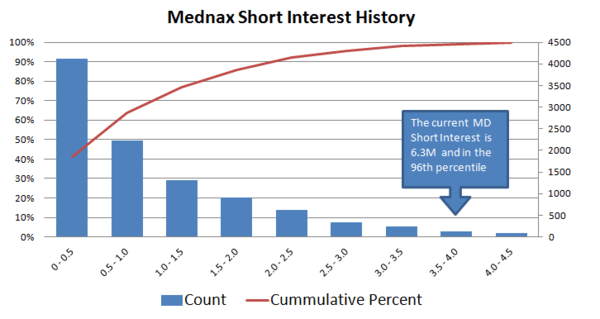

In recent weeks, we’ve noticed an increase of short interest in Mednax (MD). Short interest currently sits at 6.3 million compared to the prior two peaks of 3.5 million. Short sellers have had considerable luck with Mednax in the past and it appears they're of the belief that their winning streak will continue. Hedgeye Healthcare Sector Head Tom Tobin suggests Mednax is nearing a point where you could go long. Says Tobin:

“The best time to be long MD has been when the growth in short interest peaks and begins to decelerate and when the 3M change begins to decline. So far the first condition has been met, but on a 3M sequential basis, short interest continues to climb higher.”

Another reason to consider going long is the recent re-acceleration in births. As it relates to our positive outlook for a birth recovery, we’ve notice a few positive datapoints in recent days that coincide with the same population that drives birth trends, the 20-35 year old age group:

1. Pier 1 Imports (PIR) posted better than expected same store sales (#1 purchaser of furniture)

2. Household formation accelerated to 1.8% in October (#1 source of new households)

3. MBA Mortgage Purchase Applications Accelerating (#1 source of first time home buyers)