-- For specific questions on anything Europe, please contact me at to set up a call.

Positions in Europe: Short EUR/USD (FXE)

Asset Class Performance:

- Equities: The STOXX Europe 600 closed down -2.7% week-over-week vs -1.7% last week. Bottom performers: Cyprus -9.2%; Netherlands -3.6%; Ireland -3.5%; Hungary -3.3%; Portugal -3.2%; Switzerland -3.1%; Germany -3.0%; Denmark -2.9%; UK -2.8%. Top performers: Latvia +1.4%; Poland +1.3%; Estonia +0.2%. [Other: France -2.4%; Greece -1.4%].

- FX: The EUR/USD is up +0.17% week-over-week. W/W Divergences: CHF/EUR +0.15%; PLN/EUR +0.05%; DKK/EUR 0.00%; GBP/EUR -0.19%; RUB/EUR -0.69%; SEK/EUR -0.88%; NOK/EUR -0.91%.

- Fixed Income: The 10YR yield for sovereigns were mostly down week-on-week. Greece declined the most at -49bps to 17.38%, followed by Italy -12bps to 4.88%, Portugal -8bps to 8.78%, and France -6bps to 2.07%. Spain saw the largest gain at +6bps to 5.89% and Germany gained +2bps to 1.35%.

EUR/USD: Keith added FXE to our Real-Time Positions at $127.06. Our EUR/USD TRADE range is $1.26 – 1.28 with a TREND resistance of $1.31.

- Our call - the EUR/USD will trade within our quantitative levels and reflect much of the daily headline risk (from Spain, Greece, and Italy in particular), however ECB President Mario Draghi’s September announcement that “the ECB is ready to do whatever it takes to preserve the euro” and the resolve of Eurocrats to maintain the Union will prevent levels falling anywhere near parity.

- We believe there is a high likelihood that no significant policy action comes in the remaining weeks of 2012, which could support the band the cross has been trading in over the last weeks.

R is for Recession:

It came as little surprise this week but the Eurozone officially moved into recession with preliminary Q3 GDP showing a -0.1% contraction quarter-over-quarter following a -0.2% contraction in Q2.

Now the task is sorting through the timing of an eventual recovery, which we think could have a long runway.

Where We Are At?

Eurozone Finance Ministers agreed to allow Greece to implement its austerity program over 4 years instead of 2 years this week but postponed a decision on the next tranche of Greek aid (€31.5B) until either next Monday’s Eurozone Finance Ministers Meeting or Thursday’s EU Summit. A big point of contention is the rift between the IMF and Eurogroup over Greece’s debt reduction schedule. The IMF wants Greece’s debt to fall to 120% of GDP by 2020 while the Eurogroup says by 2022. While cohesion is needed, what’s more disturbing is both parties will set a target that they both know Greece has no chance of attaining.

Further, the IMF continues to push for an official debt restructuring, while the Eurogroup has rejected the haircut option. It appears the path of least resistance might be improving financing rates and lengthening the maturity of the loans.

Longer-term we believe there is a high likelihood that no significant policy action comes in the remaining weeks of 2012. As a reminder, some of the main topics that Eurocrats are wrestling with are:

- Setting up a Banking Union (with Pan-European Deposit Insurance)

- Setting up a Fiscal Union

- If and when Spain will request another bailout (and will it come from the IMF or ESM, or both?)

In terms of setting up a Banking Union and Fiscal Union, we believe the two are dependent on each other. While more attention has been given to a Banking Union recently, we believe Eurocrats reaching an agreement on a Fiscal Union over the near term is incredibly unlikely as countries are unwilling to part with their fiscal sovereignty. This could be one factor to put downside pressure in the cross.

On Spain, we think the sovereign asking for a bailout is a question of when and not if. The recent rumor that Spain may look to the IMF for a loan would reflect the likelihood of more favorable terms versus the European Commission and ECB’s ‘conditionality’ for aid via the ESM or OMT.

Beyond the headline news, and broader negative data out this week (see below in the section “Data Dump”), there were a couple of charts that caught our attention this week:

- Europe27 New Car Registration -4.8% OCT Y/Y vs -10.8% – down meaningfully but showing slight improvement?

- EU External Trade Balances – only part of the story, but a positive trend move.

