Investors love to focus on a single catalyst and this morning's negative New Home Sales number certainly fits the bill. Negativity aside, Hedgeye Financials Sector Head Josh Steiner notes that there are two positive data points that indicate the housing market is improving.

Firstly, household formation rates continue to accelerate, having improved meaningfully since the second quarter of 2011. September and October in particular show improvements worth mentioning; from October 2011 to October 2012 there were 2.192 million new households formed. Household growth tends to be a good economic indicator and while Americans may say they're less confident, the data says otherwise.

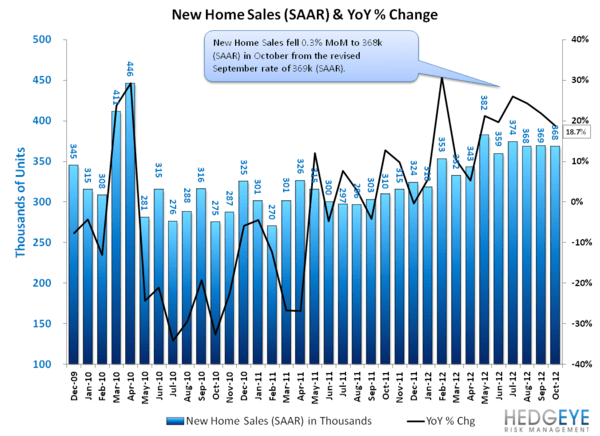

Focusing on New Home Sales, new homes sold in October were 368k (seasonally adjusted annual rate), down 0.3% month-over-month versus September's rate of 369k. On a year-over-year basis, October rose 12% versus September's change of 18.6% for the same time period. Over the long-term, new home sales are highly correlated with housing starts with the occasional mismatch. These starts are strong and show improvement in housing despite the New Home Sales number that came out this morning.