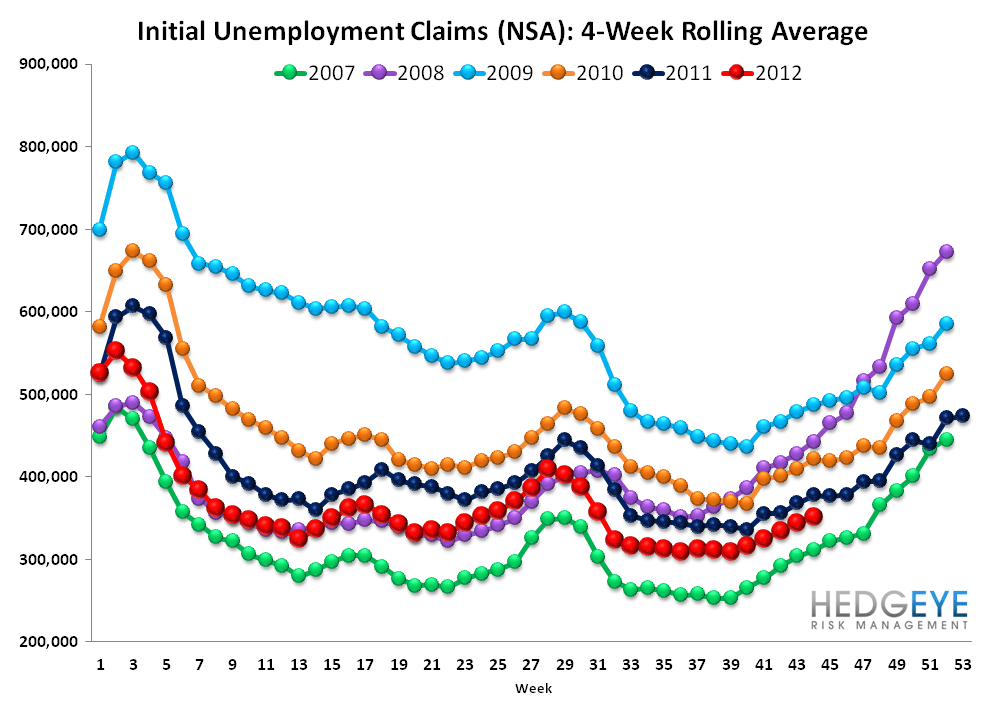

Seasonally-adjusted vs. Non-seasonally-adjusted

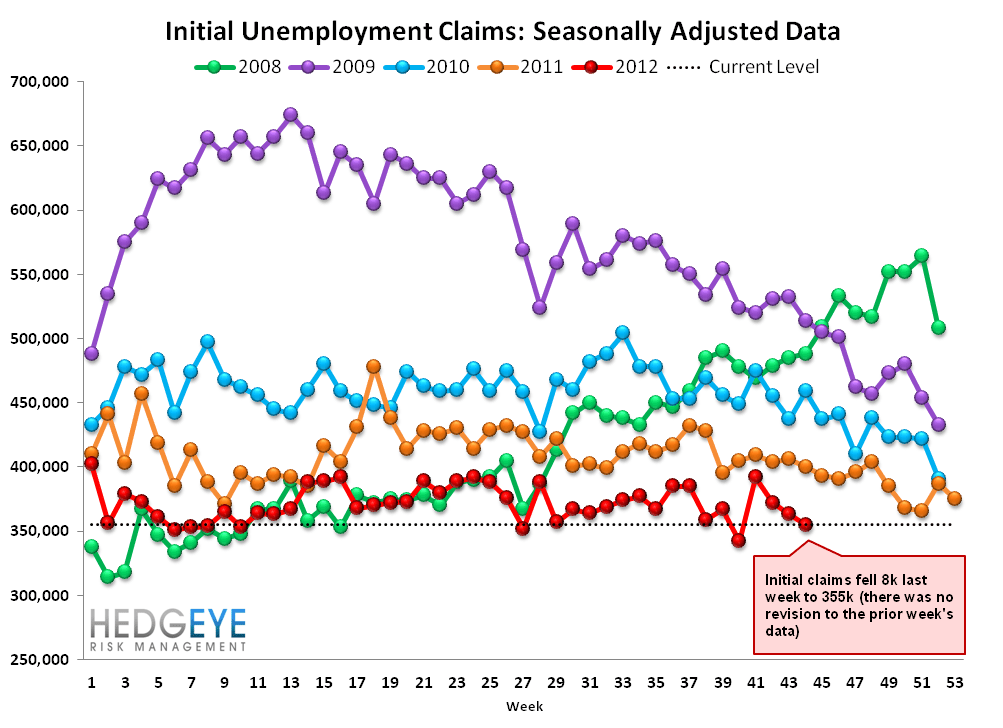

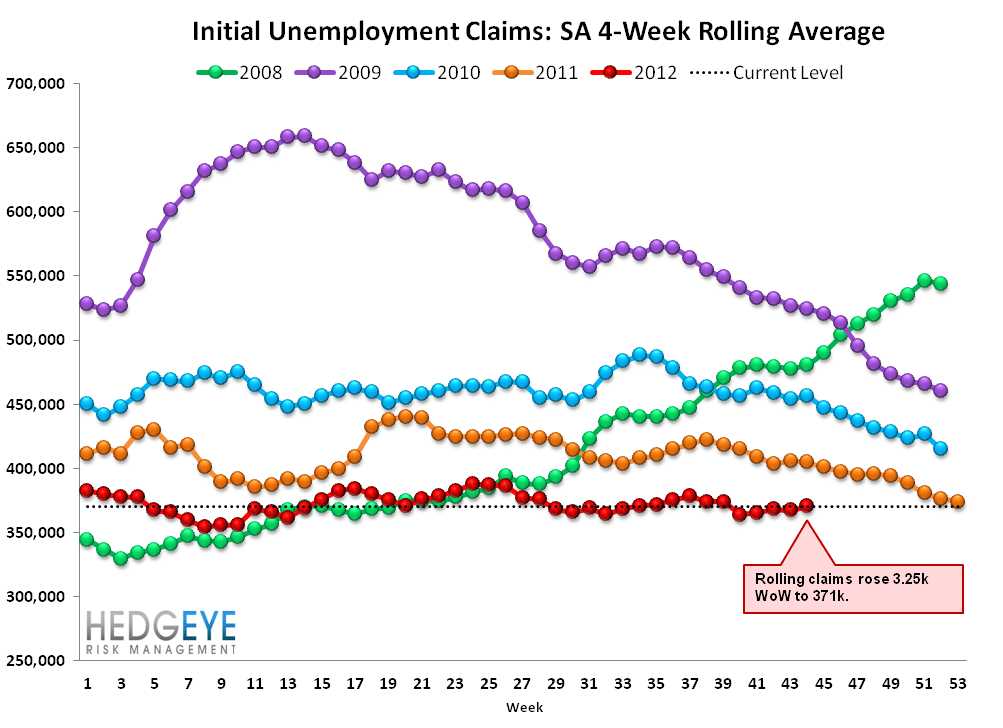

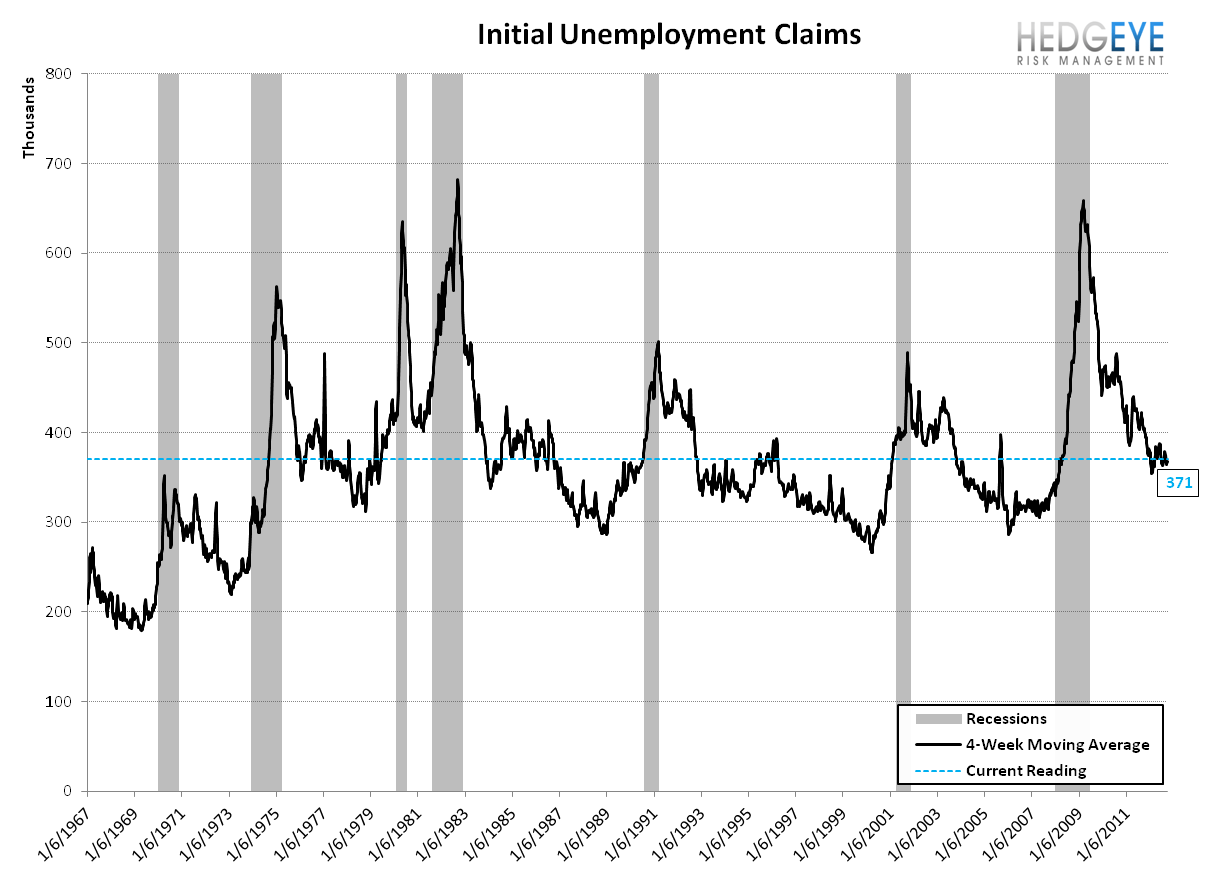

