-- For specific questions on anything Europe, please contact me at to set up a call.

Asset Class Performance:

- Equities: The STOXX Europe 600 closed up +0.9% week-over-week vs +4.0% last week. Top performers: Austria +2.7%; Hungary +2.2%; Czech Republic +2.1%; Switzerland +1.6%; Netherlands +1.5%; Germany +1.3%; Sweden +1.3%; Poland +1.3%; Italy +1.1%. Bottom performers: Cyprus -12.2%; Greece -4.2%; Portugal -1.3%. [Other: UK +0.8%].

- FX: The EUR/USD is up +0.22% week-over-week vs +1.84% last week. W/W Divergences: HUF/EUR +0.45%; CZK/EUR +0.40%; RUB/EUR +0.38%; PLN/EUR +0.30%; TRY/EUR +0.18%; DKK/EUR -0.03%; CHF/EUR -0.09%; GBP/EUR -0.28%; NOK/EUR -0.39%; SEK/EUR -0.66%.

- Fixed Income: The 10YR yield for sovereigns were down across the region week-on-week. Spain declined the most at -30bps to 5.38%, followed by Portugal -29bps to 7.62%, Italy -25bps to 4.53%, Greece -23bps to 16.21%, and Belgium -22bps to 2.07%. France fell -11bps to 2.05% and Germany declined -5bps to 1.37%.

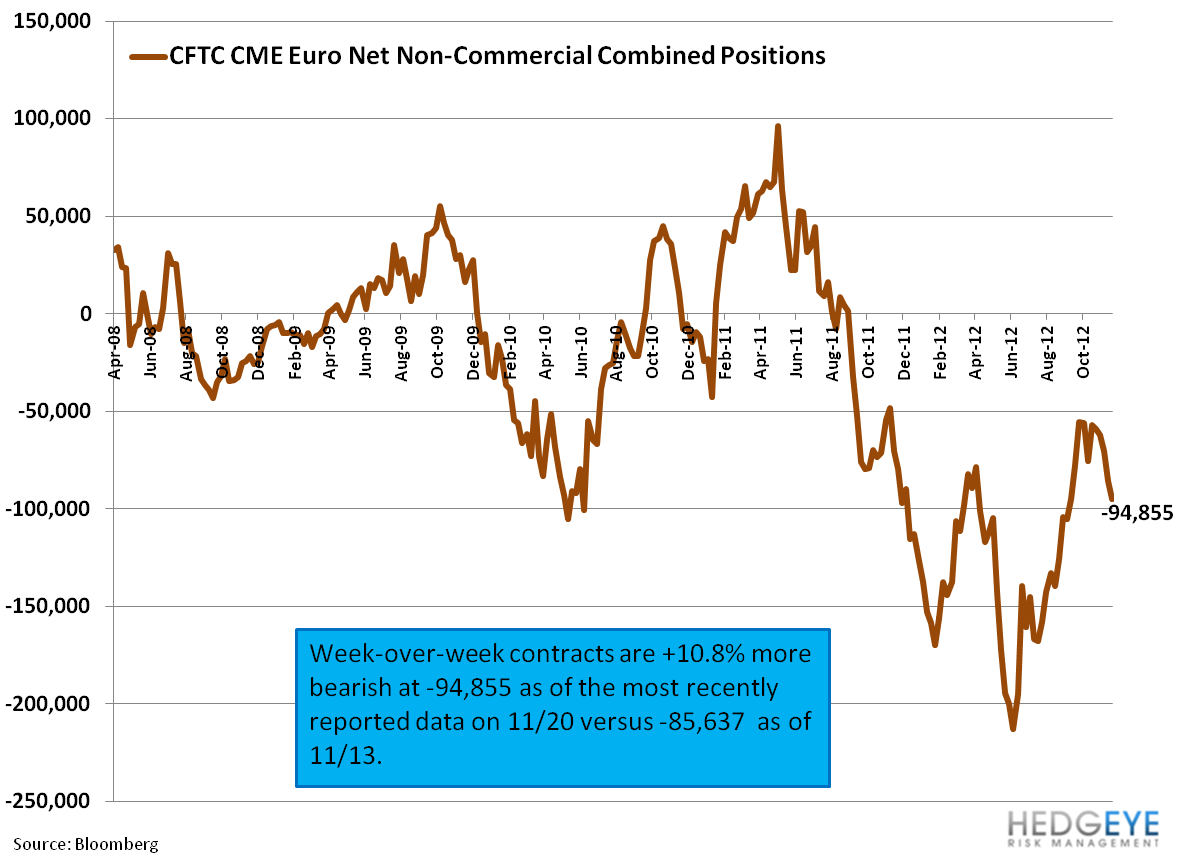

EUR/USD: Our TRADE range is $1.29 – 1.31 with a TREND resistance of $1.31.

- Our call - the EUR/USD will trade within our quantitative levels and reflect much of the daily headline risk (from Spain, Greece, and Italy in particular), however ECB President Mario Draghi’s September announcement that “the ECB is ready to do whatever it takes to preserve the euro” and the resolve of Eurocrats to maintain the Union will prevent levels falling anywhere near parity.

