-- For specific questions on anything Europe, please contact me at to set up a call.

No Current Real-Time Positions in Europe

Asset Class Performance:

- Equities: The STOXX Europe 600 closed down -1.7% week-over-week vs +1.6% last week. Bottom performers: Spain -4.2%; Italy -3.7%; Russia (RTSI) -3.0%; Germany -2.7%; Finland -2.7%; France -2.0%; Austria -2.0%; UK -1.7%. Top performers: Turkey +0.6%; Slovakia +0.5%; Switzerland +0.2%. [Other: Greece +0.0%].

- FX: The EUR/USD is down -0.94% week-over-week. W/W Divergences: TRY/EUR +1.01%; NOK/EUR +0.83%; SEK/EUR +0.43%; GBP/EUR +0.18%; CHF/EUR +0.10%; DKK/EUR +0.02%; HUF/EUR -0.44%; CZK/EUR -0.46%; PLN/EUR -1.17%.

- Fixed Income: The 10YR yield for sovereigns were mixed week-on-week. Portugal rose the most at +51bps to 8.86%, followed by Spain +23bps to 5.83%. Greece saw the largest decline at -34bps to 17.87%. Germany, Belgium, and France were notable decliners, falling -12bps, -11bps, and -9bps to 1.33%, 2.31%, and 2.13%, respectively.

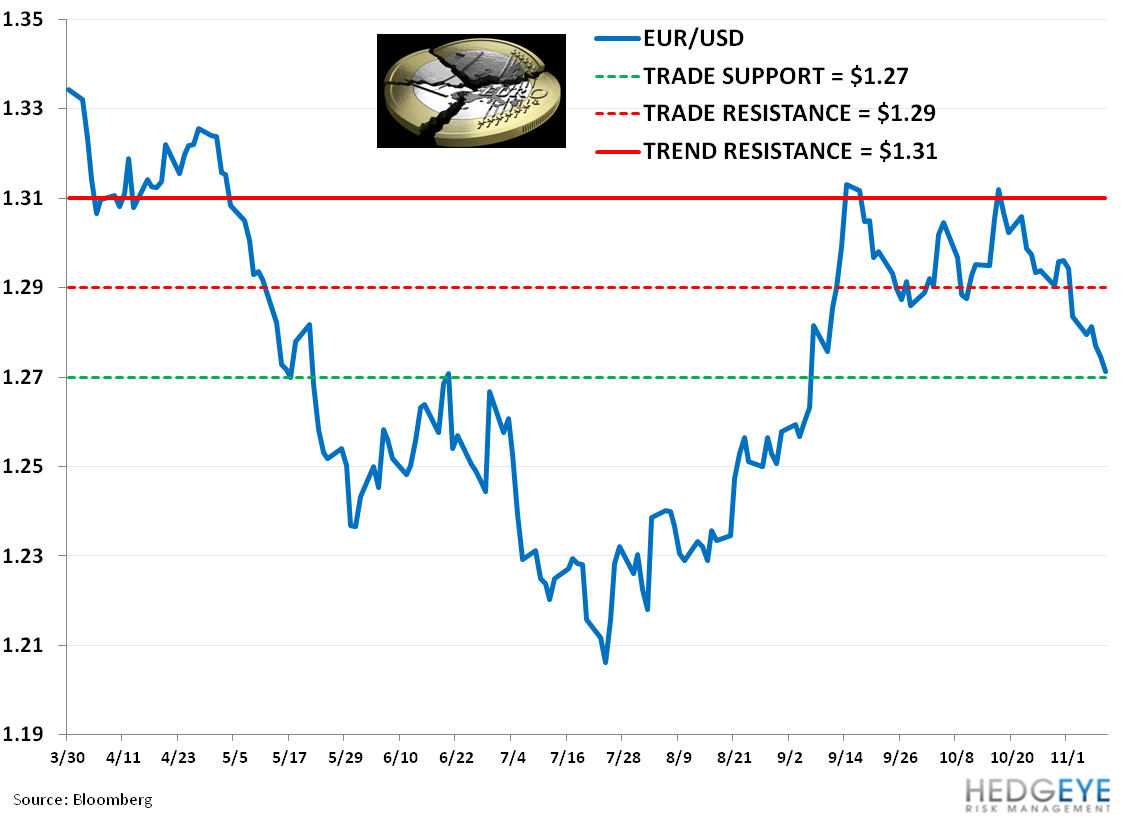

- The EUR/USD hit its lowest level in 2 months this week. We maintain an immediate term TRADE range of $1.27 to $1.29 and a heavy intermediate term TREND resistance level of $1.31.

