This note was originally published at 8am on November 13, 2012 for Hedgeye subscribers.

“When you get to the end of your rope, tie a knot and hang on.”

-Franklin D. Roosevelt

Much ado has been made about the Fiscal Cliff in recent weeks and rightfully so. As we outlined in the Keynesian Cliff section of our 4Q12 Macro Themes presentation, it’s only the biggest fiscal retrenchment in US history; the latest report from the CBO suggests a complete plunge over the cliff would have an estimated impact of $503 billion and $684 billion in FY13 and FY14, respectively.

Moving along, the aforementioned “plunge” comes at a time where underlying real GDP growth has crept to a near stall speed, slowing to an adjusted +0.9-1.3% QoQ SAAR rate in 3Q12, as we detailed in our 10/26 note titled: “BREAKING DOWN THE US GDP REPORT: THE ODDS OF A RECESSION JUST INCREASED”.

Needless to say, going over the cliff – proverbial or actual – could actually tilt the US economy into recession into and through the event, joining what are highly likely to be confirmed recessions in the European Union (confirmation pending the 3Q GROWTH data) and Japan (confirmation pending the 4Q GROWTH data).

While it may be trivial to suggest that having three of the world’s four largest economies mired in recession at the same time is not a bullish catalyst, we’ll gladly do so at this time. Someone has to take ownership of flagging Global Macro risks before they happen.

This we know: corporate management teams and sell-side analysts will almost-universally blame any negative guidance and/or estimate revisions on the Fiscal Cliff in the coming weeks. Even if we don’t actually traverse the cliff in the US, the sell-side will simply find some other “exogenous” catalyst for everyone to attribute further bottom-up weakness to. They’ll have to; the latest survey data suggests hedge funds are still very exposed to the long side of equities.

For now at least, few beyond the Hedgeye Macro client base will point to mean reversion within asymmetrically stretched corporate profit margins, broad-based corporate cost cutting and/or the continued popping of Bubble #3 (commodities and mining CapEx) as the likely culprits.

Keynesian Cliff Update

It’s worth stressing that the US, Japan and China are each dealing with some version of their own Keynesian Cliff, as each country’s government debt-fueled GROWTH model faces political headwinds to varying degrees.

Below, we summarize where each country is in its respective process (email us if you’d like to engage in a deeper discussion regarding anything you see below):

- US: This has morphed into nothing short of a Manic Media gong show despite the event just getting kicked off post last Tuesday’s election. The news flow in recent days has centered on the willingness to compromise on tax reform emanating from both President Obama and House Speaker John Boehner. Specifically, there seems to be a newfound willingness to extend the Bush-era tax cuts for the wealthy in exchange for “broadening the base” by tightening up loopholes and deductions. Outspoken fringe parties within both camps continue to be polarized on possible solutions, with unions largely in support of Obama playing “hardball” and not caving in to Republican demands and Senate Budget Committee chairwoman Patty Murray saying that the Democrats would agree to go over the cliff before agreeing on an unfair deal. Senate Minority Leader Mitch McConnell was recently out reaffirming the GOP mandate to “not raise taxes” and his lack of trust in the Obama administration, while some 60-80 Republican representatives have allegedly told Boehner that they would not support him on any backdoor deal struck with the White House without their consent.

- Japan: In recent weeks, Japan’s Finance Minister Koriki Jojima has repeatedly reminded investors that the Japanese sovereign will run out of money in late NOV, rendering it unable to pay its bills without the ability to issue more debt – an ability that had been previously delayed by partisan protest of the FY12 deficit financing bill. This morning, we received some directionally positive news on this front as Japan’s two main political opposition parties (the LDP and New Komeito Party) agreed to approve the deficit financing legislation in exchange for the ruling DPJ agreeing to call snap elections by late DEC or early JAN – after the previous impasse slowed public expenditures enough to begin causing increasing disruptions in funding at the regional and local levels. It’s worth noting that Japan’s Real GDP GROWTH slowed in 3Q to -3.5% QoQ SAAR from 0.3% in 2Q – without public consumption being a net drag on the economy in the quarter! Any further delays to ratifying the legislation would surely have equated to Japan reporting its second recession in the last two years when the 4Q12 GROWTH figures are published. It still might.

