“Buying is a profound pleasure.”

-Simone de Beauvoir

You want to buy when people are forced to sell.

If you proactively prepare for these manic market moments: A) you have cash and B) your buy list is locked and loaded. While your shopping list may not be as long as it was 2 months ago, that’s ok. I’m picky about what I buy too.

Back to the Global Macro Grind…

In New Haven, CT, rain, wind, or snow, this is what we call The Flush. That’s when you “break” a couple of the moving monkey lines (50 and 200 day simple moving averages) and you get to capitalize on your competition’s emotional selling mistakes.

I’m not saying “buy everything.” Neither am I saying everything is fixed. I am simply saying that everything in markets has a time and price. From a purely quantitative perspective, this morning’s Macro Grind is signaling the best time to sell bonds and buy stocks in 2 months.

Why?

- BONDS – US Treasuries (10yr immediate-term TRADE oversold at 1.60% yield) and German Bunds are overbought

- CURRENCIES – The Euro (EUR/USD) is immediate-term TRADE oversold at $1.27 (still bearish TREND)

- STOCKS – The SP500 is holding my long-term TAIL risk line of 1364 support

*Note: I don’t use the moving monkey other than for entertainment purposes.

Also note that the main reason for the word “buy” being in the title of my note is not “China has bottomed.” As we have said, multiple times, China’s bottom will be a process, not a point. The Shanghai Composite was just down for the 5th day in a row (down -16% since growth slowing began, globally, in March). Peculiar looking bottom to me.

As a Chaos Theorist who uses Bayesian conditional probability theory in my decision making process, it’s also critical to note that if we snap my 1364 TAIL risk line today (and close there), I reserve my Canadian and US Constitutional right to change my mind.

But, for now – let’s not stress out about that. We don’t have to. We didn’t buy the Bernanke Top (September 14th). Neither do we have to be up +32% (from here) to get back to break-even buying AAPL at its all-time high.

We’ve earned the opportunity to be patient (picky) here, and take our time.

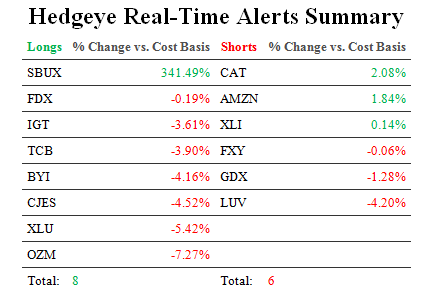

Top 3 Long Ideas?

1. International Game Tech (IGT) – Always start with what’s working. In a growth and #EarningsSlowing market like this, you should pay more for the growth that you can find. Visibility matters. Todd Jordan said IGT delivered the bacon last night, beating handily on both the top and bottom line, so buy more (email for Jordan’s note)

2. Starbucks (SBUX) – Back to the old well works for me, big time – especially now that one of America’s top capitalist innovators (CEO Howard Schultz) looks forward to selling you his Verisimo machine domestically for holiday, and continues to have one of the most visible expansion plans, globally, of a legal drug. Coffee price deflation is a big margin kicker too.

3. Federal Express (FDX) - As the world bakes a potential recession into the expectations cake, you want to be buying high-quality (non-mining capex bubble) cyclicals that have already guided down. Especially with our short Oil call working, the margin of safety buying FDX improves (email for Van Sciver’s slide deck presentation)

You’ll also note that my Top 3 Long Ideas are US Equities. That could change if German, Dutch, or Taiwanese Equities flash my immediate-term TRADE oversold signal. They have not yet. The Post Election Flush, is very American.

Whoever bought US stocks at the YTD top needs to be up, a minimum +7.5% (from here), to get back to that September 14th break-even. With the Russell2000 down -8.3% over the same 2 months, you’d have to be up +9% to get back to break-even there. With real money, timing matters. Return of your money is geometric.

This is why we are so focused on earning your respect as the top risk management source you have in your inbox every morning. Buying is a pleasure. We get it. But someone also needs to tell you when to sell. Put another way, as one of my best investors reminded me in NYC yesterday, “Keith, your job isn’t to make me rich – it’s to keep me rich.”

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, EUR/USD, UST 10yr Yield, IGT, SBUX, FDX, and the SP500 are now $1, $105.22-108.44, $80.41-81.12, $1.27-1.29, 1.60-1.72%, $12.69-13.73, $49.27-54.21, $89.21-91.98, and 1, respectively.

Enjoy the weekend and best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer