-- For specific questions on anything Europe, please contact me at to set up a call.

Positions in Europe: Short EUR/USD (FXE)

Asset Class Performance:

- Equities: The STOXX Europe 600 closed up +4.0% week-over-week vs -2.7% last week. Top performers: Cyprus +13.9%; Greece +6.9%; Finland +6.2%; France +5.4%; Italy +5.3%; Germany +5.1%; Belgium +4.6%; Sweden +4.4%; Spain +4.0%. Bottom performers: Hungary -3.0%; Slovakia -0.9%; Romania +0.4%; Czech Republic +0.7%. [Other: UK +3.8%].

- FX: The EUR/USD is up +1.84% week-over-week vs +0.17% last week. W/W Divergences: PLN/EUR +1.15%; HUF/EUR +0.89%; CZK/EUR +0.83%; SEK/EUR +0.64%; NOK/EUR +0.40%; RUB/EUR +0.33%; CHF/EUR +0.07%; DKK/EUR +0.01%; RON/EUR -0.07%; ISK/EUR -0.43%; GBP/EUR -0.84%; TRY/EUR -1.48%.

- Fixed Income: The 10YR yield for sovereigns across the periphery were down week-on-week. Greece declined the most at -94bps to 16.44%, followed by Portugal -87bps to 7.91%, Spain -21bps to 5.68%, and Italy -10bps to 4.78%. France saw the largest gain at +9bps to 2.16% and Germany gained +7bps to 1.42%.

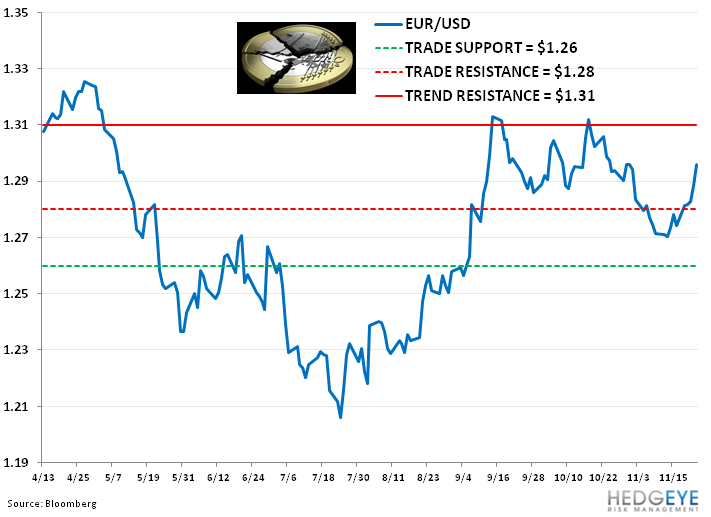

EUR/USD: Today Keith added FXE short for a second time to our Real-Time Positions at $128.97. Our EUR/USD TRADE range is $1.26 – 1.28 with a TREND resistance of $1.31.

- Our call - the EUR/USD will trade within our quantitative levels and reflect much of the daily headline risk (from Spain, Greece, and Italy in particular), however ECB President Mario Draghi’s September announcement that “the ECB is ready to do whatever it takes to preserve the euro” and the resolve of Eurocrats to maintain the Union will prevent levels falling anywhere near parity.

- We believe there is a high likelihood that no significant policy action comes in the remaining weeks of 2012, which could support the band the cross has been trading in over the last weeks.

Groundhog Day:

“You want a prediction about the weather? You’re asking the wrong Phil. I’ll give you a winter prediction: It’s gonna be cold, it’s gonna be grey, and it’s gonna last you for the rest of your life.”

-From the film Groundhog Day

No agreement was reached from Tuesday’s Eurogroup and IMF on a debt reduction package for Greece. The impasse signals to us a couple of things:

- Eurocrats will continue to react to crises by calling meetings and summits, however the “announced solutions” will continue to have little to no substance or won’t work, which will set into motion a repeat “crisis” further down the road, hence the reference to the film Groundhog Day. In particular, we think the inability of member countries to give up their fiscal sovereignty in order to create a Fiscal Union will be a significant stumbling block.

