The market move in GMCR on its most recent earnings print was emphatic but there was nothing in the 4Q12 results that led us to believe that our bearish stance on the stock should change. We have been bearish on the stock since early 2011.

New CEO

Brian Kelley, formerly of KO, is a respected executive and showed wise judgment, in our view, to get himself paid up front. The company’s cash flow situation is yet to be resolved and there are several potentially serious issues ahead in the form of SEC investigations and class action law suits. Green Mountain has been in a downward spiral and investors will be watching closely over the coming quarters to see if Kelly can formulate a plan to solidify the company’s role in the coffee market. As things stand, there is a large number of questions related to competitive pressures in the brewer segment, margin pressure in the K-Cup business, and the potential for the aforementioned investigations and law suits to yield negative outcomes for the company.

4Q12 Numbers Flattered to Deceive

GMCR reporting 4Q12 EPS of $0.64 versus consensus of $0.48, along with the FY13 guidance raise, pushed the stock higher on Tuesday after the market close. We believe that much more clarity is required before we get comfortable with an expected earnings number for FY13.

Pulling the Goalie?

- SG&A saved the day in 4Q12. A 220bps decline in SG&A expenses was instrumental in GMCR offsetting the negative margin impact of increased promotional activity

- Promotional activity is not a sustainable driver of sales for a business that is already seeing its margins decline

Positives in 4Q12

- Inventory was brought under control for the first time in 9 quarters

- FCF was positive as capex came in $100m lighter than expected

Issues Facing GMCR in FY13

- Competitive pressures due to patent expiration: The company reiterated several times that this is not a significant issue for the company but the data tells a different story.

- Negative K-Cup mix (-2% in 4Q): Lower ASPs and mix with partner brands should bring further mix declines going forward as we are only in early stages of transition from wholly-owned brands to private label brands.

- Promotional Activity: Gross margins declined 230 bps helped by 100 bps of coffee cost benefit. Starbucks is taking advantage of favorable input costs to make strategic acquisitions while Green Mountain is using the COGs environment to discount product.

- Starbucks’ Commitment Issues: We doubt that SBUX has committed itself to a long-term contract with GMCR. Even if that is the case, we know SBUX is not shy when it comes to extricating itself from relationships it does not see as being to its advantage. The Starbucks Investor meeting on December 5th could shed light on this relationship.

Other Red Flags

Accounting Signals? The surge in deprecation in as a percentage of sales is a potential red flag. Is the company changing its accounting practices with respect to depreciation?

Vue Appeal? The company reported $10mm in Keurig Vue sales, down from $20mm in F3Q. While the company insists the brand will be a slow build, brewer sales declining by 50% sequentially indicates that the rollout has been underwhelming.

Margins Rolling Over? Neither lower coffee costs nor managing SG&A constitutes a sustainable strategy for expanding margins.

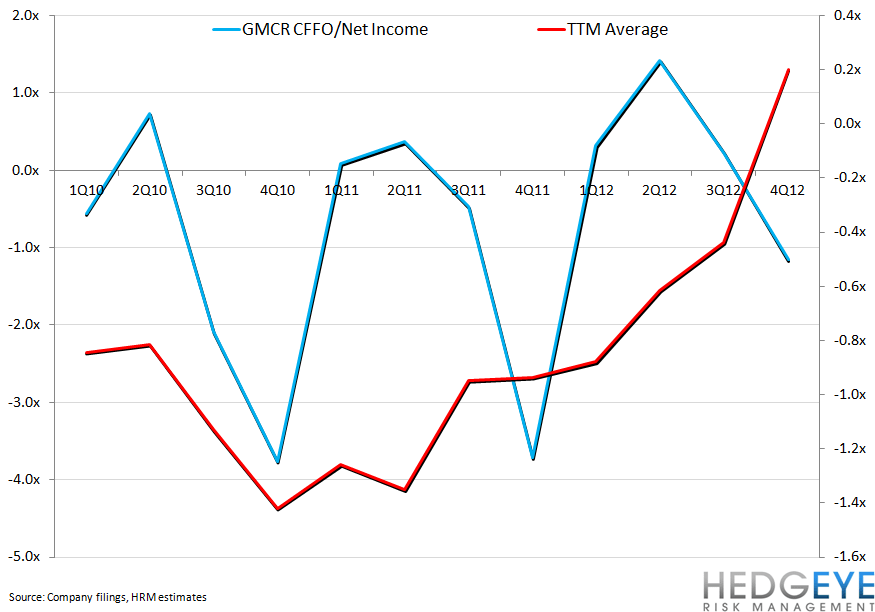

Cash Flow Slow Drip? CFFO/Net Income is a key metric for Green Mountain as it indicates the proportion of earnings that are yielding cash. A higher ratio relative to the industry can indicate more conservative accounting, signaling a sustainable level of income. Any ratio that is nearly flat or negative is generally a concern for us. The company has moved out of the “danger zone” over the past few quarters but we will continue to monitor this metric.

Howard Penney

Managing Director

Rory Green

Analyst