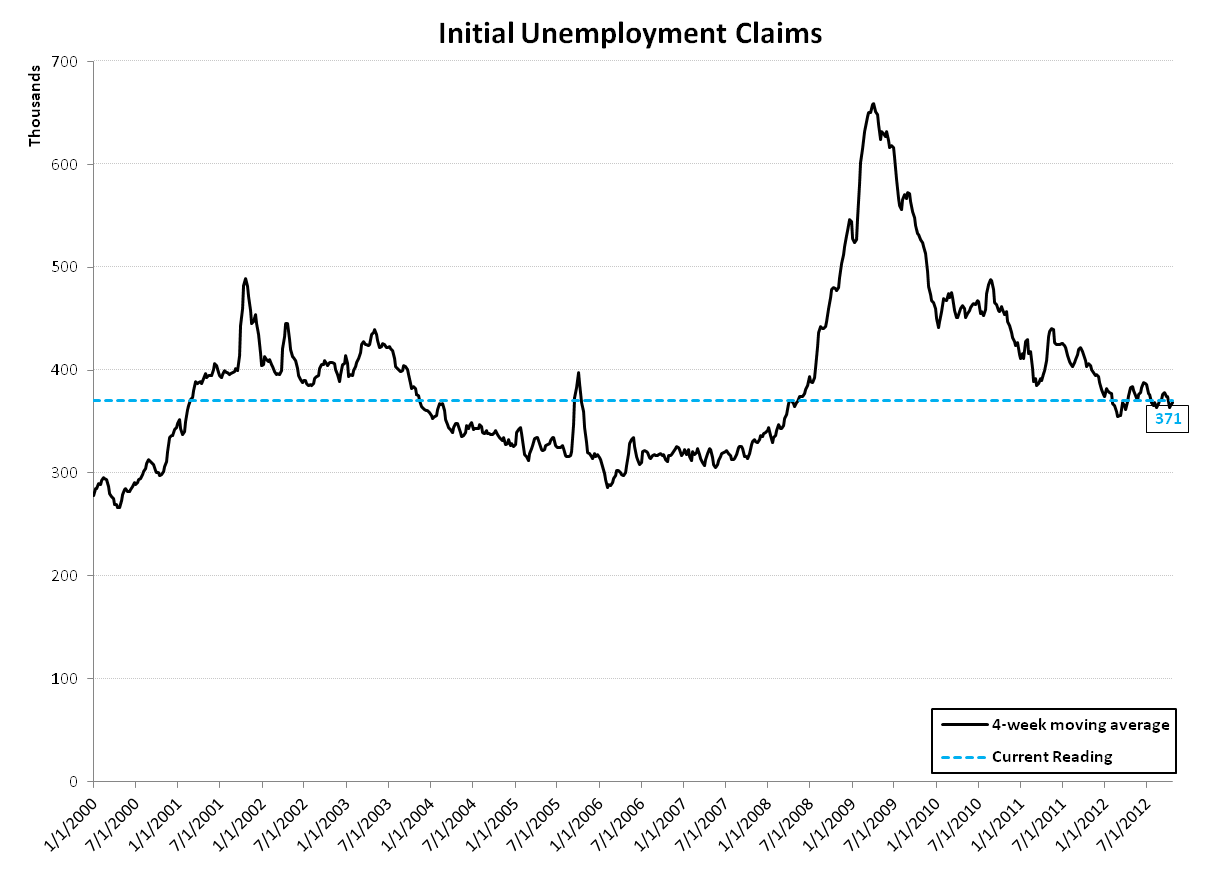

Seasonally-adjusted initial jobless claims fell by 8k last week to 355k. There was no revision to the prior week's data. On a 4-week rolling basis, claims rose 3.25k to 371k. We know that last week's print was affected by Hurricane Sandy, but based on comments from Labor Department officials, we don't know whether the affect was positive or negative. Some states saw an increase in claims because Sandy left them out of work, while in other states there was such widespread damage that it inhibited people's ability to file for new claims.