- Eurocrats are squarely on board to save in the first order their own jobs and in the second order the idea of a Union of uneven states; therefore we expect them to do all that’s necessary to keep up the Union’s status quo. In short, this means Greece will get its bills paid and you can bet that some form of restructuring of its sovereign debt is inevitable. While the market may cheer this on, suspending reality in Greece will only further divide the Union and perpetuate the uneven footing the states are bound on.

The rumor is now that a resolution on Greece’s debt, which will put the payment of its next bailout tranche ($31.5B) in motion, could come as soon as this Monday, 11/26. But don’t hold your breath! Here’s a quick update on the Greek developments:

- Sticking Points = the IMF wants Greece's debt burden to fall to 120% of GDP by 2020, while the Eurogroup believes that 2022 is a more realistic date for that debt target. The fund has also pushed for an official sector restructuring to improve Greece's debt sustainability. However, there is no consensus in the Eurogroup for a haircut, which Germany has said is illegal.

- Remedy Options Under Consideration = one measure revolved around a 10-year suspension of interest payments on loans to Greece from the EFSF. It said that this would result in €44B of savings. It added that there is also a possibility that the interest rate on loans to Greece from Eurozone countries could be reduced to 0.25% from 1.5%, though it added that Germany was opposed to such a step.

Another signal this week that it’s Groundhog Day, Moody’s downgraded France's government bond rating by one notch to Aa1 from Aaa citing an uncertain fiscal outlook, deteriorating economy in the short-term, and longer-term structural rigidities. This came as no great surprise and was a repeat of S&P’s decision to downgraded France back in January.

The move by two leading credit ratings agencies however begs the questions, should the ESM and EFSF facilities also be downgraded, with the second largest backer to Germany losing its AAA status. We think the answer is yes but would further suggest that given the level of central bank intervention in markets, AA is new AAA.

Finally, gear up for a Spanish regional election in Catalonia on Sunday, a region with a long history of succession desires given its bend towards cultural and economic independence (more below under “Call Outs”).

The European Week Ahead:

Sunday: Regional Election in Spain’s Catalonia

Monday: Eurozone Finance Ministers may sign off on Greece’s next bailout tranche (31.5B EU); ECB's Constancio Speaks in Berlin; Dec. Germany GfK Consumer Confidence Survey; Oct. Germany Import Price Index; Nov. UK Nationwide House Prices (Nov. 26-29); Sep. Spain Mortgages-capital loaned, Mortgages on Houses; Nov. Italy Consumer Confidence

Tuesday: Nov. Eurozone OECD Economic Outlook; Sep. UK Index of Services; 3Q UK GDP, Private Consumption, Government Spending, Gross Fixed Capital Formation, Exports, Imports and Total Business Investment – Preliminary; Oct. France Jobseekers; Oct. Italy Hourly Wages; Spain AFME 4th Annual Spanish Funding Conference in Madrid; Oct. Spain Budget Balance

Wednesday: Oct. Eurozone M3; Nov. Germany CPI – Preliminary; Oct. Spain Retail Sales

Thursday: Nov. Eurozone Consumer Confidence – Final, Services Confidence, Business Climate Indicator, Industrial Confidence; Nov. Germany Unemployment Change, Unemployment Rate; Nov. UK CBI Reported Sales, GfK Consumer Confidence Survey, Oct. UK Net Consumer Credit, Net Lending Sec. on Dwellings, Mortgage Approvals, M4 Money Supply; Sep. Spain Total Housing Permits; Nov. Italy Business Confidence; Economic Sentiment

Friday: Nov. Eurozone CPI Estimate; Oct. Eurozone Unemployment Rate; Oct. Germany Retail Sales; Oct. France Producer Prices, Consumer Spending; Nov. Spain CPI - Preliminary; Sep. Spain Current Account; Nov. Italy CPI - Preliminary; Oct. Italy Unemployment Rate – Preliminary, PPI, 3Q Italy Unemployment Rate; Sep. Greece Retail Sales

