Yum! Brands (YUM) is selling off strong today after worse-than-expected preannounced China comps spooked analysts and investors last night. Several downgrades from the Street today have added to the fear, creating what we have seen time and again in this stock: the China scare buying opportunity.

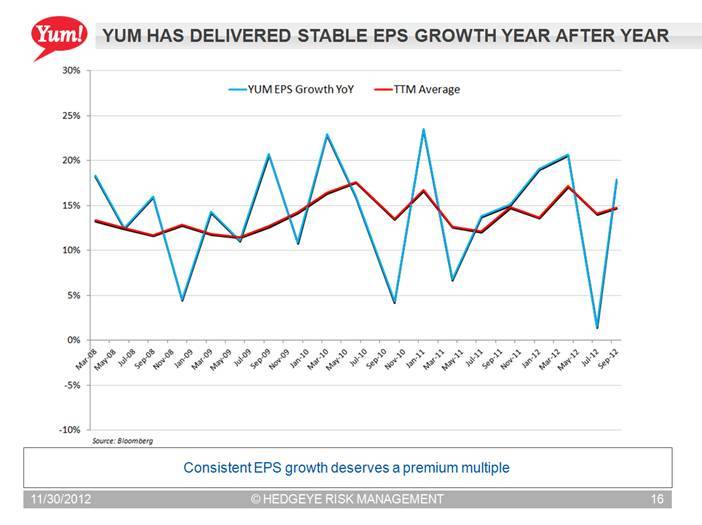

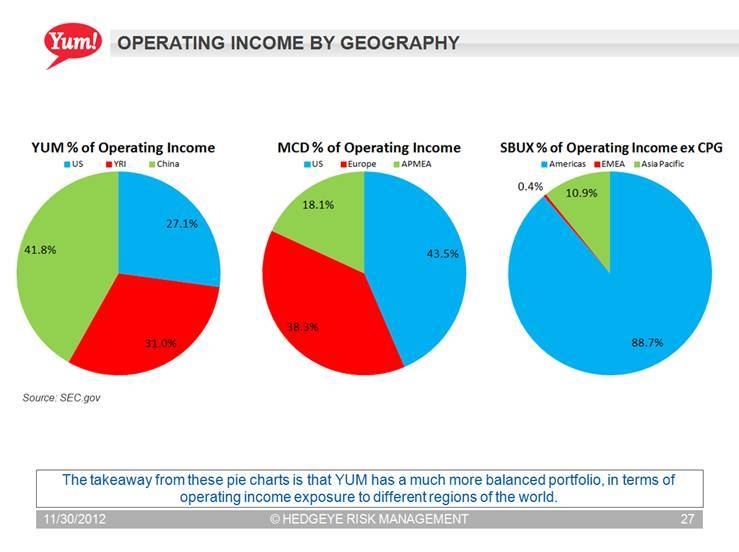

YUM is geographically diverse from an operating income perspective (first chart, below) but not so much from a sentiment perspective. The perception among many investors is that this is a “China stock”. While China is important for YUM, we would highlight that previous sequential decelerations in China’s Real GDP Growth and YUM’s China comps have not resulted in corresponding deceleration in earnings growth (second chart, below). EPS growth has been remarkably consistent over the past number of years with economic growth rates in China and other markets varying over time.

With today’s sell off, a spate of downgrades, and what seems to be a full baking in of worse China growth expectations, we believe that YUM represents a very attractive opportunity on the long side.