The Eurocrat Shuffle:

The Eurozone continues to take two steps forward and one step back, or is it, one step forward and two steps back? Headline risk continues to be a governing factor. This week it largely revolved around Greece – waiting on the narrow passage of a €13.5B package of spending cuts, tax increases and structural reforms late Wednesday night and ahead of Sunday’s vote on its 2013 budget.

Markets remained constipated over Greece’s next lifeline aid tranche of €31.5B, as the European Commission, Eurogroup, and IMF are in disagreement about how to both reduce Greece’s debt load and set appropriate debt reduction targets for such far-out dates as 2020. On some level an agreement to both will be needed before the money is dropped from the skies. [See our note titled “November ECB Presser: No Surprises” for our commentary on the ECB’s decision to keep rates on hold this week.]

Away from the politically compromised Eurocrats and structural flaws of the Eurosystem, Keith noted that his multi-factor quantitative model was flashing a major buy signal for the German DAX. [Note: we sold our Real-Time Position in German Bonds (BUNL) on Thursday (11/8) so we have no exposure to Europe]. He also said that the broader equity market of Denmark looks good; whereas the UK is flashing a negative set-up.

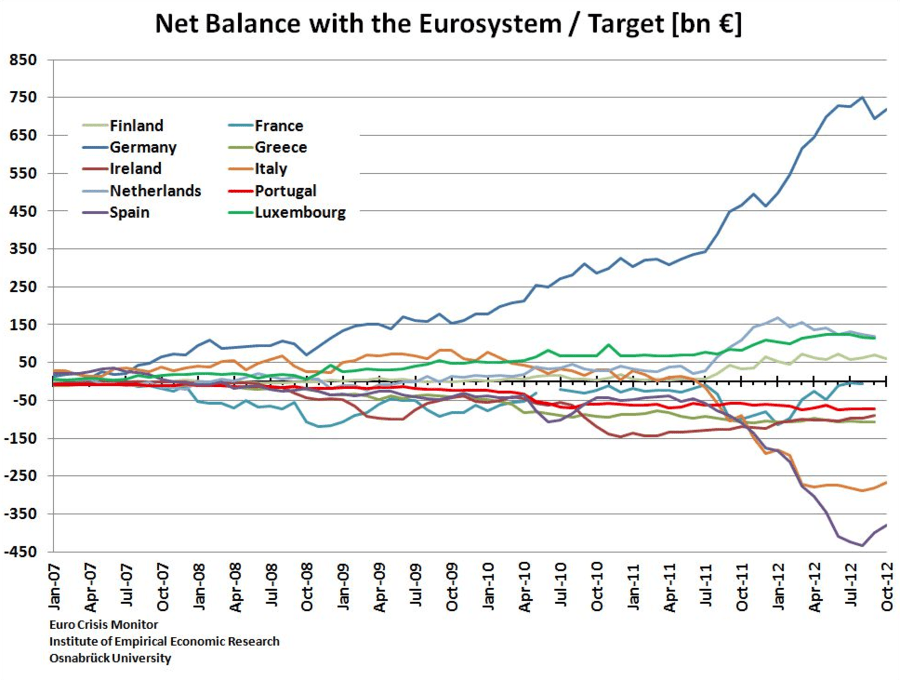

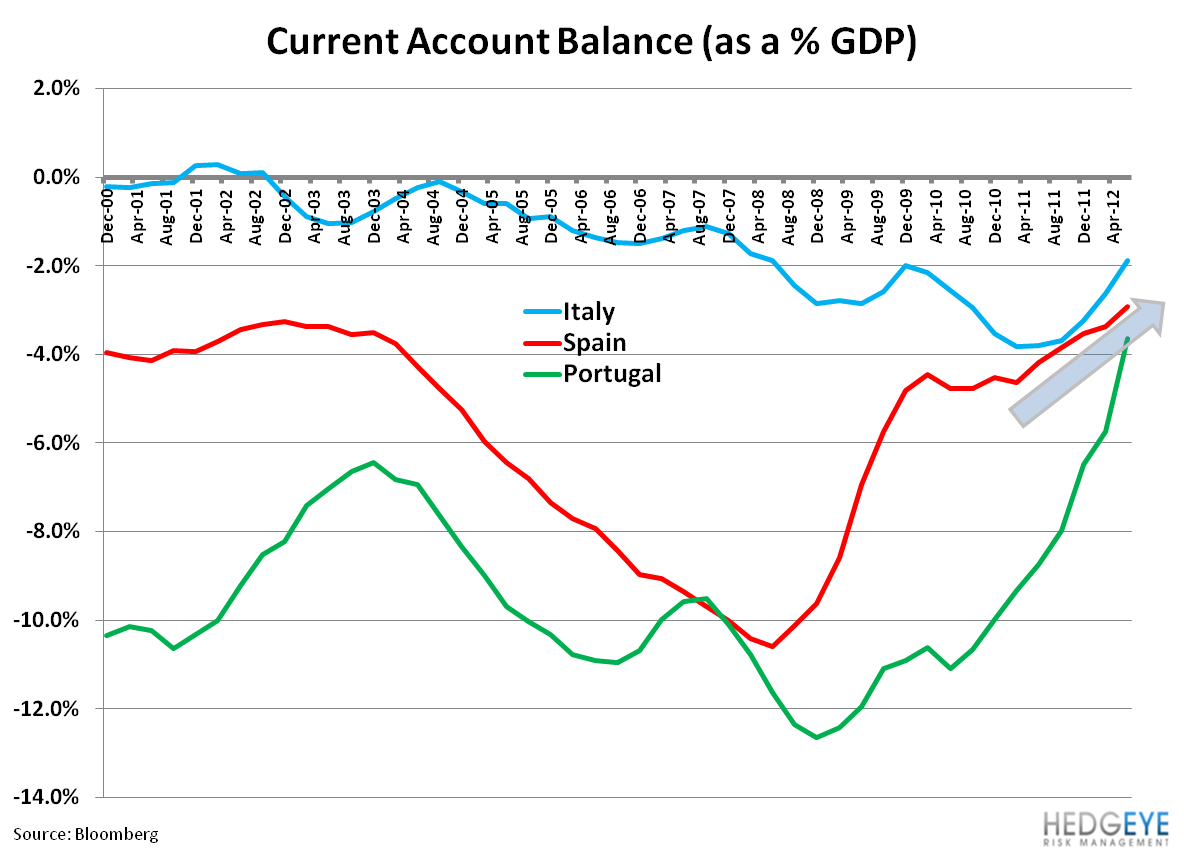

Beyond the headline news, and broader negative data out this week (see below in the section “Data Dump”), there were a couple positive charts that caught our attention this week:

- Target 2 exposure is actually slowly improving across the periphery.

- Current Account Balances are showing improvement across countries that have historically had heavy deficits.

The European Week Ahead:

Monday: Eurogroup Meeting in Brussels; Oct. Germany Wholesale Price Index (Nov. 12-13); Oct. UK RICS House Price Balance; Sep. Spain House Transactions

Tuesday: Nov. Eurozone ZEW Survey Economic Sentiment; Nov. Germany ZEW Survey Current Situation and Economic Sentiment; Oct. UK PPI Input and Output, CPI, Retail Price Index; Sep. UK ONS House Price; Oct. France CPI - Final; Sep. France Current Account; 3Q France Wages and Non-Farm Payrolls – Preliminary; Oct. Italy CPI - Final; Sep. Italy General Government Debt