- We believe there is a high likelihood that no significant policy action comes in the remaining weeks of 2012, which could support the band the cross has been trading in over the last weeks.

Padding Greece’s Pocket:

For updated thoughts on Europe, and in particular Greece’s most recent hand-out, see Thursday’s Early Look Titled Europe’s Shell Game.

The European Week Ahead:

Saturday - Beginning of the Russian Presidency of G20

Sunday - Nov. UK Lloyds Business Barometer and Hometrack Housing Survey

Monday - ECB Governing Council Meeting; Eurogroup Meeting in Brussels; Nov. Eurozone PMI Manufacturing – Final; Nov. Germany PMI Manufacturing – Final; Nov. UK PMI Manufacturing, BRC Sales Like-For-Like; Nov. France PMI Manufacturing – Final; Spain Manufacturing PMI; Nov. Italy PMI Manufacturing, Budget Balance, New Car Registration; Greece Manufacturing PMI

Tuesday - Oct. Eurozone PPI; Nov. UK PMI Construction, BRC Shop Price Index; Nov. Spain Unemployment

Wednesday - Nov. Eurozone PMI Composite and Services Final; Oct. Eurozone Retail Sales; Nov. Germany PMI Services – Final; UK Chancellor Osborne Makes Autumn Statement in Commons; Nov. UK Official Reserves, PMI Services; Nov. France PMI Services – Final; Spain Services PMI; Oct. Spain Industrial Output; Nov. Italy PMI Services

Thursday - ECB Announces Interest Rates, ECB Deposit Facility Rate; 3Q Eurozone Household Cons, Gross Fix Cap, Government Expend and GDP – Preliminary; Oct. Germany Factory Orders; UK BoE Announces Interest Rates, BoE Asset Purchase Target; Nov. UK New Car Registration; Oct. UK Visible Trade Balance, Total Trade – Preliminary; 3Q France ILO Unemployment Rate; Sep. Greece Unemployment Rate

Friday - Oct. Germany Industrial Production; Nov. Germany Wholesale Price Index (Dec. 7-12); 3Q Germany Labor Costs Workday Adj, Labor Costs Seas. Adj; Dec. UK CBI Trends Total Orders, Trends Selling Prices and Reported Sales (Dec. 7-15); Nov. UK BoE/GfK Inflation Next 12 Mths, NIESR GDP Estimate; Oct. UK Industrial Production, Manufacturing Production; Oct. France Central Govt. Balance, Trade Balance; 3Q Greece GDP - Final

Extended Calendar:

DEC 12-13 – First public consultation between the Russian government, B20 Coalition and international civil society representatives on G20 agenda for 2013 (in Moscow)

DEC 20 – ECB Governing and General Council Meeting

APR 2013 – Parliamentary elections in Italy

MAY 2013 – Presidential elections in Italy

Call Outs:

Spanish Banks - The European Commission approved the restructuring plans for four Spanish banks - Bankia, NCG Banco, Catalunya Banc and Banco de Valencia (which will be sold to CaixaBank). The approval will allow the banks to receive aid from the ESM.

Spanish banks - Cut their government bond holdings by €5.2B in October after an €8.8B increase in September. Total sovereign holdings, adjusted by market value, fell to €253.7B last month.

Spain - Bankia said that holders of preferred shares will have to take a write-down of 39%, while holders of perpetual subordinated debt will face a write-down of 46% and holders of subordinated debt with a maturity date will have to take a loss of 14%. According to estimates by Barclays, ~€30B of these products were sold to individual savers/retail investors before the crisis by small Spanish banks, including Bankia.

Spain - Bank of Spain noted that Spain experienced a capital inflow of €31B in September (August saw an outflow of €11.8B).

OECD - Slashes 2013 growth forecast for advanced economies (1.4% versus 2.2% forecast in May).

ECB and OMT - Vice President Constancio said that the central bank expects Madrid to apply for support, triggering the OMT. While he noted that this is the ECB's base scenario for Spain, he reiterated that it is up to the Rajoy government to make a request.

UK - Bank of Canada Governor Mark Carney was named head of the Bank of England.

Data Dump:

Eurozone Services Confidence -11.9 NOV (exp. -12.5) vs -12.1 OCT

Eurozone Business Climate -1.19 NOV (exp. -1.60) vs -1.61 OCT

Eurozone Industrial Confidence -15.1 NOV (exp. -17.1) vs -18.3 OCT

Eurozone Economic Confidence 85.7 NOV (exp. 84.5) vs 84.3 OCT

Eurozone Consumer Confidence -26.9 NOV Final (inline)

