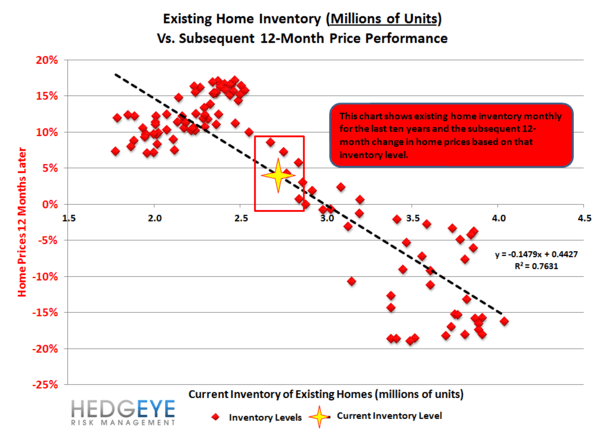

One of the most important metrics for the housing market is existing inventory of homes for sale. Existing inventory recently moved lower (a positive for the market) by 7.8% on a month-over-month basis for October and 21.9% on a year-over-year basis. Levels continue to tighten which helps improve price and rid the market of excess housing. The charts below showcase the current state of the housing market over various metrics.