The European Week Ahead:

Sunday: Nov. UK releases Rightmove House Prices

Monday: Eurozone Finance Ministers Meeting; Sep. Eurozone Construction Output; Sep. Italy Industrial Orders and Sales; Sep. Greece Current Account

Tuesday: Oct. Germany Producer Prices

Wednesday: BoE Minutes; Oct. UK Public Finances, Public Sector Net Borrowing; Sep. Spain Trade Balance

Thursday: EU Summit and ECB Governing Council Meeting; Nov. Eurozone PMI Composite, Manufacturing and Services – Advance, Consumer Confidence – Advance; Nov. Germany PMI Manufacturing and Services – Advance; Nov. UK CBI Trends Total Orders and Selling Prices; Nov. France PMI Manufacturing and Services - Preliminary

Friday: Nov. Germany IFO Business Climate, Current Assessment and Expectations; 3Q Germany GDP – Final, Domestic Demand, Exports, Capital Investment, Government Spending, Construction Investment, Imports, Private Consumption; Oct. UK BBA Loans for House Purchase; Nov. France Production Outlook Indicator, Business Confidence Indicator; Oct. Spain Producer Prices; Sep. Italy Retail Sales

Extended Calendar:

NOV 26 – Finance Ministers may sign off on Greece’s next bailout tranche, 31.5B EUR

NOV 27 – AFME 4th Annual Spanish Funding Conference in Madrid

DEC 1 – Beginning of the Russian Presidency of G20

DEC 3 – Eurogroup Meeting in Brussels

DEC 6 – ECB Governing Council Meeting

DEC 12-13 – First public consultation between the Russian government, B20 Coalition and international civil society representatives on G20 agenda for 2013 (in Moscow)

DEC 20 – ECB Governing and General Council Meeting

APR 2013 – Parliamentary elections in Italy

MAY 2013 – Presidential elections in Italy

Call Outs:

European Day of Action and Solidarity – unprecedented and coordinated cross-border protests against austerity measures on Wednesday with 40 unions participating across 23 countries (strikes mainly in Italy, Spain, Greece, and Portugal).

Spain - El Confidencial, without citing sources, reported that Spain is considering requesting a credit line from the IMF as an alternative to a European bailout. The paper highlighted the support for Spain recently expressed by both President Obama and IMF leaders, along with concerns about Germany's resistance to additional funding for Spain and its continued insistence on austerity prescriptions.

Spain - the government passed a decree to prevent low-income families being evicted for defaulting on their mortgages, and plans to create a stock of homes that can be rented out cheaply.

Banking Union - some hawkish comments on the proposed banking union from ECB governing council member (and Bundesbank President) Jens Weidmann in a guest column in the German financial daily Handelsblatt. He said that establishing the ECB as the single supervisory mechanism risks compromising the central bank's primary goal of price stability. He also noted that a banking union should not be rushed, while adding that it would need a resolution mechanism that should be funded by the banks themselves, and not by European taxpayers. In addition, he argued that legacy risks should be the responsibility of respective member states.

Data Dump:

Preliminary Q3 GDP:

Eurozone -0.6% Y/Y (inline) vs -0.4% in Q2 [-0.1% Q/Q (inline) vs -0.2% in Q2]

Germany 0.9% Y/Y (exp. 0.8%) vs 1.0% in Q2 [0.2% Q/Q (exp. 0.1%) vs 0.3% in Q2]

France 0.2% Y/Y (exp. 0.0%) vs 0.1% in Q2 [0.2% Q/Q (exp. 0.0%) vs -0.1% in Q2]

Italy -2.4% Y/Y (exp. -2.9%) vs -2.4% in Q2 [-0.2% Q/Q (exp. -0.5%) vs -0.7% in Q2]

Netherlands -1.6% Y/Y (exp. -0.5%) vs -0.4% in Q2 [-1.1% Q/Q (exp. -0.2%) vs 0.1% in Q2]

Czech Republic -1.5% Y/Y (exp. -1.2%) vs -1.0% in Q2 [-0.3% Q/Q (exp. -0.2%) vs -0.2% in Q2]

Hungary -1.5% Y/Y (exp. -1.3%) vs -1.5% in Q2 [-0.2% Q/Q (exp. -0.1%) vs -0.4% in Q2]

Romania -0.6% Y/Y (exp. 0.0%) vs 1.1% in Q2 [-0.5% Q/Q (exp. -0.4%) vs 0.5% in Q2]

Eurozone ZEW Economic Sentiment -2.6 NOV vs -1.4 OCT

Europe27 New Car Registration -4.8% OCT Y/Y vs -10.8%

Eurozone Industrial Production -2.3% SEPT Y/Y (exp. -2.2%) vs -1.3% AUG [-2.5% M/M vs 0.9% AUG]

