Macau average daily table revenue (ADTR) grew 17% YoY last week, in-line with our expectations. For the full month, we are projecting YoY growth in GGR of 5-10%, above October’s 4% growth. We continue to believe that December growth will be even better than November’s. However, we would caution that there is likely to be some investor consternation surrounding the smoking restrictions which may go into effect either January 1 or 14.

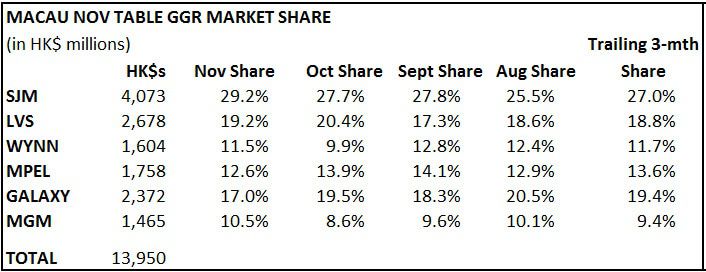

Relative to trend, SJM and MGM seem to be outperforming in terms of market share while Galaxy and MPEL lag behind.