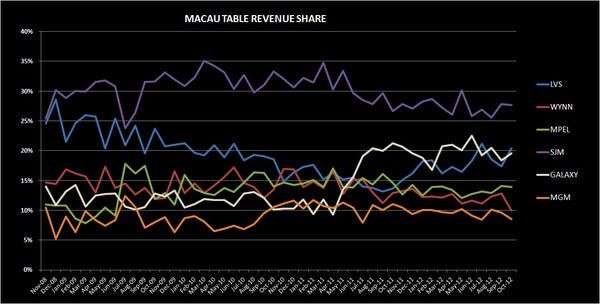

Gross gaming revenue (GGR) was up +3.5% in Macau for October, at the high end of our forecast for the month. VIP hold was down but mass volume grew. We think that November growth will pick up with 7-14% growth year-over-year and will accelerate into December. So with Macau volumes and revenues picking up, who’s the winner? Las Vegas Sands (LVS). They put up the best GGR growth and largest market share on a month-over-month basis. LVS reached a three year high in market share on Mass revenue and a 2 year high in slot market share. LVS remains one of our top long ideas.

On the other side, Wynn Resorts’ (WYNN) market share set an all-time low of just 10.1% because of lower hold. A freidnly reminder: house hold is the measure of the amount of money a casino table game keeps from the total amount of money that is dropped into the game's cash box. MGM and SJM also had low hold. As for Galaxy and MPEL, they put up solid mass growth yet again.