Eurozone CPI 2.2% NOV Y/Y vs 2.5% OCT

Eurozone M3 3.9% OCT Y/Y vs 2.6% September

Eurozone Unemployment Rate 11.7% OCT vs 11.6% SEPT

Germany Unemployment Rate 6.9% NOV vs 6.9% OCT

Germany Unemployment Change 5K NOV vs 19K OCT

Germany Retail Sales -0.8% OCT Y/Y (exp. -0.3%) vs -3.4% SEPT [-2.8% OCT M/M (= most in ~4yrs) (exp. -0.4%) vs 0.5% September]

Germany GfK Consumer Confidence 5.9 DEC (exp. 6.2) vs 6.1 NOV

Germany CPI 2.0% NOV Prelim Y/Y (inline) vs 2.1% OCT

Germany Import Price Index 1.5% OCT Y/Y vs 1.8% September

France Consumer Confidence 84 NOV vs 84 OCT

France Producer Prices 2.9% OCT Y/Y vs 2.9% SEPT

France Consumer Spending -0.5% OCT Y/Y vs -0.3% September

UK Q3 GDP Preliminary -0.1% Y/Y vs -0.5% in Q2 [1.0% Q/Q vs -0.4% in Q2]

UK Nationwide House Prices -1.2% NOV Y/Y vs -0.9% OCT

UK M4 Money Supply -3.2% OCT Y/Y vs -3.7% September

UK GfK Consumer Confidence -22 NOV (exp. -30) vs -30 OCT

Italy Consumer Confidence 84.8 NOV (exp. 86.3) vs 86.2 OCT [new record low]

Italy Unemployment Rate 11.1% OCT vs 10.8 SEPT

Italy CPI 2.6% NOV Y/Y vs 2.8% OCT

Italy PPI 2.6% OCT Y/Y vs 2.8% SEPT

Italy Hourly Wages 1.5% OCT Y/Y vs 1.4% SEPT

Italy Business Confidence 88.5 NOV vs 87.8 OCT

Italy Economic Sentiment 76.4 NOV vs 77.1 OCT

Spain Retail Sales -8.4% OCT Y/Y (exp. -10.0%) vs -12.7% September

Spain Total Housing Permits -51.3% SEPT Y/Y vs -31.7% AUG

Spain CPI 3.0% NOV Prelim. Y/Y vs 3.5% OCT

Spain Mortgages on Houses -32.2% SEPT Y/Y vs -28.5% AUG

Switzerland Q3 GDP 1.4% Y/Y vs 0.3% in Q2 [0.6% Q/Q vs -0.1% in Q2]

Switzerland KOF Swiss Leading Indicator 1.50 NOV (exp. 1.60) vs 1.64 OCT

Switzerland UBS Consumption Indicator 1.31 OCT vs 1.04 SEPT

Austria Producer Prices 0.7% OCT Y/Y vs 0.7% SEPT

Belgium CPI 2.26% NOV Y/Y vs 2.79%

Ireland Property Prices -8.1% OCT Y/Y vs -9.6% SEPT

Portugal Consumer Confidence -59 NOV vs -55.3 OCT

Portugal Economic Climate -5 NOV vs -4.6 OCT

Portugal Industrial Production -4.3% OCT Y/Y vs -9.5% September

Portugal Retail Sales -6.9% OCT Y/Y vs -5.9% September

Sweden Manufacturing Confidence -18 NOV vs -16 OCT

Sweden Economic Tendency Survey 86 NOV vs 92.7 OCT

Sweden PPI -2.3% OCT vs -1.9% September

Sweden Household Lending 4.5% OCT Y/Y vs 4.5% SEPT

Sweden Q3 GDP 0.7% Y/Y vs 1.3% in Q2 [0.5% Q/Q vs 0.7% in Q2]

Sweden Retail Sales 1.2% OCT Y/Y vs 4.5% September

Sweden Consumer Confidence -7.4 NOV vs -2.9 OCT

Finland Business Confidence -14 NOV vs -12 OCT

Finland Consumer Confidence 1.0 NOV vs -1.6 OCT

Denmark Q3 GDP Prelim -0.5% Y/Y vs -0.6% in Q2 [0.1% Q/Q vs -0.7% in Q2]

Norway Consumer Confidence 25.4 in Q4 vs 23.4 in Q3

Netherlands Producer Confidence -7.0 NOV vs -7.7 OCT

Greece Retail Sales -10.7% SEPT Y/Y vs -7.2% AUG

Hungary Unemployment Rate 10.5% OCT vs 10.4% SEPT

Slovakia Consumer Confidence -33.1 NOV vs -38.0 OCT

Slovakia PPI 4.2% OCT Y/Y vs 4.4% SEPT

Czech Republic Business Confidence 0.3 NOV vs 2.6 OCT

Czech Republic Consumer and Business Confidence -5 NOV vs -3.3 OCT

Czech Republic Consumer Confidence -26.3 NOV vs -27 OCT

Poland Retail Sales 3.3% OCT Y/Y vs 3.1% SEPT

Poland Unemployment Rate 12.5% OCT vs 12.4% SEPT

Interest Rate Decisions:

(11/27) Hungary Base Rate Announcement CUT 25bps to 6.00%

Matthew Hedrick

Senior Analyst