TODAY’S S&P 500 SET-UP – November 13, 2012

As we look at today's setup for the S&P 500, the range is 39 points or 1.16% downside to 1364 and 1.66% upside to 1403.

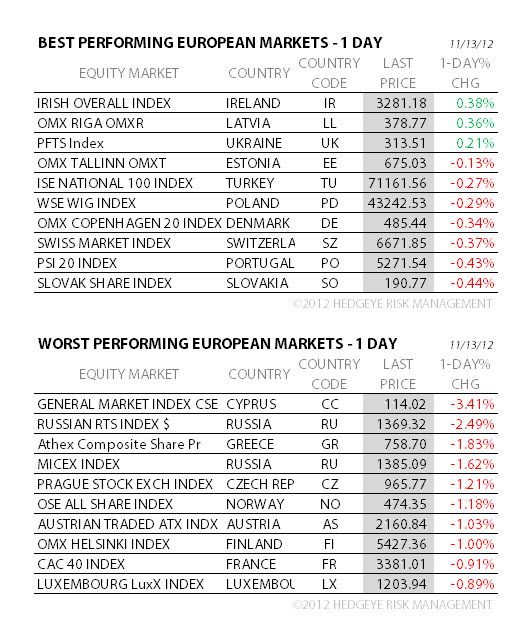

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.35 from 1.35

- 10YR – got #GrowthSlowing? Treasuries ripping since Election Day with the UST 10yr yield testing its August low here this morn at 1.58%; good spot to sell some of your Fixed Income gross long exposure and buy US and German stocks provided that 1364 TAIL risk line for SPX holds.

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30am: NFIB Small Bus. Optimism, Oct., est. 93 (prior 92.8)

- 7:45am: ICSC weekly sales

- 8:55am: Johnson/Redbook weekly sale

- 10am: IBD/TIPP Economic Optimism, Nov., est. 54 (prior 54)

- 11am: Fed to purchase $4.35b-$5.25b notes due 11/15/18-8/15/20

- 11:30am: U.S. Treasury to sell $32b 3-mo. bills, $28b 6-mo. bills

- 2pm: Monthly Budget Statement, Oct., est. -$113b (prior -$98.5)

- 3:30pm: Fed’s Yellen speaks at Berkeley

GOVERNMENT:

- Congress returns for post-election “lame duck” session

- Bloomberg Government, National Defense Industrial Association hold webinar on “Post-Election Sequestration,” 2pm

- Geithner speaks at WSJ CEO Council conference, 4pm

- Inter-American Development Bank holds second day of the 36th meeting of the network of Central Banks and Finance Ministers

- ITC may announce review of judge’s findings that companies infringe patents owned by Vitec Group’s Litepanels for LEDs, 5pm

WHAT TO WATCH

- Europe gives Greece extra time, spars with IMF on debt plan

- Spanish yields climb to six-week high

- Microsoft’s Sinofsky departs as Larson-Green ascends at Windows

- U.K. inflation quickens more than forecast on tuition fees

- Kodak gets $793m in financing to exit bankruptcy by mid-2013

- Weatherford finds material weakness in internal controls

- NBC Universal said to cut ~450 jobs across several units

- Fiat must pay $342m for Chrysler stake, retiree fund says

- Vodafone, Verizon Communications get $8.5b from venture

- NYSE computer issue leads to no closing auction in 216 stocks

- Goldman said to promote 70 to partner, lowest in yrs, WSJ says

- Goldman said to plan exit from asset management in Korea

EARNINGS

- Home Depot (HD) 6am, $0.70 - Preview

- Quebecor (QBR/B CN) 6am, C$0.73

- AECOM Technology (ACM) 6:30am, $0.82

- AuRico Gold (AUQ CN) 7am, $0.05

- Michael Kors (KORS) 7am, $0.40

- Dick’s Sporting Goods (DKS) 7:30am, $0.37

- Saks (SKS) 8am, $0.12

- Baytex Energy (BTE CN) 8am, C$0.31

- Shoppers Drug Mart (SC CN) 8:28am, C$0.81

- TJX Cos (TJX) 8:32am, $0.61

- Woodward (WWD) 4pm, $0.57

- Wesco Aircraft Holdings (WAIR) 4:01pm, $0.24

- Cisco Systems (CSCO) 4:04pm, $0.46

- Osisko Mining (OSK CN) 4:05pm, C$0.05

- Giant Interactive (GA) 4:30pm, $0.19

- Silvercorp Metals (SVM CN) 5pm, $0.07

- Renren (RENN) 6pm, $0.05

- Chartwell Seniors Housing REIT (CSH-U CN) 6:06pm, C$0.20

- IAMGOLD (IMG CN) Post-Mkt, $0.24

- B2Gold (BTO CN) Post-Mkt, $0.05

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Oil Drops on Signs of Rising U.S. Supply, Reduced Demand Outlook

- Chocolate Rush Hits Record as Cocoa Shortages Loom: Commodities

- Platinum, Palladium Shortage Most in a Decade on Falling Supply

- Copper Declines on Greece Funding Delay, China Output Data

- Gold Drops in New York Trading as Stronger Dollar Curbs Demand

- Soybeans Rebound as Drop to Four-Month Low May Spur Purchases

- Gold to Climb to $1,849, LBMA Survey Shows, as Outlook Cut

- Sugar Resumes Drop as Commodities Slide on Europe; Coffee Falls

- Shanghai Rebar Drops for First Time in Three Days on Winter Risk

- Raw Material Prices Squeezing Aluminum Producers: Bear Case

- U.K. Regulators Probe Allegations of Price-Fixing in Gas Market

- Iron-Ore Rebound Boosts STX With Record Chinese Imports: Freight

- China Oil Production Rises to Record on Demand From Refiners

- North Sea Buzzard Field Said to Resume Oil Flows Late Yesterday

CURRENCIES

EUROPEAN MARKETS

RUSSIA – back into crash mode we go with the RTSI leading losers in Europe this morning, -1.3% (down 20.9% since #GrowthSlowing started, globally, in March. We’ll keep writing that btw, because A) its true and B) its rarely highlighted as true by consensus bulls within the context of the SEP Bernanke Top.

ASIAN MARKETS

CHINA – Shanghai Comp gets spanked, down -1.5% overnight and down for the 6th day in the last 7; “China has bottomed” crowd quiet as the Chinese don’t behave like Krugman. Chinese stocks -16.8% since #GrowthSlowing started, globally, in March.

MIDDLE EAST

The Hedgeye Macro Team