A victim of its early success: most metrics down YoY

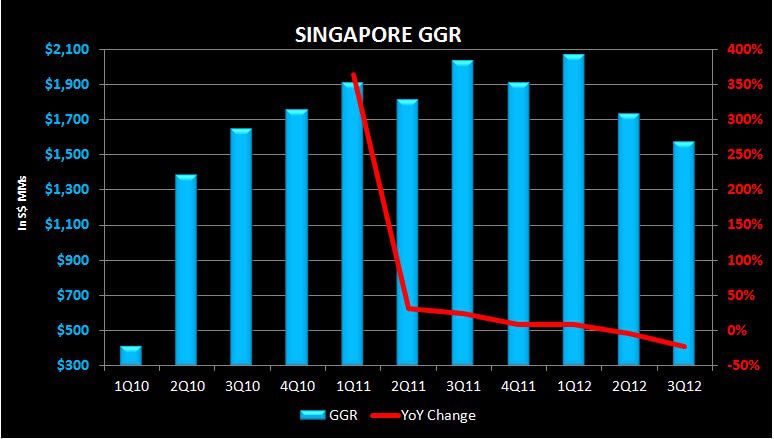

Singapore’s gaming metrics continue to decline in Q3 as gross gaming revenues fell to the lowest level since 2Q 2010. For comparison, Macau hit a new quarterly record in 3Q. Q3 hold in Singapore was 2.27%, the lowest quarterly hold rate ever and way below Singapore’s historical hold rate of 2.99%. Hold in 3Q 2011 was 2.90%. If we use 3% to normalize VIP revenues in 3Q 2012 and 3Q 2011, GGR would have been S$1.77BN, which is down 14% YoY and 3% QoQ.

3Q gross gaming revenues fell 23% YoY and 9% QoQ to S$1.57 billion. Not since MBS’s grand opening has revenues been this low. RWS GGR share rose 1.6% QoQ to 50.8%.

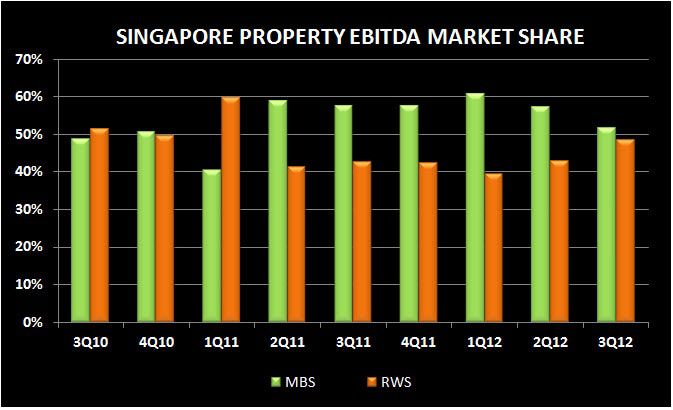

RWS gained 3% points in net gaming revenue share to 47.3%. This is the 2nd consecutive quarterly gain for RWS.

Total property EBITDA experienced its 2nd consecutive YoY and QoQ decline to S$629 million, falling 29% YoY and 14% QoQ. RWS’s EBITDA share jumped 5.6% points to 48.3%.

For the 4th consecutive quarter, RC turnover declined YoY. RC turnover was S$27.6BN, down 25% YoY and 1% QoQ. RWS’s RC share was 46.6%, down 0.8% points QoQ, marking the 3rd consecutive quarter of declines.

Mass revenue was flat QoQ as hold reached a new high of 23.52%. Market shares were basically unchanged.

Mass drop fell QoQ (6%) for the 1st time. RWS gained 1.4% points in share to 46.8%.

Slot win slipped 4% QoQ and slot win per slot per day reached a record low of S$718. RWS gained 1.1% QoQ in slot win share.