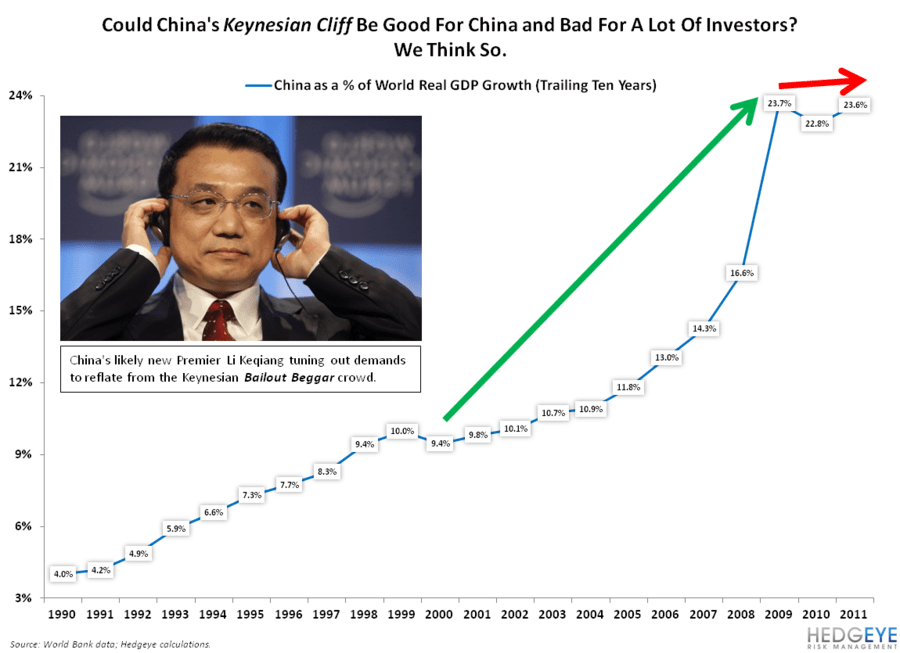

- China: We continue to think the Chinese economy is in the later stages of a bottoming process, with GROWTH slowing for the better part of the last three years to levels more consistent with the revised political objectives of those atop the Chinese Communist Party leadership. Over the past ten years, China’s investment-fueled GROWTH model – a model perpetuated by GDP targets at the State, provincial and municipal levels – has accounted for 23.6% of global real GDP growth vs. only 9.8% in the ten years preceding the Hu-Wen administration. Heightening concerns about macroeconomic sustainability and general asset quality throughout the purposefully-repressed Chinese financial system amid broad-based vertical and horizontal malinvestment have compelled Chinese officials to focus intently on heading off excesses and rebalancing their economy – gradually scaling down the Keynesian Cliff in the process. That process appears to be nearing completion from a GROWTH rate perspective, but we continue to warn that it’s too early to put capital to work largely on the premise the Chinese economy has bottomed. In fact, since a large swath of pundits and analysts decided to lock arms and agree to agree that China bottomed on OCT 18, the Shanghai Composite has fallen another -3.9% and remains in a Bearish Formation on our quantitative factoring.

All told, we will continue to let the market tell us how to risk manage the confluence of the aforementioned POLICY scenarios.

Domestically speaking, a confirmed break out above the S&P 500’s 1,419 TREND line would be a signal to us that the “can” is likely to be sufficiently kicked down the road in a way that will not upset the bond market from a sovereign credit risk perspective.

A confirmed break down below the S&P 500’s TAIL line of 1,364 suggests Obama and Boehner are likely unable to lead their respective Parties to a grand compromise and/or they were able to and the bond market does not like the solution.

It’s worth noting that a domestic sovereign credit risk scare is not at all out of the band of probable outcomes – especially given the likely JAN ‘13 timing of the debt ceiling breach. That would put a summer of 2011-type scenario in play in our opinion. Per the latest commentary from credit ratings agency Fitch:

“Washington needs to put in place a credible deficit-reduction plan to underpin the economic recovery and confidence in the full faith and credit of the US… As reflected in the Negative Outlook on the rating, failure to avoid the fiscal cliff and raise the debt ceiling in a timely manner, as well as securing agreement on credible deficit reduction, would likely result in a rating downgrade in 2013.”

Best of luck out there handicapping the world’s increasingly compromised political event risk.

Our immediate-term risk ranges for Gold, Brent (Oil), US Dollar, EUR/USD, UST 10yr Yield, Copper and the SP500 are now, 1712-1714, 105.32-109.69, 80.56-80.44, 1.26-1.28, 1.58-1.71%, 3.41-3.49 and 1364-1403, respectively.

Darius Dale

Senior Analyst