Extended Calendar:

DEC 1 – Beginning of the Russian Presidency of G20

DEC 3 – Eurogroup Meeting in Brussels

DEC 6 – ECB Governing Council Meeting

DEC 12-13 – First public consultation between the Russian government, B20 Coalition and international civil society representatives on G20 agenda for 2013 (in Moscow)

DEC 20 – ECB Governing and General Council Meeting

APR 2013 – Parliamentary elections in Italy

MAY 2013 – Presidential elections in Italy

Call Outs:

UK - BOE Minutes: voted 9-0 to keep interest rates on hold, 8-1 to maintain current asset purchases target.

Spain - Newspaper polls last Sunday showed that CiU, the Catalan nationalist party, will win the closely watched regional parliamentary elections this Sunday (25-Nov), but will not gain an absolute majority. It added that the pro-independence party of President Artur Mas is expected to win 60-64 seats in the Catalan parliament, little changed from the 62 seats it currently holds, but short of the 68 seats needed for an absolute majority. According to the article, an absolute majority would give the government more legitimacy in its ongoing battle with Madrid for independence.

Spain - Spanish Prime Minister Rajoy warned that a vote for Catalan independence risked excluding the region from the EU (recall that the Rajoy administration has repeatedly argued that a Catalan referendum on independence is illegal). However, the article noted that Catalan President Artur Mas would consider pursuing a separation from Spain even if an independent Catalan state were denied EU membership. His chief of staff, Joan Vidal de Ciurana, told Bloomberg that Catalonia would not need Spain's Treasury for funding if it had the possibility to become a state and negotiate directly with the markets.

Germany - Bloomberg noted that Europolis, a German citizen group, filed a lawsuit over the ECB's new intervention program at the EU General Court. The article said that the plaintiffs have asked the court to declare the OMT to be incompatible with EU law. It added the case is the sixth challenging the ECB to reach the EU's two top courts.

Data Dump:

