“It is seldom that liberty of any kind is lost all at once.”

-David Hume

If alarm bells aren’t going off in your head this holiday season, they should be. Don’t confuse our 2012 Global Macro call for #GrowthSlowing as regressive. Being a realist is progressive. So is standing on the front lines of change.

While he had a tough time marketing his progressive free-market ideas in the 1930s and 1940s, Hayek’s lessons lived on. The aforementioned quote from Hume stands like a rock alongside one from de Tocqueville at the beginning of The Road To Serfdom. Hayek addressed his book “to socialists of all parties.”

I’m not suggesting you become a hard core Hayekian. Neither am I telling you what and/or how to think. I am just a man in a room. I’m fighting for free-market liberties like many men and women who have come before me. During this generational debate about debt, spending, and taxes, all that we ask is that you educate yourself. Liberty’s Bells are ringing.

Back to the Global Macro Grind…

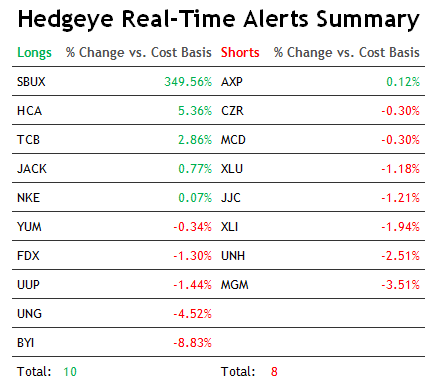

After another Monday morning littered with Greek bailout headlines, Global Equities backed off their early morning highs and closed on their lows (SP500 -0.5%). Across durations in our risk management model, Risk Ranges are getting pretty tight.

Tight can be trade-able. That’s a good thing. In Hedgeye-speak we are always talking to clients about managing the Risk Range. Once you have a repeatable process to calculate it, it’s trivial. Risk Ranges are at the bottom of the Early Look note, every day.

Risk Ranges provide us with a quantitative, probability-weighted, framework to contextualize the storytelling in the marketplace. Most stories are qualitative in nature, so having some math wrapped around what’s happening out there is helpful.

We tell stories too. We call them our Hedgeye Global Macro Quarterly Themes. For Q4, they remain as follows:

1. #EarningsSlowing

2. Bubble#3 (Commodities)

3. #KeynesianCliff

For accountability purposes, I use the hash-tag to provide you an archive of high-frequency macro data on Twitter. Being early doesn’t always make us right – but it will make you think outside the government’s centrally planned box.

While the #KeynesianCliff is annoying you, here’s an update on what used to matter to markets (#EarningsSlowing):

- For Q4 2012 so far, 78 companies have issued negative EPS guidance (29 companies have issued positive EPS guidance)

- That means 73% (78 out of 107) of the companies that have said something, said something negative, on the margin

- 73% = 2nd highest percentage of companies issuing negative EPS guidance since FactSet began tracking the data in Q1 2006

Per the lynx-eyed (and some say exotic) Darius Dale, I guess the perma-bulls would say that only 73% of companies guiding down is bullish! Relative to the worst quarter on recent record, that is (i.e. the one just reported with Q3 of 2012 = 74%).

I know, I know – since very few bulls called for both global and earnings growth to slow in Q1, blame everyone and everything but the forecasters in 2012. It’s all the government’s fault. So what we really need to do now is beg for more government.

Or do we?

The best thing that can happen to both the US and Global Consumption economy is more of Theme #2. Popping Bernanke’s Bubbles in food and energy prices would be wildly stimulative to the 71% (that’s US Consumption as a % of total US GDP).

Get consumption right, you’ll get global growth right.

That’s why I got bullish in 2009. That’s why I was bullish until January 25th of 2012 (until Bernanke decided to move 0% rates out to 2014 with more Policy To Inflate asset prices). Inflation is not growth.

“We are now so conditioned by permanent price inflation that the idea of prices falling every year is difficult to grasp. And, yet, prices generally fell every year from the beginning of the Industrial Revolution in the latter part of the eighteenth century until 1940, with the exception of periods of major war when governments inflated the money supply radically and drove up prices.” -Rothbard

The only war I see now is between the #PoliticalClass and the rest of us.

At tomorrow’s NYC Analyst Day one of the greatest innovators in America will be talking up asset price deflation in commodities. The Brooklyn born grinder (Starbucks CEO, Howard Schultz) knows how to make a buck and then hire someone with it. Now he’s staring down a futures price in coffee that’s down 50% since topping in May (see Chart of The Day).

That may not be the kind of change you are hearing from Marxist price controllers and debt/deficit spending Keynesians. That’s simply called the Fed getting out of the way for a few months. Cheers to that. Liberty’s Bells are ringing.

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1, $109.42-111.76, $3.54-3.66, $79.59-80.27, $1.29-1.31, 1.58-1.67%, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer