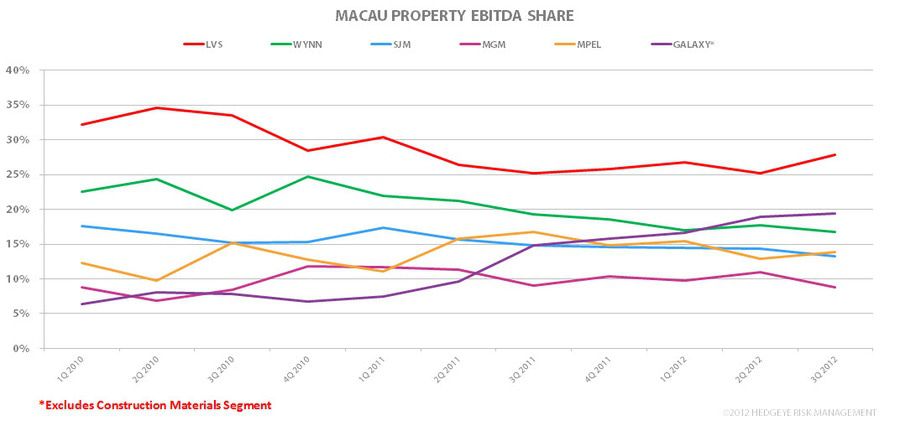

While much of the EBITDA share movements is due to hold fluctuation, we believe LVS will continue to gain revenue and EBITDA share

- LVS maintained its industry leading position thanks to a strong performance from the Venetian. 3Q EBITDA share improved 2.8% QoQ to 27.9%.

- Due to stellar results at Galaxy Macau, Galaxy has surged into 2nd place, a significant rise over the last year. Galaxy Macau’s EBITDA rose 12% QoQ.

- MGM continues to hold the rear. 3Q EBITDA was negatively impact by low hold on direct play and rolling chip play.