Wednesday: Sep. Eurozone Industrial Production; BoE Inflation Report; Oct. UK Claimant Count Rate, Jobless Claims Change; Sep. UK Weekly Earnings, ILO Unemployment Rate, Employment Change; Oct. France Consumer Price Index; 3Q Greece GDP - Advance

Thursday: ECB Publishes Nov. Monthly Report; Oct. Eurozone CPI; 3Q Eurozone GDP – Advance; 3Q Germany GDP – Preliminary; Oct. UK Retail Sales; 3Q France GDP – Preliminary; Spain Catalonia Regional Election; 3Q GDP - Final 3Q Spain GDP – Final; Sep. Italy Current Account; 3Q Italy GDP - Preliminary

Friday: Sep. Eurozone Current Account, Trade Balance; Sep. Italy Trade Balance

Extended Calendar:

NOV 19 – Eurozone Finance Ministers Meeting

NOV 22 – EU Summit and ECB Governing Council Meeting

NOV 26 – Finance Ministers may sign off on Greece’s next bailout tranche, 31.5B EUR

NOV 27 – AFME 4th Annual Spanish Funding Conference in Madrid

DEC 1 – Beginning of the Russian Presidency of G20

DEC 3 – Eurogroup Meeting in Brussels

DEC 6 – ECB Governing Council Meeting

DEC 12-13 – First public consultation between the Russian government, B20 Coalition and international civil society representatives on G20 agenda for 2013 (in Moscow)

DEC 20 – ECB Governing and General Council Meeting

APR 2013 – Parliamentary elections in Italy

MAY 2013 – Presidential elections in Italy

Call Outs:

Turkey - received its first investment- grade ranking since 1994 after Fitch Ratings raised the country by one level (BB+ to BBB-), citing an easing in economic risk and lower debt.

Italy - Italian Treasury officials rejected proposals to create a so-called bad bank for the non-performing loans of the nation’s lenders amid concern the plan would strengthen the link between sovereign and bank debt, said people with knowledge of the matter.

France - the IMF warned that France risks falling behind the likes of Spain and Italy if it does not reform its economy. It called for a comprehensive program of structural reforms, citing the country's significant loss of competitiveness.

