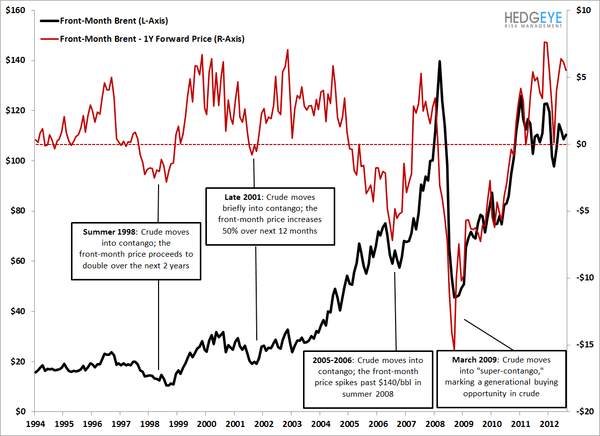

Brent crude oil prices will likely remain depressed for some time as futures contracts for oil are currently in backwardation. That means that futures contracts further out in time (i.e. January 2013, February 2013, etc.) are lower than today’s current price. That means you can lock in lower prices for oil in the future today. The opposite is called contango, which is what we saw back in 2009.

Normally, prices should reflect current supply, demand, inventory and convenience yield. The curve occasionally moves into backwardation when the convenience yield exceeds the storage and interest costs; that puts a premium on owning oil now.

The consensus would normally think that backwardation signals higher oil prices are coming; we argue the opposite. From Hedgeye Energy Sector Head Kevin Kaiser:

“In our view, consensus considers a backwardated futures curve as a bullish signal for future spot prices. We have read and heard this argument many times from highly-regarded energy analysts and investors. We argue the opposite: if the curve is backwardated then the demand or supply shock has either already happened or is highly-anticipated, and we would expect spot oil prices to fall in the future. Conversely, a steep contango would be a compelling buying opportunity, as it implies low convenience yield that is likely to rebound.”