Alto Networks (PANW) 4:05pm, $0.03

- Harry Winston Diamond (HW CN) 5:00pm, $0.12

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – both Brent and WTIC continue to make lower-highs on low volume rallies – and both remain in Bearish Formations in my model. We expanded our Commodities Bubble short positioning yesterday to US Energy stocks (XLE) and Russia (RSX); the sell side’s top rated Sector is still Energy “because it’s cheap”, using the wrong commodity prices of course.

GOLD – not good. My intermediate-term TREND line of $1711 is now broken and being confirmed on the downside. Gold Miners getting hammered as they remain over-owned by funds seeing redemptions.

- World Food Prices Fell a Second Month in November on Oils, Grain

- Russian Wheat Facing Coldest Winter in Two Decades: Commodities

- Copper Declines on Concerns About Global Economic Growth

- Oil Trades Near One-Week Low as U.S. Distillate Supplies Surge

- Freeport’s Oil-Gas Bet Prompts Biggest Slump in 4 Years: Energy

- Morgan Stanley Backs Gold, Corn, Soybeans as Best Picks in 2013

- Sugar Falls on Mounting Speculation of Oversupply; Coffee Climbs

- Gold Declines for Third Day Toward One-Month Low as Dollar Gains

- Palm Oil Reserves in Malaysia Seen Holding Near Highest Ever

- Mississippi Water Level Buoys Odds of Keeping River Open Longer

- Japan Buys Most Milling Wheat in Four Months From U.S., Canada

- OPEC’s Biggest Cut Since 2009 Looms Next Year: Energy Markets

- Gold Set to Return to Run of Records Next Year: Chart of the Day

- Soybeans Gain as USDA May Report Lower South American Outlook

CURRENCIES

EUROPEAN MARKETS

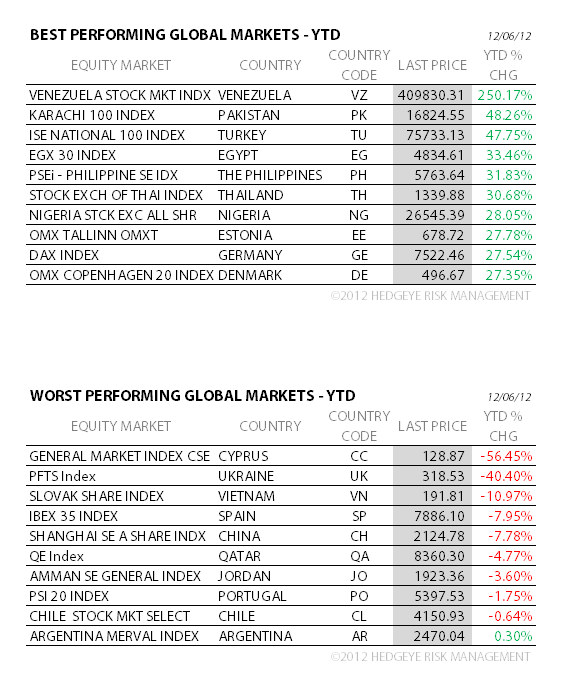

GERMANY – who cares what the Dow is “up YTD” when you could be up +28% YTD owning the German DAX, powering past the September closing highs? With the SP500 -4.4% from the Bernanke SEP Top, this +1.1% move this morning in Germany is definitely the macro move of the morning.

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team