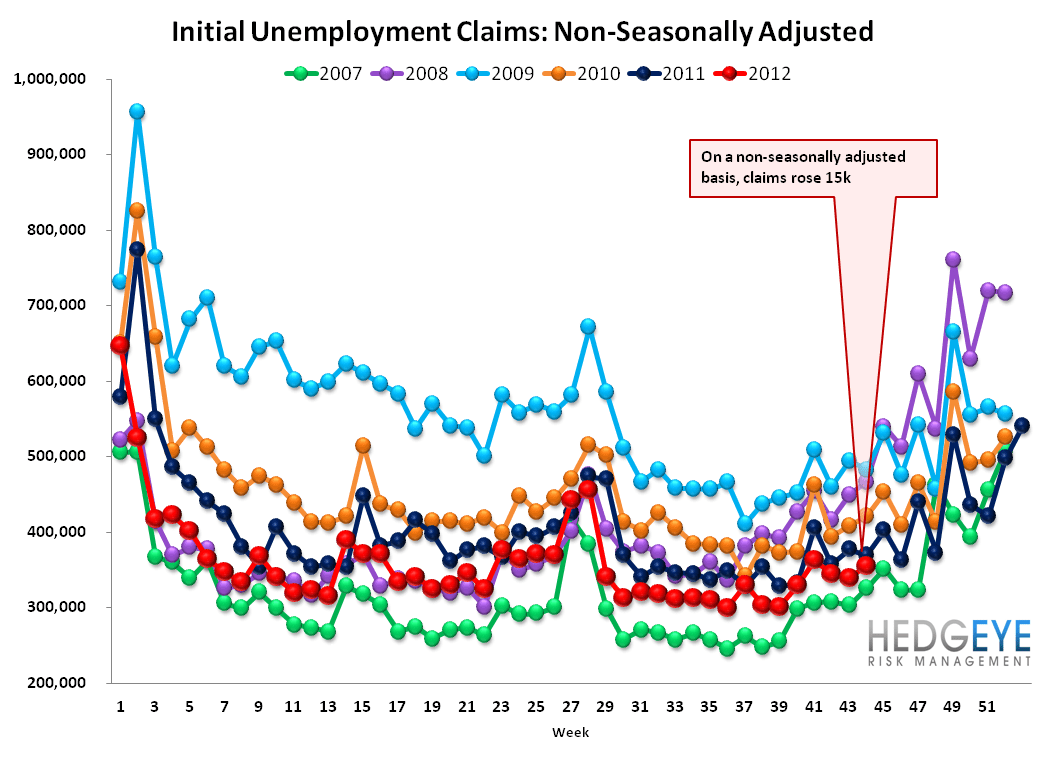

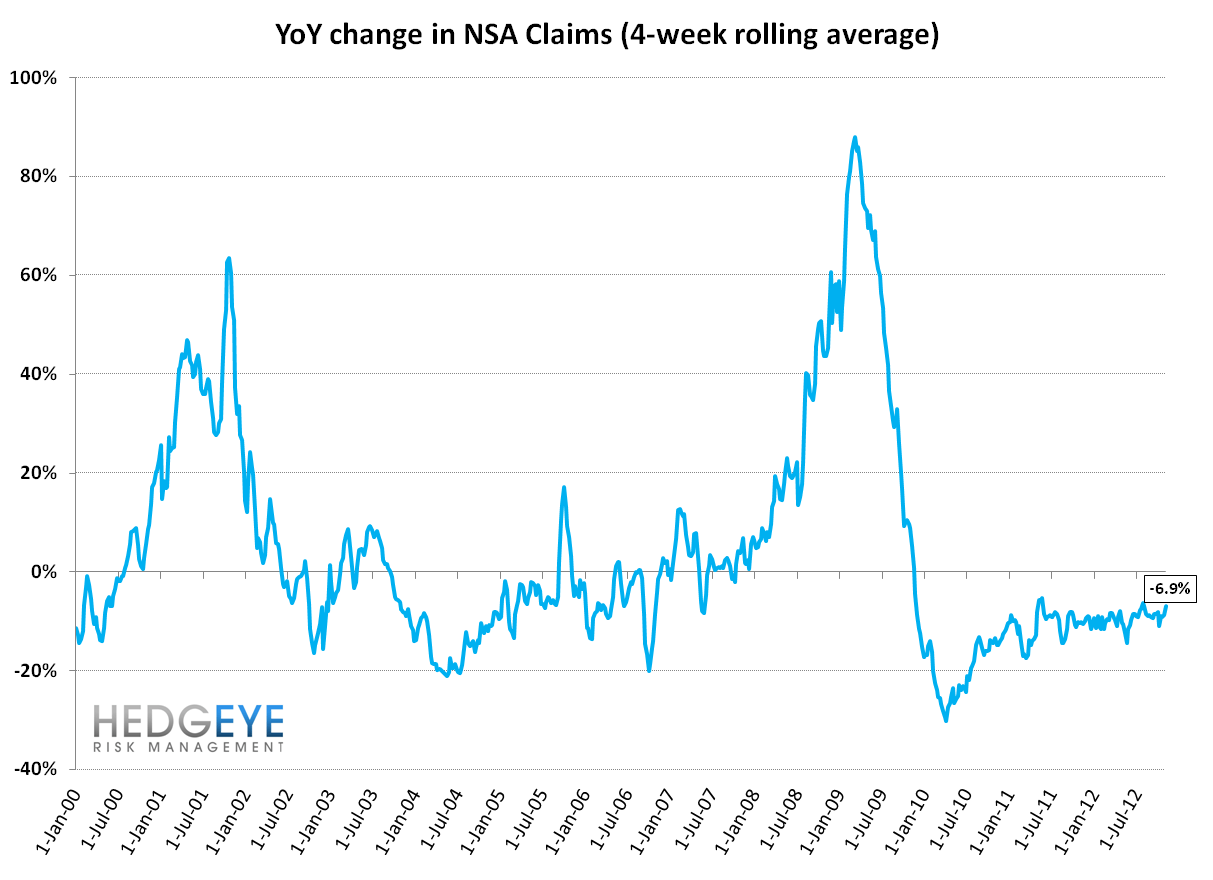

The non-seasonally adjusted data would be subject to the same Sandy distortion. This week's non-seasonally adjusted claims were higher by 15k. We like to look at the YoY change in rolling NSA claims for a more accurate read on the trends. This week that YoY improvement slowed to -6.9% from the prior two readings of -8.8% and -9.1%. This slowdown is worth keeping an eye on, as it may be an early