This note was originally published November 27, 2012 at 13:42 in Retail

As a follow up to FL’s recent 3Q results, we think a reacceleration in athletic footwear industry sales after a slow start to November and a favorable near-term setup suggest a strong finish into year-end. We are also positive on FINL and NKE, which is another top long idea.

Consider the following on a TRADE basis (3-weeks or Less):

- Athletic footwear sales have come in up +5.3% over the last two weeks after coming in down -6% in the first two weeks of November accelerating sequentially each of the last 3-weeks.

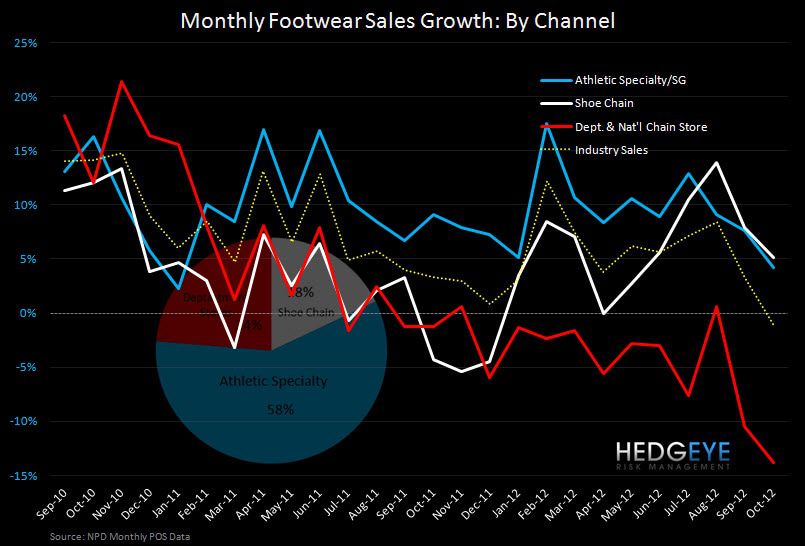

- As seen in the chart below, continued underperformance in the other channels cause weekly sales to significantly understate performance in the Athletic Specialty channel (i.e. FL, FINL, DKS, etc.).

- Basketball continues to be a significant driver with trailing 3-week domestic sales accelerating sharply higher +27% from +15% over each of the prior four weeks.

- With FL reporting comps up +MSD through the first half of November despite the industry down -6% and sales over the last two weeks running +5%, we believe FL comps are tracking well ahead of the “upper end of mid-single digit” comp plan.

- With a favorable setup through year-end and shift towards basketball in Europe, we expect more opportunity for further upside in performance.

- Retailer sales gains over the holiday weekend were heavily reliant on deep promotional activity. We think athletic footwear retailers (FL/FINL) were substantially less impacted and benefitted from more full-priced sell through with several new launches hitting over the holiday week. Moreover, while several apparel and home furnishing retailers offered free shipping on certain items for the first time, there was no incremental hit to footwear retailer margins as free shipping has become standard.

The longer-term TREND (3-Months or More) & TAIL (3-Year or Less) call:

- Still in the early stages of its turnaround, FL is not solely reliant on the ‘footwear cycle’ for growth.

- A return to new store growth for the first time in over 6-years will augment comps benefitting from higher growth and higher margin businesses (i.e. Women’s, Apparel, and Kids).

- After a decade of inventories outpacing sales growth and contracting margins under Matt Serra, FL has posted positive sales/inventory growth and margins expansion over the last three years under Ken Hicks.

- We’re see more opportunity for upside performance over the intermediate-term and are looking at $3 in earnings power next year approaching $3.50 in F14.

Source: NPD Weekly POS Data