TODAY’S S&P 500 SET-UP – November 09, 2012

As we look at today's setup for the S&P 500, the range is 46 points or 0.98% downside to 1364 and 2.36% upside to 1410

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

YIELD CURVE – as of this morning 1.34 decreased from prior day's trading at 1.36

BONDS – We’ve gone back and forth with clients on this one all yr and maintained that the most obvious bull market remains in bonds, provided that we remain right on both US/Global Growth surprising on the downside; at 1.61% on the 10yr, UST’s finally give us the immediate-term TRADE overbought bond signal here (German and Belgian Bonds overbought as well).

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Import Price Index M/m, Oct. est. 0.0% (prior 1.1%)

- 8:30am: WASDE agricultural data

- 9:55am: U. of Michigan Conf., Nov. est. 83.0 (prior 82.6)

- 10am: Wholesale Inventories, Sept. est. 0.4% (prior 0.5%)

- 10am: Fed’s Duke speaks in Chicago

- 11am: Fed to buy $1b-$1.5b TIPS due 1/15/19-2/15/42

- 1pm: Baker Hughes rig count

GOVERNMENT:

- SEC Enforcement Director Robert Khuzami speaks in N.Y., 9am

- National Committee to Preserve Social Security & Medicare holds conference call briefing on proposed benefit cuts, with Sen. Bernie Sanders, I-Vt, 11am

- IRS holds a public forum on proposed regulations relating to branded prescription drug fee imposed by Affordable Care Act

WHAT TO WATCH:

- CME Group sued CFTC, challenging cleared-swaps reporting requirements imposed under Dodd-Frank legislation

- President Obama expected to issue statement today on his plan for spurring economic growth, reducing deficit

- To hold first post-election news conference early next week

- NY federal judge to consider arguments today over whether to give Visa, MasterCard’s proposed $7.25b settlement of merchant fee price-fixing case prelim. approval

- BP, plaintiffs ask judge to approve $7.8b spill accord

- BofA’s Merrill Lynch unit must face lawsuit by FHFA over mortgage-backed securities sold by the bank

- Whistle-blower helping U.S. mount $1b fraud lawsuit against BofA accused of fraud by investor in financing co. he co-founded

- BNY Mellon reached deal to end lawsuit accusing it of defrauding state pension funds through forex transactions

- China passenger-vehicle sales rose in Oct., beat est.

- Lockheed’s F-35 jets may cost $1.26b for fixes

- U.S. Fiscal Cliff, China Exports, Cisco: Week Ahead Nov. 10-17

EARNINGS

- Alliant Energy (LNT) 6:00am, $1.30

- Enerplus (ERF CN) 6:00am, C$0.06

- TMX Group (X CN) 6:00am, C$0.74

- Covidien (COV) 6:00am, $1

- GMP Capital (GMP CN) 6:00am, $(0.03)

- JC Penney (JCP) 6:00am, $(0.07)

- HeartWare (HTWR) 6:30am, $(1.52)

- Foster Wheeler (FWLT) 6:45am, $0.45

- Stella-Jones (SJ CN) 7:00am, $1.26

- GenOn Energy (GEN) 7:00am, $0.03

- MGIC Investment (MTG) 7:00am, $(0.74)

- Warner Chilcott (WCRX) 7:00am, $0.79

- Apollo Global Management (APO) 7:08am, $0.76

- Laredo Petroleum Holdings (LPI) 7:26am, $0.13

- EW Scripps (SSP) 7:30am, $0.11

- Brookfield Asset Management (BAM/A CN) 8:00am, $0.30

- Telus (T CN) 8:01am, C$1.07

- Ameren (AEE) 8:15am, $1.41

- Emera (EMA CN) 9:48am, C$0.36

- Medivation (MDVN) 4:09pm, $(0.10)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Set for Best Week Since January on Stimulus Prospects, ETPs

- Gold Traders More Bullish After Obama’s Re-Election: Commodities

- Sugar Declines in London on Brazilian Supplies; Cocoa Rises

- Gold Demand in India Seen Rebounding on Festivals, Price Decline

- Copper Heads for Fifth Weekly Decline on European Growth Concern

- Corn Top Commodity Pick at Morgan Stanley as U.S. Supply Shrinks

- Rubber Gains, Paring Weekly Loss, on Signs of Economic Recovery

- Indonesia Palm Oil Group Wants Tax Changes to Counter Malaysia

- Oil Trades Near Four-Month Low on Demand Concern, Supply Growth

- Copper Inventories in Shanghai Climb to Highest Since April

- Canada’s New Corn Belt Attracts Hot Money to Bargain Farmland

- California Carbon ‘Crippled’ by Buyer Hesitation: Energy Markets

- China’s High-Cost Aluminum Producers Limit Output Declines

- Gold Traders More Bullish After Obama’s Win

- Sugar Fee for Thailand Climbing as Futures Slump to Two-Year Low

CURRENCIES

EURO – euro $1.27 is ugly, but also immediate-term TRADE oversold; get the EUR/USD right, you get a lot of things big beta right; so today’s currency signal, like our bond signal, says buy stocks that can deliver on the numbers (yes, there are far fewer of those today than 2 months ago). Top 3 Ideas from here: IGT, SBUX, FDX (long).

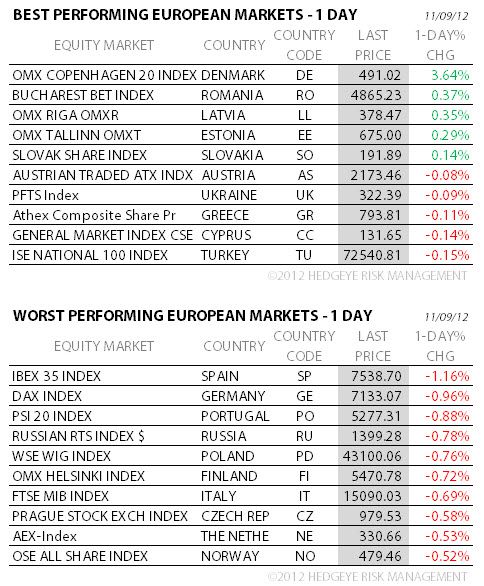

EUROPEAN MARKETS

ASIAN MARKETS

CHINA – unfortunately, for team “China has bottomed”, China is not the reason for us being more bullish than we have in 2 months this morn – everything has a time and price, but Chinese stocks were down for the 5th consecutive day and remain in a Bearish Formation as China refuses to deliver the Western hope for stimuli.

MIDDLE EAST

The Hedgeye Macro Team