Data Dump:

Eurozone PPI 2.7% SEPT Y/Y vs 2.7% AUG

Eurozone Retail Sales -0.8% SEPT Y/Y vs -0.9% AUG

Eurozone Sentix Investor Confidence -18.8 NOV (exp. -21) vs -22.2 OCT

UK Halifax House Price -1.7% OCT Y/Y vs -1.2% September

UK New Car Registrations 12.1% OCT Y/Y vs 8.2% September

UK Industrial Production -2.6% SEPT Y/Y vs -1.0% AUG

UK Manufacturing Production -1.0% SEPT Y/Y vs -1.2% AUG

Germany CPI 2.1% OCT Final Y/Y UNCH [0.1% M/M UNCH]

Germany Exports -2.5% SEPT M/M vs 2.3% AUG

Germany Imports -1.6% SEPT M/M vs 0.4% AUG

Germany Industrial Sales -1.2% SEPT Y/Y vs -1.3% AUG

Germany Factory Orders -4.7% SEPT Y/Y vs -4.6% AUG [-3.3% SEPT M/M vs -0.8% AUG]

France Bank of France Business Sentiment 92 OCT vs 92 SEPT

France Industrial Production -2.5% SEPT Y/Y vs -0.9% AUG

France Manufacturing Production -2.5% SEPT Y/Y vs -0.3% AUG

Italy Industrial Production SA -1.5% SEPT Y/Y vs 1.7% AUG

Italy Industrial Production WDA -4.8% SEPT Y/Y vs -5.2% AUG

Italy Industrial Production NSA -10.5% SEPT Y/Y vs -5.1% AUG

Spain Industrial Output NSA -11.7% SEPT Y/Y vs -2.5% AUG

Spain Unemployment Change 128.2k OCT M/M (exp. 110k) vs 79.6k SEPT

Norway Industrial Production -5.0% SEPT Y/Y vs 1.9% AUG

Norway CPI 1.1% OCT Y/Y vs 0.5% SEPT

Norway CPI incl. oil 1.7% OCT Y/Y vs 1.4% SEPT

Finland Industrial Production -1.7% SEPT Y/Y vs -1.4% AUG

Sweden Industrial Production -5.0% SEPT Y/Y vs 2.7% AUG

Switzerland Unemployment Rate 3.0% OCT vs 2.9%

Switzerland CPI -0.1% OCT Y/Y vs -0.3% SEPT

Austria Wholesale Price Index 4.2% OCT Y/Y vs 4.2% SEPT

Netherlands CPI 2.9% OCT Y/Y vs 2.3% SEPT

Netherlands Industrial Production -0.2% SEPT Y/Y vs -0.6% AUG

Greece Unemployment Rate 25.4% AUG vs 24.8% JUL

Greece Industrial Production -7.3% SEPT Y/Y vs 2.5% AUG

Greece CPI 1.6% OCT Y/Y vs 0.9% September

Ireland CPI 2.1% OCT Y/Y vs 2.4% SEPT

Ireland Industrial Production -12.7% SEPT Y/Y vs -0.5% AUG

Portugal Industrial Sales -8.1% SEPT Y/Y vs -1.3% AUG

Russia Consumer Prices 6.5% OCT Y/Y vs 6.6% SEPT

Czech Republic Unemployment Rate 8.5% OCT vs 8.4% SEPT

Czech Republic Retail Sales -3.3% SEPT Y/Y vs -0.8% AUG

Czech Republic CPI 3.4% OCT Y/Y vs 3.4% September

Romania Retail Sales 5.1% SEPT Y/Y vs 4.7% AUG

Hungary Industrial Production 0.6% SEPT Y/Y vs 1.8% AUG

Slovenia Industrial Production -0.2% SEPT Y/Y vs 4.2% AUG

Latvia Preliminary Q3 GDP 5.3% Y/Y vs 5.0% in Q2 [1.7% Q/Q vs 1.3% in Q2]

Turkey Consumer Prices 7.80% OCT Y/Y vs 9.19% SEPT

Turkey Producer Prices 2.57% OCT Y/Y vs 4.03% September

Turkey Industrial Production 6.2% SEPT Y/Y vs 0.9% AUG

Interest Rate Decisions:

(11/8) BOE Main Interest Rate UNCH at 0.50% (and asset purchase program UNCH)

(11/8) ECB Main Interest Rate UNCH at 0.75%

(11/8) Serbia Repo Rate HIKED to 10.95% from 10.75% (exp. 11%)

(11/9) Russia Refinancing Rate UNCH at 8.25%

(11/9) Russia Overnight Deposit Rate UNCH at 4.25%

(11/9) Russia Overnight Auction-Based Repo UNCH at 5.50%

Matthew Hedrick

Senior Analyst