We’re two weeks away from Nike’s quarter, and just over three weeks away from the deadline for the swarm of ‘special’ dividends that will fall into the 2012 tax year. There are factors for Nike that are worth considering.

- The company has about $3.2bn in cash, or $7ps, waiting to be deployed.

- There’s another $2bn in FCF over the next 12 months, or $4.40ps. Combined with current holdings, we’ve got net pro-forma cash balance of $5.2bn, or $11.40 per share. That’s 11.75% of NKE’s equity value.

- Though we still think that Nike is grossly under-levered with only $364mm in debt on a $15.1bn balance sheet, it’s unrealistic to think that it will take its cash to zero due to its sheer conservatism – especially in that it faces the same hurdles the same hurdles as other multi-nationals with repatriating cash with a tax penalty.

- But it has another characteristic that others do not…and that is the fact that management owns 21% of the stock, with Phil Knight himself owning 18% (with full control of the Board due to super voting rights in Class A/B share structure). Mr. Knight has been a very conservative seller of the stock over time, and sold hardly no shares since the first of several small 10b5-1s in 2005.

- We could comfortably leave Nike with $2.5bn in cash on the balance sheet over 12 months, leaving $2,000-$3,000 to distribute today. That accounts for around 5-6% of Nike’s current equity value. A $2bn dividend would be a $360mm paycheck for Phil Knight.

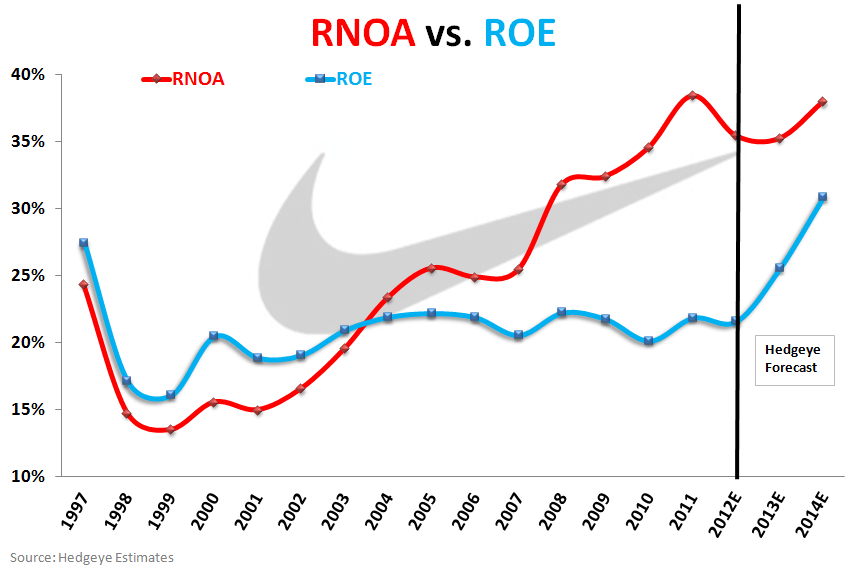

We don’t have a crystal ball as to the event or magnitude for NKE, but we see three distinct buckets of companies issuing these dividends. 1) Those that COULD, 2) Those that SHOULD, and 3) Those that THINK that they have the resources to do so, but will be regretting it in a year (like GES). Nike has ample opportunity for reinvestment in the business, but its ROE vs ROIC trend definitely suggests that it SHOULD give some back to shareholders.