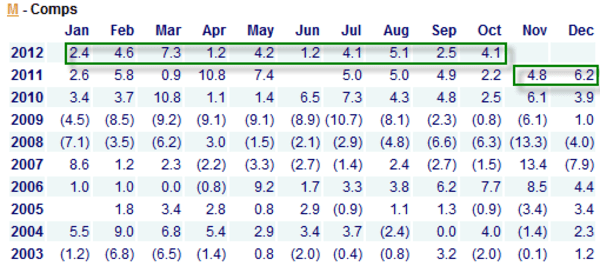

We’re seeing more downside in Macy’s (M) than upside these days. The company is comping well right now thanks to the success of My Macy’s and the Millennial Stores. The stock is trading at 5.5x EBITDA today but could be seen as trading at 8.5x earnings if you factor in things like gross margin leverage. Would you really pay 8.5x/5.5x for a department store stock assuming that everything goes according to plan without any hiccups? That’s a risky bet considering that no one can keep comping up forever and JCPenney (JCP) is a credible threat to Macy’s. Hence, we’re increasingly bearish on the stock moving forward in Q4.

From Retail Sector Head Brian McGough:

“This a business that has no square footage growth, no ‘birthright to comp’ in its core, struggles to consistently earn its cost of capital (what happens when lease accounting rules change and M has to account for its property?), and has zero competitive advantage in the core area that will be driving incremental consumer purchases for generations to come – dot.com.”