TODAY’S S&P 500 SET-UP – November 30, 2012

As we look at today's setup for the S&P 500, the range is 13 points or 0.70% downside to 1406 and 0.22% upside to 1419.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.36 from 1.36

- BONDS – Treasuries haven’t cared, at all, about the no volume performance chase in US Equities into another month end; #GrowthSlowing expectations continue to dominate both bond yields and fund flows; 10yr down from 1.69% at the start of the wk to 1.62%.

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Personal Income, Oct. est. 0.2% (prior 0.4%)

- 8:30am: Personal Spending, Oct. est. 0.0% (prior 0.8%)

- 8:30: PCE Deflator M/m, Oct. est. 0.1% (prior 0.4%)

- 9am: NAPM-Milwaukee, Nov. est. 47.0 (prior 43.3)

- 9:45am: Chicago Purchasing Mgr, Nov. est. 50.5 (prior 49.9)

- 11am: Fed to buy $1.75b-$2.25b notes due 2/15/36-11/15/42

- 1pm: Baker Hughes rig count

- 5pm: Fed’s Stein, Kocherlakota at panel discussion about evaluating large-scale asset purchases at Boston Fed

GOVERNMENT:

- House may vote on overhaul of U.S. work visa system, establish new kind of green card for foreign students who graduate in U.S. with advanced degrees in sci/tech

- Deadline for Barclays to respond to FERC proposal for $470m in penalties for alleged market manipulation

- American Gas Association holds a news conference to outline vision for natural gas in 2013, 9am

- CFTC Chairman Gary Gensler speaks at agency’s 2012 Research Conference on key issues in derivatives markets

- American Trucking Associations hosts final day of conference on expanding use of natural gas as a trucking fuel, with executives from UPS, Navistar, Swift

WHAT TO WATCH

- Supervalu says in active sale talks; Cerberus talks said to stall

- TNT, UPS propose steps to satisfy EU competition requirements

- Zynga loosens ties with Facebook in order to seek growth

- MSCI index changes effective as of mkt close today

- VeriSign to discuss .com registry agreement

- Health Management to hold call on allegations on “60 Minutes”

- ITC Judge Pender may release finding in HTC vs Apple case

- U.S. regulators not granted access JPMorgan emails to investigate potential energy-market manipulation, judge rules

- Steven Cohen testified to SEC on share sales, FT says

- Univerity of Michigan professor linked to SAC Capital trades resigns

- Hostess wins final bankruptcy court approval to shut down, unwind assets

- Microsoft said to plan next Xbox console for 2013 holiday season

EARNINGS:

- United Natural Foods (UNFI), 7:30am, $0.46

- Genesco (GCO) 7:31am, $1.33

- WhiteWave Foods (WWAV) Pre-Mkt, $0.17

- Exco Technologies (XTC CN) 4:30pm, C$0.14

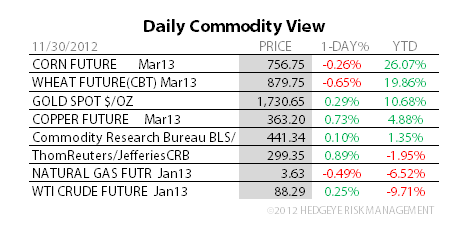

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Oil Heads for First Monthly Gain Since August on Economic Growth

- Sugar Traders Most Bearish in Two Months on Brazil: Commodities

- Gas Pricing in U.K. Is No Libor as Probe Begins: Energy Markets

- Codelco Seeing Solid Interest From China for Copper Contracts

- Copper Advances to Five-Week High on China Growth Optimism

- Shanghai Copper Stockpiles Drop to One-Month Low, Lead Increases

- Gold Extends Monthly Gain in London as Physical Demand Improves

- Felda Global Profit Slumps 40% on Lower Palm Prices, Production

- Rebar Rises First Day in Five as Discount to Spot Spurs Buying

- Aluminum Demand Growth in China Seen Least in More Than 10 Years

- Hong Kong Bourse in $1 Billion Placement for LME Purchase

- Asia to Boost West African Crude Imports to Most in Six Months

- Mistry Predicts Palm Oil Bear Market in 2013 on Supply, Reserves

- Fonterra Fund Surges Above Offer Price on Yield, Asia Links

CURRENCIES

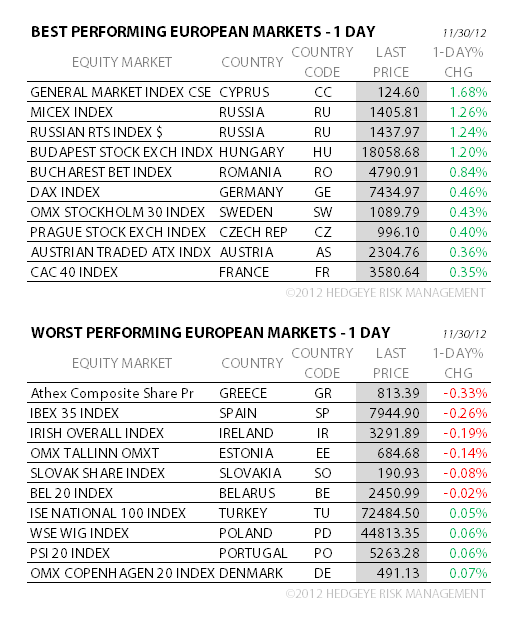

EUROPEAN MARKETS

GREEECE – remember where the bulls were at the beginning of the wk? Greece was the catalyst, then it failed – Athex going out on the lows for the wk, down -9% from the OCT lower-highs; European economic data this morning is just plain bad (Italy unemployment 11.1% = 13yr high; German and French Consumer Spending down y/y).

ASIAN MARKETS

JAPAN – one way to fool some of the people that the economy is good is to devalue your currency; Japan gets that – Yen testing 7mth lows again this morning at $82.62 vs USD and that’s good for a +10% squeeze in the Nikkei off the OCT lows – all the while, life in Japan gets worse (Exports at 3yr lows, despite the debauchery).

MIDDLE EAST

The Hedgeye Macro Team