Macau average daily table revenue (ADTR) remained unchanged from last week at HK$775 million. For the full month, we are projecting YoY growth in GGR of 5-9%, above October’s 4% growth. December growth should be even better than November’s. We believe hold was normal this week and that mass traffic continues to be strong.

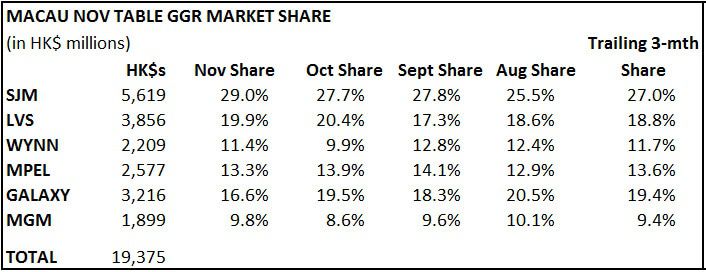

Relative to market share trend, Galaxy continues to be the laggard in November while LVS is pushing towards 20% again, above its trailing 3-month share of 18.8%.