This note was originally published November 23, 2012 at 08:29 in Early Look

“The last of human freedoms - the ability to chose one's attitude in a given set of circumstances."

-Viktor Frankl

Typically over Thanksgiving, I head over to Keith’s house and join his family for a masterfully prepared feast by his wife. This year they’ve headed out of town, so I joined some friends on an impromptu basis in Williamsburg, Brooklyn. No, I didn’t don skinny jeans for the adventure, but I did experience a gluten-free Thanksgiving for the first time.

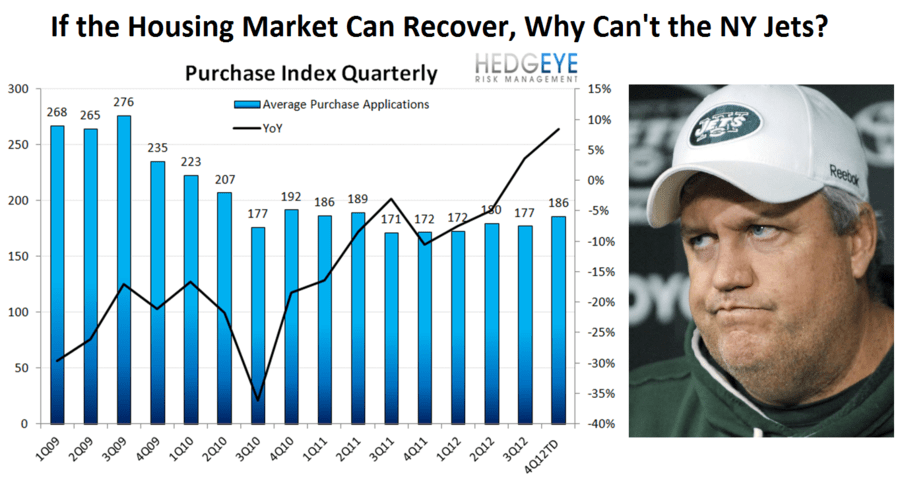

As a Canadian in the United States, I have always been thankful for the great American holiday of Thanksgiving. It is the ideal opportunity to reconnect with old friends and establish new friendships. And if you are a fan of the correct NFL team, it is also a chance to cheer your team to victory. Unfortunately, for those fans of the New York Jets, the last point doesn’t exactly hold.

Given the elongated nature of the holiday this year, I’ve also been doing some reading for pleasure and have picked up Viktor Frankl’s best-selling book, “Man’s Search for Meaning.” For those that haven’t read this great book, it is basically the story of Frankl’s time in the Nazi German concentration camps. The gist of the book is that humans can, and should, find meaning in even the most sordid of situations.

It goes without saying that we have had a relatively negative outlook on global growth this year. Even as a resolution of the Fiscal Cliff becomes possible, we aren’t likely to be persuaded that global growth is set to accelerate. As it relates to equities, the key issue of tepid economic growth is that the pace of earnings growth will ultimately slow, as it has and is in the United States (one of our key Q3 themes).

Even as bearish as we are and have been on economic activity, we are certainly not as pessimistic as Jeremy Grantham, who wrote the following in his most recent quarterly letter:

“The U.S. GDP growth rate that we have become accustomed to for over a hundred years – in excess of 3% a year – is not just hiding behind temporary setbacks. It is gone forever. Yet most business people (and the Fed) assume that economic growth will recover to its old rates.

Going forward, GDP growth (conventionally measured) for the U.S. is likely to be about only 1.4% a year, and adjusted growth about 0.9%.”

Certainly, Grantham has an impressive long run track record, but there is always danger in predicting out for long time frames. In this case, Grantham is actually saying that the United State’s historic growth rate of 3% is gone forever. As much respect as we have for Grantham, we wouldn’t bet against the American people and their ability to innovate and create economic growth in the long run.

In the short term, akin to Frankl’s ideas of finding a positive in the most sordid of situations, housing is starting to become a real positive factor in the U.S. economy. Our Financials Team led by Josh Steiner has done much of our housing work and on the way down was correct in his analysis that housing would take longer to bottom than consensus expected. Conversely, on the way up, Steiner is starting to develop the thesis that housing may recover quicker than expected.

The most recent data point on housing was mortgage applications from last week that rose 3.0% week-over-week, which is on the back of a 11.0% increase in the prior week. In the Chart of the Day, we show mortgage application data going back to 2009. The key takeaway is that mortgage applications are starting to accelerate on a year-over-year basis.

The conundrum of the housing market for many has been the fact that mortgage applications, and thus purchases, have remained at anemic levels despite all-time lows in interest rates. In part, of course, this is due to tighter lending standards from banks, but the other key component is psychological. In effect, housing is a virtuous cycle in which rising prices and falling inventory actually stoke demand. So when potential home buyers see that prices are starting to accelerate, or there is less inventory, they get more excited to buy. A shocking concept we know – people chase price!

To be clear, a stabilization in the housing market is basically a consensus call at this point. There is an alternative scenario from the simple linear recovery though, which is that the housing recovery could become parabolic. As my colleague Josh Steiner wrote last week:

“Fundamentally, the data suggests that over the long run total housing starts have grown at a rate slightly above the growth rate in household formation. From 1959-2012 housing starts have averaged 1.468 million per year while over that same time period new household formation has averaged 1.287 million per year. Recently, household formation rates have picked up sharply.

From 3Q11 through 2Q12, household formation growth has risen at an annualized rate of 1.739 million, yet housing starts have been running at an annualized rate of 0.673 million during that same time period. Our parabolic extrapolation from above projects that housing starts would rise to an annualized level of 1.318 million and 1.886 million by year-end 2013 and 2014, respectively, whereas a linear extrapolation gets to 1.012 million and 1.180 million by year-end 2013 and 2014.

While the parabolic extrapolation may seem high, it exceeds recent household formation rates by just 147k units. This compares with the 53 year trend (1959-2012) of starts exceeding HH formation by an average of 181k.”

Simply put, the combination of rising prices, tight inventories, and increasing household formation may lead to an accelerating recovering in housing. This would certainly be beacon of positivity in sordid economic recovery.

Our immediate-term Risk Ranges (support and resistance) for Gold, Oil (Brent), Natural Gas, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1714-1738, $109.21-111.48, $3.73-3.94, $80.53-81.36, $1.26-1.28, 1.54-1.68%, and 1364-1399, respectively.

Happy Thanksgiving to you and your families.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research