Darden is down today on the company issuing EPS guidance for 2QFY12 of $0.25-0.26. We have been bearish on DRI since July and we believe the indications are that our thesis is playing out.

Tectonic Shift in Expectations

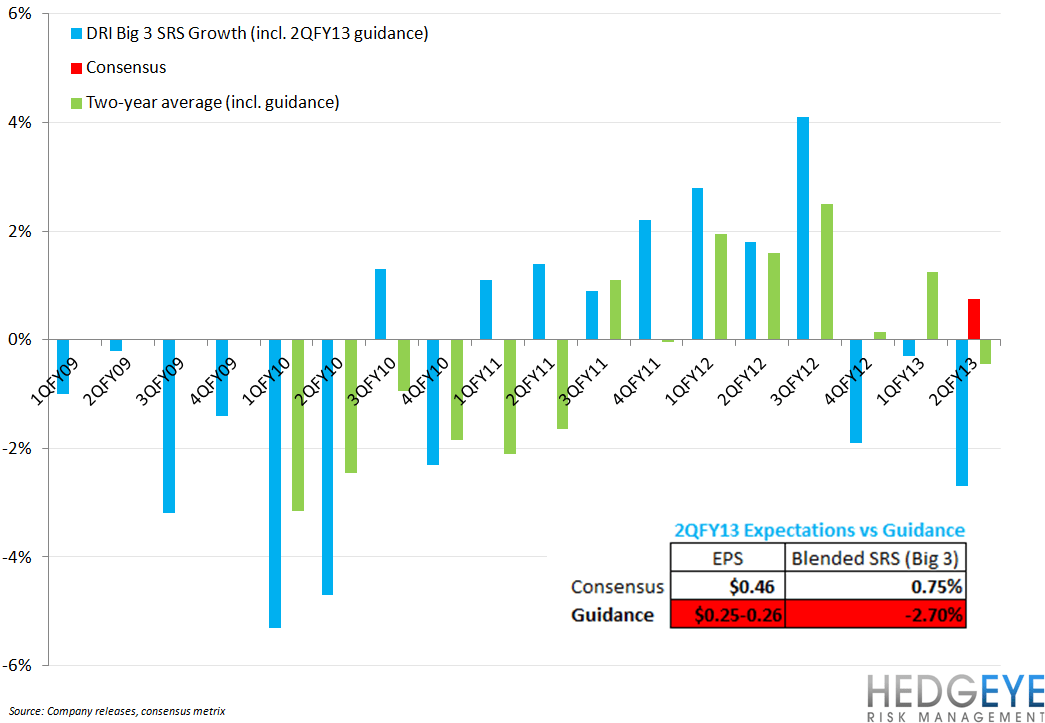

Based on poor results for 2QFY13 to-date, Darden revised its FY13 combined U.S. same-restaurant sales growth (OG, RL, LH) guidance from +1-2% to -1% this morning. Sales growth guidance for the year was lowered to 7.5-8.5% versus 9-10% prior while EPS guidance was lowered to $3.29-3.49 versus $3.76-3.90 (consensus is at $3.87).

No Easy Way Out

CEO Clarence Otis, commenting in this morning’s release, stated that the quarter’s offers were “largely consistent in nature with what we've promoted successfully in the past” but that the promotions “not resonate with financially stretched consumers as well as newer promotions from competitors”.

We continue to hear the same messages from management as its hit-and-miss top-line record continues. In fact, as we stated in our Black Book in July, “lately, it has been more miss than hit”. More promotion-dependant sales are failing to provide the consistency that investors are seeking in a stock with Darden’s reputation. The CMO leaving in November was a sign that things were not going too well

Pleasing All of the Investors, All of the Time

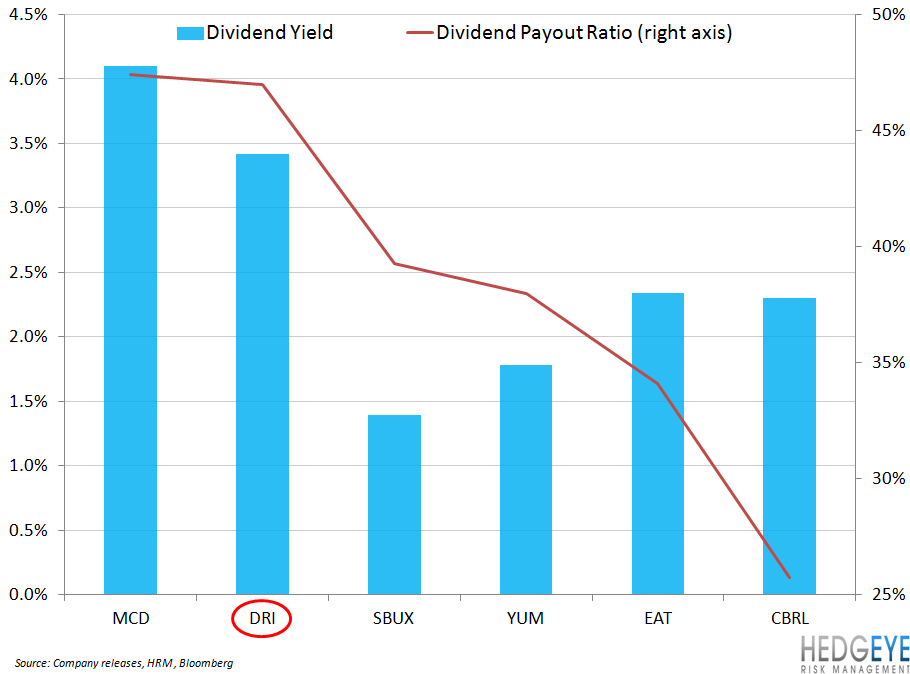

One of the core facets of Darden thesis has been that it is improbable that the company can continue to appeal to such a wide array of investors through such a wide array of attributes. Financing unit growth at a time when the existing system’s performance is less-than-reassuring seems to be an attempt to be everything to everyone: paying dividends, buying back stock, and continuing to grow while maintaining a strong balance sheet.

We believe that Darden’s true free cash flow (CFO less capex, dividends, buybacks) will remain under pressure. A reduction in the company’s dividend could be forthcoming absent a turnaround at its largest two chains, Olive Garden and Red Lobster.

Our contention has been, and remains, that management is focusing on too many things at once. A la Brinker in 2010, we would like to see this company focus on attacking the middle of the P&L. Until then, we are likely to remain bearish but will be publishing more on this stock, and casual dining, in the coming days.

Howard Penney

Managing Director

Rory Green

Analyst