TODAY’S S&P 500 SET-UP – November 26, 2012

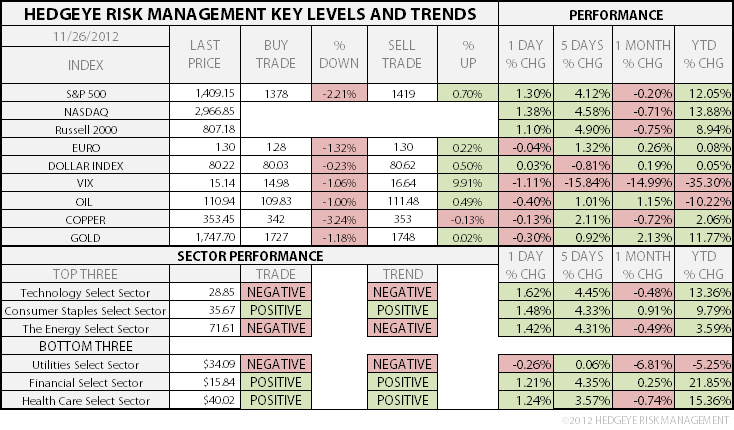

As we look at today's setup for the S&P 500, the range is 41 points or 2.21% downside to 1378 and 0.70% upside to 1419.

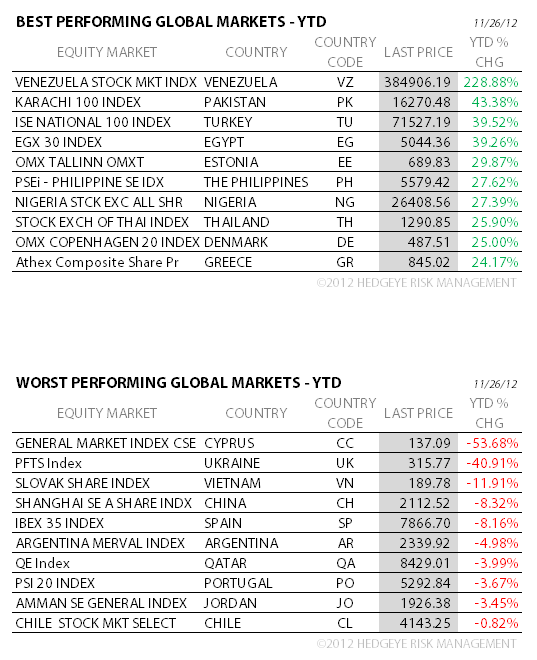

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

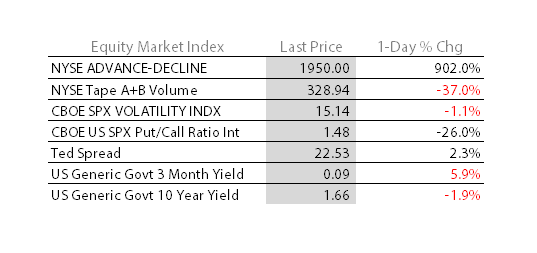

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.40 from 1.42

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Chicago Fed Nat Activity Index, Oct. (prior 0)

- 10:30am: Dallas Fed Manf. Activity, Nov. (est. 2.0, prior 1.8)

- 11am: Fed to purchase $1.75b-$2.25b notes due 2/15/36-11/15/42

- 11:30am: U.S. Treasury to sell $32b 3-mo., $28b 6-mo. bills

- 4pm: USDA crop reports

GOVERNMENT:

- Senate in session, House not in session

WHAT TO WATCH

- Shoppers lift Thanksgiving wknd spending 13% to $59.1b

- ‘Black Friday’ online retail sales rise 26% to $1b

- PNC’s Twelve Days of Christmas Price Index for 2012

- ‘Twilight,’ ‘Skyfall’ help push holiday box office to record

- Knight seen getting buyout offers this wk from Getco, Virtu

- Baxter said to near deal to buy Sweden’s Gambro for $4b

- UBS fined $47.6m, faces higher capital level over Adoboli

- UBS leads Wall Street bid to halt FHFA mortgage-bond suit

- Cohen’s SAC faces client questions as U.S. investigators circle

- Euro finance chiefs try again to approve Greek payment

- China wage gains trimmed by weaker corporate profits

EARNINGS:

- Hillenbrand (HI) 4:20pm, $0.44

- Berry Plastics (BERY), Post-Mkt, $0.28

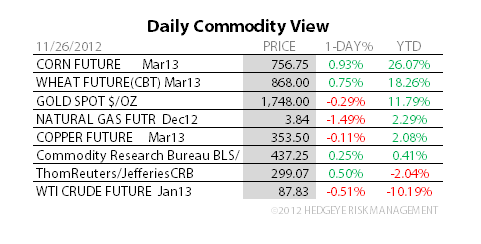

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Nickel Glut Recedes as Biggest Metals Loser Rallies: Commodities

- China Traders to Boost Rubber Imports From Thailand on Price Gap

- Crude Declines From Three-Day High as European Ministers Meet

- Copper Falls as Spain May Delay Seeking Bailout From Debt Crisis

- Gold Retreats From Six-Week High as Steady Dollar Cuts Demand

- Soybeans Extend Best Week in Three Months on South American Crop

- Coffee Falls to Nine-Month Low on Vietnam Exports; Cocoa Drops

- Palm Oil Futures Gain as Four-Day Losing Streak Attracts Buyers

- Glencore, Vedanta Face Up to 50% Pay-Raise Demand in Zambia

- Muddy Olam Call Spurred by Rule Accountants Call Ambiguous

- Pemex Discovers Oil in Region That Could Hold 1 Billion Barrels

- Japan Aluminum Buyers Said to Get Proposal for 5.5% Fee Cut

- Europe’s Shale Boom Lies in Sahara as Algeria Woos Exxon: Energy

- Brent Poised to Oust WTI as Most-Traded Oil

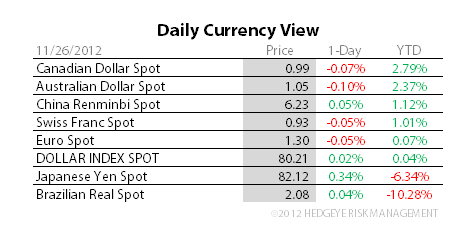

CURRENCIES

EURO – we shorted the EUR/USD on Friday as intermediate-term TREND resistance of $1.31 remains overhead; immediate-term TRADE resistance was $1.28 (now support), so now we have plenty of duration mismatch in consensus positioning to risk manage a multi-duration range around.

EUROPEAN MARKETS

ITALY – reports an all-time low in consumer confidence of 84.8 NOV (vs 86.2 in OCT) – all-time (data set only goes back to 1996) is a long-time as we head into Christmas selling season for Europe; European stocks we’re up huge (on no volume) last wk (+4.0% on the EuroStoxx600, which just made another lower-highs vs SEP).

ASIAN MARKETS

CHINA – the “China has bottomed” crowd is still looking for that bottom as the Shanghai Comp re-tested her YTD lows last night, closing -0.5% (down -18.1% since the #GrowthSlowing top in March); we need to see consumption taxes (food and energy prices) continue to deflate before we buy anything China/EastAsia.

MIDDLE EAST

The Hedgeye Macro Team