Germany Wholesale Price Index 4.6% OCT Y/Y vs 4.2% SEPT

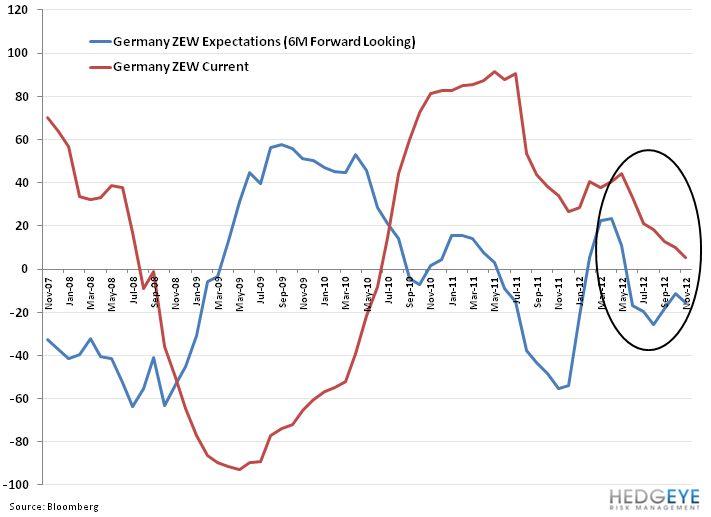

Germany ZEW Current Situation 5.4 NOV (exp. 8) vs 10 OCT

Germany ZEW Economic Sentiment -15.7 NOV (exp. -10) vs -11.5 OCT

UK PPI Input 0.1% OCT Y/Y (exp. -0.5%) vs -1% SEPT

UK PPI Output 2.5% OCT Y/Y (exp. 2.5%) vs 2.5% September

UK Retail Price Index 3.2% OCT Y/Y vs 2.6% September

UK ILO Unemployment Rate 7.8% SEPT vs 7.9% AUG

UK Jobless Claims Change 10.1K OCT vs 0.8K September

UK Retail Sales w/ Auto Fuel 0.6% OCT Y/Y (exp. 1.6%) vs 2.4% SEPT

France Prelim. Q3 Wages 0.4% Q/Q vs 0.5% in Q2

Spain Q3 GDP Final -1.6% Y/Y (inline)

Spain House Transactions 0.9% SEPT Y/Y vs 3.0% AUG

Portugal Prelim Q3 GDP -0.8% Q/Q (exp. -0.6%) vs -1.1% in Q2 [-3.4% Y/Y (exp. -3.2) vs -3.2% in Q2]

Portugal Unemployment Rate 15.8% in Q3 vs 15.0% in Q2

Switzerland Producer and Import Prices 0.4% OCT Y/Y vs 0.3% September

Switzerland Credit Suisse ZEW Survey Expectations -27.9 NOV vs -28.9 OCT

Ireland PPI 2.9% OCT Y/Y vs 2.2% SEPT

Greece Prelim Q3 GDP -7.2% Y/Y vs -6.3% in Q2

Sweden Unemployment Rate 7.1% OCT vs 7.4% SEPT

Netherlands Retail Sales -0.1% SEPT Y/Y vs 0.9% AUG

Iceland Unemployment Rate 5.2% OCT vs 4.9% SEPT

Russia Producer Prices 8.8% OCT Y/Y vs 11.6% SEPT

Russia Industrial Production 1.8% OCT Y/Y vs 2.0% September

Russia Preliminary Q3 GDP 2.9% Y/Y vs 4.0% in Q2

Estonia Preliminary Q3 GDP 1.7% Q/Q vs 0.5% in Q2 [3.4% Y/Y vs 2.2% in Q2]

Estonia Unemployment Rate 5.8% OCT vs 5.7% SEPT

Estonia Unemployment Rate 9.7% in Q3 vs 10.2% in Q2

Latvia Unemployment Rate 13.5% in Q3 vs 16.1% in Q2

Hungary Industrial Production 0.6% SEPT Y/Y vs 1.8% AUG

Slovenia Unemployment Rate 11.5% SEPT vs 11.6% AUG

Turkey Consumer Confidence 85.7 OCT vs 88.8 September

Turkey Unemployment Rate 8.8% AUG vs 8.4% JUL

Interest Rate Decisions:

(11/14) Iceland Sedlabanki Interest Rate HIKED 25bps to 6.00%

Matthew Hedrick

Senior Analyst