TODAY’S S&P 500 SET-UP – November 19, 2012

As we look at today's setup for the S&P 500, the range is 29 points or 1.83% downside to 1335 and 0.30% upside to 1364

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.37 from 1.34

- BONDS – the US Treasury market has not and could not care less about Equity emotions flickering on the futures tick; 10yr at 1.60% this morning remains in a Bearish Formation; Bonds remain in a Bullish Formation, despite High Yield and IG debt underperforming last wk (HYG looking interesting short side for the 1st time in a long time).

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: NAHB Housing Market Index, Nov., est. 41 (prior 41)

- 10am: Existing Home Sales, Oct., est. 4.75m (prior 4.75m)

- 11am: Fed to sell $7b-$8b notes due 7/31/15-11/15/15

- 11:30am: U.S. Treasury to sell $32b 3 mo. bills, $28b 6 mo. bills

- 4pm: Crop conditions: winter wheat

GOVERNMENT:

- President Obama continues trip to Southeast Asia, visits Myanmar

- Brookings Institution holds discussion on capital markets, fiscal cliff with Robert Greifeld, CEO of Nasdaq. 1pm

- House, Senate not in session

WHAT TO WATCH

- Cisco buys Meraki for $1.2b to add technology that elps businesses manage Wi-Fi networks remotely

- Obama says he’s confident about deal to avoid fiscal cliff

- Oct. sales of previously owned homes probably stayed at 2-yr high of 4.75m annual rate

- Jana proposes 5 new directors for Canada’s Agrium: G&M

- European finance chiefs seek to settle Greek aid this wk amid IMF spat

- Nintendo Wii U goes on sale in U.S. with apps, no TVii

- News Corp. expected 49% bid to value YES channel at $3b: NYT

- Wal-Mart workers vow to mount 1k protests online and outside stores up to and including Black Friday

- Hostess to seek approval to liquidate as Metropoulos weighs bid

- ITC decision on whether to review Apple vs Samsung findings

- EMI goes on auction block again this wk as Universal Music divests some assets to meet antitrust requirements

- Israel ready to invade Gaza Strip if cease-fire efforts fail

- HSBC is in talks to sell its $9b stake in Ping An Insurance

- Shadow banking grows to $67t industry, Financial Stability Board said in a report

- Weekly agendas: IPO, Media/Entertainment, Real Estate, Health, Consumer, Tech, Transport, Industrial, Energy, Canada Energy, Canada Mining

EARNINGS:

- Lowe’s (LOW) 6am, $0.35 Preview

- New Jersey Resources (NJR) 6:59am, $(0.26)

- Tyson Foods (TSN) 7:30am, $0.44

- Laclede (LG) 8:30am, $(0.17)

- Urban Outfitters (URBN) 4pm, $0.41

- Nuance Communications (NUAN) 4:01pm, $0.48

- Bob Evans (BOBE) 4:01pm, $0.61

- Krispy Kreme (KKD) 4:01pm, $0.08

- Brocade Communications (BRCD) 4:04pm, $0.14

- Agilent Technologies (A) 4:05pm, $0.80

- Perfect World (PWRD) 5pm, $0.48

- Qihoo 360 (QIHU) 5pm, $0.14

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Gains in London on Weaker Dollar, Israel Conflict Concern

- Hedge Funds Cut Bets in Longest Retreat Since 2008: Commodities

- Oil Rises a Second Day Amid Israel Conflict, U.S. Budget Talks

- Soybeans Gain From Lowest Price Since June as U.S. Exports Jump

- Copper Rises in London on Speculation U.S. to Avoid Fiscal Cliff

- Sugar Gains Amid Speculation Recent Price Drop Attracting Buyers

- Iron-Ore Swaps Fall Most in a Month on China Real-Estate Prices

- Gold Set for Record in Euros by End of Year: Technical Analysis

- Speculators Sell Gas at 1-Year High to Utilities: Energy Markets

- Condoms Provide Lifeline for Malaysian Rubber: Southeast Asia

- Glasenberg Breaks Word on Equal With Glencore-Xstrata Deal Near

- BP Seen Takeover Target as Valuation Sinks on Settlement: Energy

- IEA Says Energy Demand to Rise By More Than a Third to 2035

- Cocoa-Growing Nations Seen Grinding 50% of Beans in Three Years

- Rebar Declines on Speculation China Won’t Relax Property Curbs

CURRENCIES

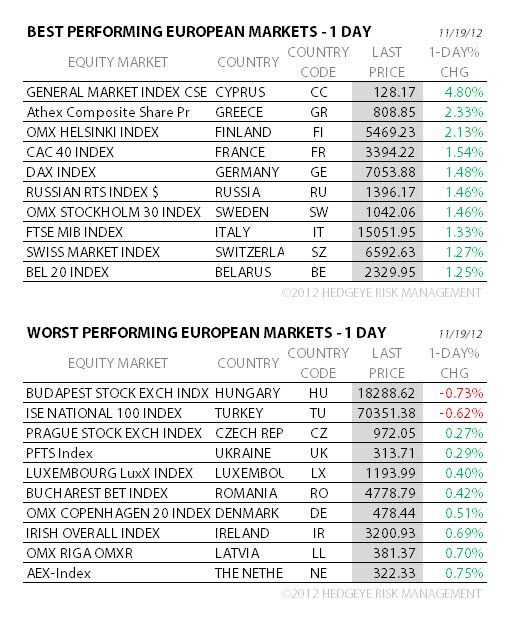

EUROPEAN MARKETS

EUROPE – Europe is picking up +1.1% of last week’s -2.7% decline in the EuroStoxx600; big damage done on that move as TREND lines snapped across the board; so watch the DAX from here as its TREND line of 7116 is one of the most important on my screens for Equity risk, globally; covered our Spain short on Friday, making us 16 for 17 (all-time) on the short side.

ASIAN MARKETS

ASIA – very mixed message coming out of Asian Equities this morn – Japan is channeling its inner-Krugman w/ money printing rhetoric = Yen down, Stocks straight up (+1.4% overnight post Nikkei +3% last wk), but Chinese stocks closed 11bps above their YTD lows after the new leadership didn’t deliver a Western style bailout; Indonesia -0.87% led decliners.

MIDDLE EAST

The Hedgeye Macro Team