Eurozone PMI Manufacturing 46.2 NOV Prelim (exp. 45.6) vs 45.4 OCT

Eurozone PMI Services 45.7 NOV Prelim (exp. 46) vs 46 OCT

Eurozone PMI Composite 45.8 NOV Prelim (exp. 45.7) vs 45.7 OCT

Eurozone Construction Output -2.6% SEPT Y/Y vs -1.4% AUG

Eurozone Consumer Confidence -26.9 NOV (exp. -25.9) vs -25.7 OCT

Germany Q3 GDP Final UNCH vs Previous 0.2% Q/Q and 0.9% Y/Y

Germany Domestic Demand 0.0% in Q3 (inline) vs -0.4% in Q2

Germany Exports 1.4% in Q3 (exp. 1.0%) vs 3.3% in Q2

Germany Imports 1.0% in Q3 (exp. 0.5%) vs 2.2% in Q2

Germany Capital Investment 0.2% in Q3 (exp. -0.1%) vs -2.1% in Q2

Germany Govt Spending 0.4% in Q3 (exp. 0.2%) vs -0.2% in Q2

Germany Construction Investment 1.5% in Q3 (exp. 0.8%) vs -1.1% in Q2

Germany Private Consumption 0.3% in Q3 (vs 0.2%) vs 0.1% in Q2

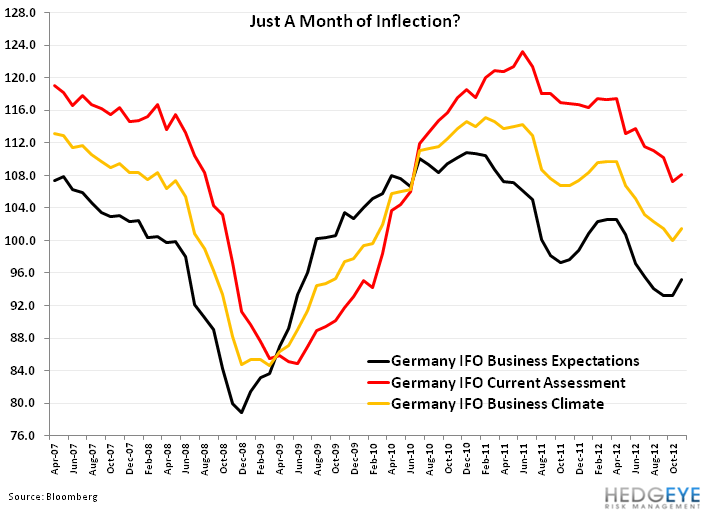

Germany IFO Business Climate 101.4 NOV (exp. 99.5) vs 100 OCT

Germany IFO Current Assessment 108.1 NOV (exp. 106.3) vs 107.2 OCT

Germany IFO Expectations 95.2 NOV (exp. 93) vs 93.2 OCT

Germany PMI Manufacturing 46.8 NOV Prelim (exp. 46) vs 46 OCT

Germany PMI Services 48 NOV Prelim (exp. 48.3) vs 48.4 OCT

Germany Producer Prices 1.5% OCT Y/Y vs 1.7% SEPT

France PMI Manufacturing 44.7 NOV Prelim (exp. 44) vs 43.7 OCT

France PMI Services 46.1 NOV Prelim (exp. 45) vs 44.6 OCT

France Own-Company Production Outlook -7 NOV vs -9 SEPT

France Production Outlook -40 NOV vs -55 SEPT

France Business Confidence 88 NOV vs 85 September

UK BBA Loans for House Purchase 33,039 OCT vs 31,544 September

Italy Retail Sales -1.7% SEPT Y/Y (exp. -1.1%) vs -1.1% AUG

Italy Industrial Orders NSA -12.8% SEPT Y/Y vs -9.0% AUG

Spain Producer Prices 3.5% OCT Y/Y vs 3.8% SEPT

Portugal Producer Prices 4.6% OCT Y/Y vs 4.5% SEPT

Austria Industrial Production 2.3% SEPT Y/Y vs 3.8% AUG

Switzerland Exports -16.5% OCT M/M vs 2.9% SEPT [Watch exports +9.3% Y/Y in real terms; +13.2% Y/Y in nominal terms]

Switzerland Imports -8.2% OCT M/M vs 4.6% September

Switzerland M3 Money Supply 8.6% OCT Y/Y vs 8.8% SEPT

Denmark Retail Sales -1.4% OCT Y/Y vs -2.8% SEPT

Denmark Consumer Confidence Indicator -1.3% NOV vs -5.5% OCT

Netherlands Consumer Spending 0.0% SEPT vs -1.8% AUG

Netherlands House Price Index -7.8% OCT Y/Y vs -7.9% SEPT

Norway Q3 GDP 0.7% Q/Q vs 0.8% in Q2

Finland Unemployment Rate 6.9% OCT vs 7.1% September

Poland Core CPI 1.9% OCT Y/Y vs 1.9% SEPT

Slovenia PPI 0.8% OCT Y/Y vs 0.7% September

Hungary Avg Gross Wages 3.7% SEPT Y/Y vs 3.8% AUG

Bulgaria Unemployment Rate 11% OCT vs 10.6% SEPT

Russia Foreign Direct Investment 4.6% in Q3 vs 8.0% in Q2

Russia Unemployment Rate 5.3% OCT vs 5.2% September

Russia Disposable Income 2.4% OCT Y/Y vs 3.8% September

Russia Real Wages 5.2% OCT Y/Y vs 4.7% September

Russia Retail Sales 3.8% OCT Y/Y vs 4.4% SEPT

Russia Investment in Production Capacity 4.9% OCT Y/Y vs -1.3% September

Turkey Foreign Tourist Arrivals 0.4% OCT Y/Y vs 1.7% SEPT

Interest Rate Decisions:

(11/20) Turkey Benchmark Rep Rate UNCH at 5.75%

(11/20) Turkey Overnight Lending Rate CUT 50bps to 9.00%

Matthew Hedrick

Senior Analyst