We’re changing our tune on Macau. While we continue to expect a strong December, there are a number of near-term hurdles that investors may not be focused on.

Slowing growth has been a worldwide theme that the Macro boys at Hedgeye have nailed. Our Macau specific analysis complemented the Macro work nicely in predicting the halting growth in GGR this summer. Following a period of accelerating growth this Fall, we’re ready to project another difficult period for Macau. Why? Well, it’s not just because we like to go against consensus. There are a few issues that we don’t think the Street appreciates fully:

- China Crackdown – The WSJ reported today that China may be tightening the screws on large cash transactions as it pursues anti-corruption measures. Obviously, this could impact the Macau VIP business which most certainly benefits from money laundering.

- Smoking Restrictions – Okay, this one people know about but we feel like they are a little too complacent regarding the potential impact.

- Plateauing Mass Hold Percentage – We don’t think people realize how much rising hold has contributed to the strong Mass growth generated over the past few years. While the current hold percentage should be sustainable, it probably won’t elevate more.

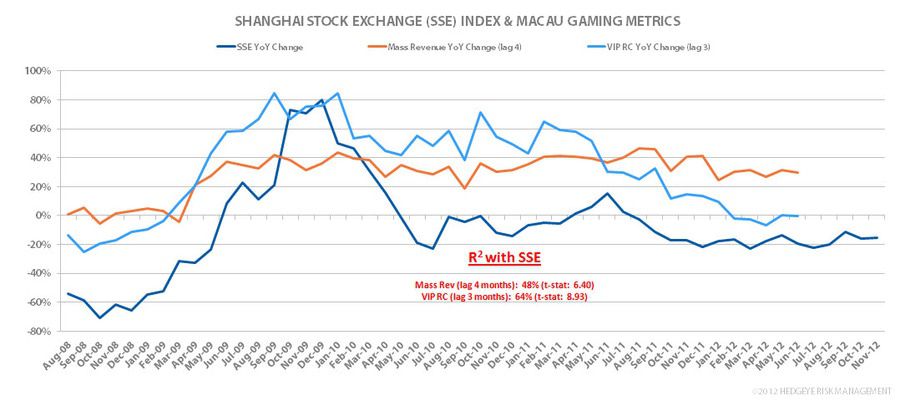

- Performance of SSE – We’ve found a statistically significant relationship between the performance of the Shanghai Stock Exchange and Macau GGR. The relationship peaks at a lag of 4-5 months which doesn’t bode well for early 2013 GGR.

CHINA CRACKDOWN ON CORRUPTION?

We’ve seen alarmist articles like this before, but we think today’s WSJ story has teeth. Certainly, the new Chinese government was going to make some noise since corruption is a big issue with the populace. While we don’t think this will be a permanent issue for the Macau operators, the junkets and VIP players are likely to lay low for at least the near-term. This will no doubt negatively impact the VIP business over the near-term.

SMOKING RESTRICTIONS

As we pointed out in our 11/12/12 post, “SMOKIN IN THE BOYS ROOM”, it looks like there will be no more delays in the 50% smoking ban for all Macau casinos. The implementation of the new smoking rules will be enforced in early January. Once implemented, we believe there will be a major impact on the main gaming floor, particularly for mass-centric LVS and SJM. Lower table efficiency and higher labor costs will also result from this new smoking rule. Investors should begin to discount an impact this month.

PLATEAUING MASS TABLE HOLD PERCENTAGE

On the mass side, there may not be more luck coming for the casinos. With Mass hold % plateauing, revenue growth is likely to slow. As we wrote about in our 11/26/12 post, “CHART DU JOUR: THE END OF THE MASS HOLD TAILWIND?” over the past four years, mass revenue growth has significantly outpaced volume growth as mass hold rates climbed higher and higher.

True, Mass hold % can be difficult to analyze as there are many factors. One factor is whether or not the casino includes cage cash (and not just table cash) in its calculation of drop. That has probably had an impact as more chips are now taken at the cage than before due to security measures implemented by some of the casinos.

Mass hold % has stabilized over the past 3 quarters and increases over time were achieved through dealer efficiencies, better targeted marketing, and table rationalization and productivity. However, the smoking ban could have a negative impact on productivity and efficiencies which would could also negatively impact Mass hold rate. That also means future mass revenue growth will rely more on volume growth, which hasn’t been nearly as robust by a wide margin as seen in the chart below.

PERFORMANCE OF SSE

An update of our analysis seen in “MACAU: THE SSE MATTERS” (9/5/2012) continues to show that the horrendous performance of the Shanghai Stock Exchange (SSE) does not bode well for Macau gaming revenues. VIP RC (on a 3-month lag) has a 64% correlation with SSE, while Mass revenues (on a 4-month lag) has a 48% correlation with SSE. This would suggest slowing growth in Macau GGR for the next 6 months.

OUR PROJECTIONS

The chart clearly displays our view of slowing growth. While most investors are focused on the VIP slowdown – a fairly long trend already underway – not enough seem to be paying attention to the presence of some potentially meaningful governors on Mass growth. The smoking ban, moderating Mass hold percentage, and the recent lousy performance of the SSE could restrict growth.

The rate of Mass growth should continue to decelerate all year long, culminating in full year YoY growth of only 9% versus 32% in 2012, according to our model. By mid-year, VIP growth could begin to exceed Mass in some months. If we’re right, 2013 margins and EBITDA could disappoint analysts given the significantly better profitability inherent in the Mass business. VIP is always a wild card and it remains to be seen how long of an impact the reported Beijing crackdown could have on Macau.