Some discounting but overall still solid pricing

Various Caribbean and Europe itineraries saw some discounting in the last month, but that was offset by pricing improvements in other regions. Costa pricing remains steady in Europe while its venture into Asia has garnered solid pricing. We see pricing strength in the very close-in Caribbean bookings for CCL’s F4Q. Overall, F1Q pricing for RCL and CCL continue to exhibit weakness but both companies stressed F1Q will be a difficult quarter due to tough comps pre-Costa Concordia. The good news for F1Q is that Asia Pacific/South America/Mexico account for ~30% of the total itineraries and those regions have had better pricing. For early F2Q, pricing trends improved for Alaska, Asia Pacific and Mexico while Europe pricing remained status quo in November.

While the ‘Sandy and Athena’ card could be effectively used by Carnival and Royal Caribbean to mask weak F1Q 2013 guidance, the rest of 2013 remains to be seen until the upcoming Wave Season. Although there will surely be bumps along the road, we continue to be encouraged by the pricing stability out of Europe, a relatively low capacity environment and better visibility due to higher booking volumes.

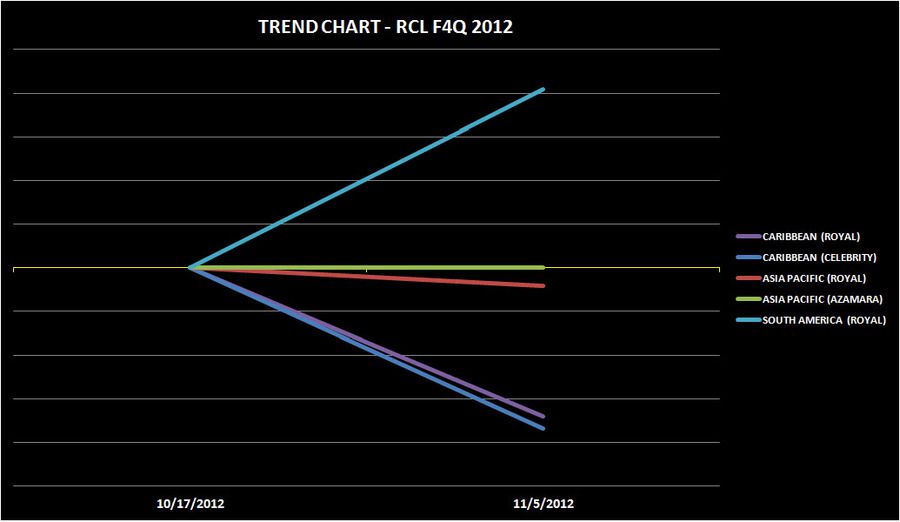

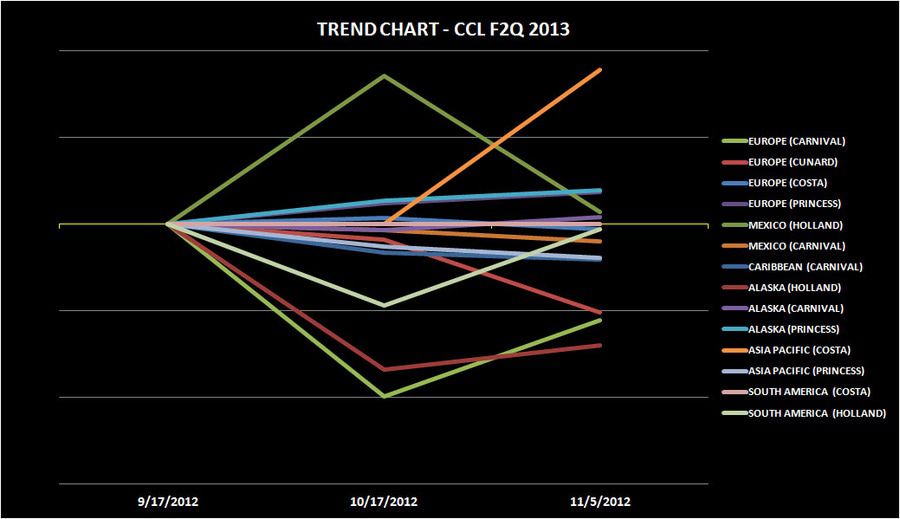

Here are some conclusions from our cruise pricing survey completed this week. The charts below track pricing trends on a relative basis—i.e. prices relative to that seen on the last earnings call (RCL – Oct 25, CCL –Sept 25).

FQ4 2012

- Caribbean

- Pricing was mixed in November. For the very last-minute bookings, the Carnival brand continues to improve on pricing in spite of Sandy. RCL brand pricing wasn’t so lucky but given Celebrity’s strength pre-Sandy, the Caribbean may still retain the top spot in yield growth.

- Europe

- Most of the Costa itineraries maintained their pricing; discounting in a couple of Spanish itineraries pushed overall pricing a tad lower.

- Asia Pacific

- Not much movement from October to November

FQ1 2013

- Caribbean

- Royal and Celebrity pricing both slipped in November. While modestly negative YoY, Carnival’s pricing improved slightly in November.

- Europe

- Cunard pricing dropped as this brand has had trouble maintaining price in the past few months

- Asia Pacific

- Royal and Azamara both saw a tick up in November

- South America

- Overall positive, as strong Royal brand pricing offset weakness in Celebrity pricing

- Mexico

- Carnival brand remains steady, while Holland improved in November.

FQ2 2013

- Caribbean

- RCL brand pricing was unchanged, while Carnival brand pricing was slightly lower.

- Europe

- RCL: Mixed—Prices were raised for the RCL brand while lowered for Celebrity. The changes, however, are not material. Celebrity pricing continues to be better than Royal on a YoY basis.

- CCL: not much price change on Costa.

- Alaska

- RCL: Celebrity is lower but trend is improving.

- CCL: Mixed—Holland prices are lower YoY but the trend is improving while Princess prices are higher YoY but the trend is declining.

- Asia Pacific

- RCL: While only a handful of itineraries, the trend has been positive.

- CCL: Princess is treading along while Costa is nicely higher.

- South America

- Fairly stable pricing

- Mexico

- Strong pricing in the Carnival brand