indication that the real labor market is starting to show signs of weakening. However, we would emphasize that the distortions from Sandy have us cautious about putting too much emphasis on the numbers at this time.

On a seasonally-adjusted basis, we expect to see claims continue to benefit from a seasonality tailwind through February, consistent with the last three years. We illustrate these various dynamics in the charts below.

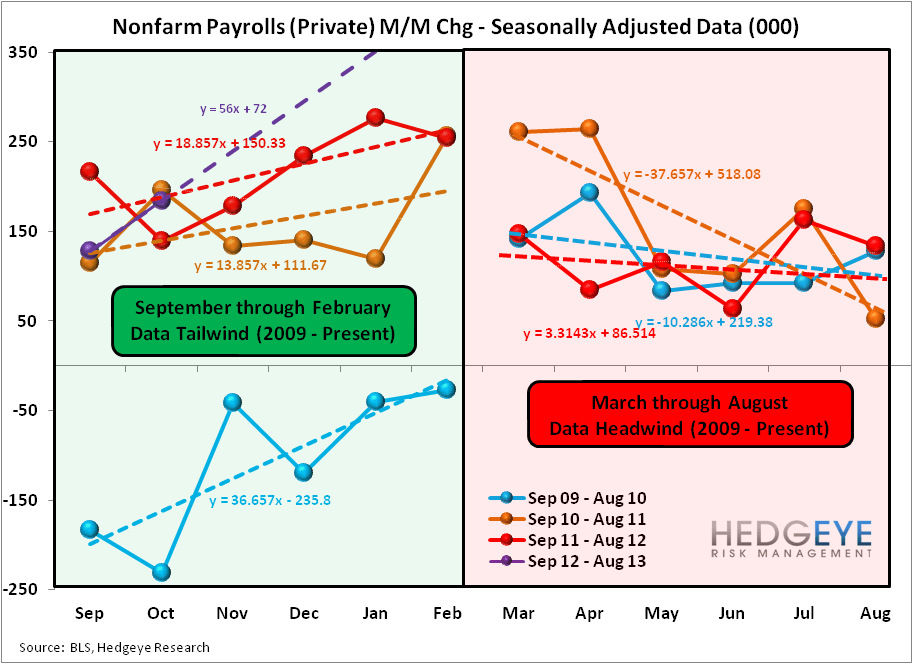

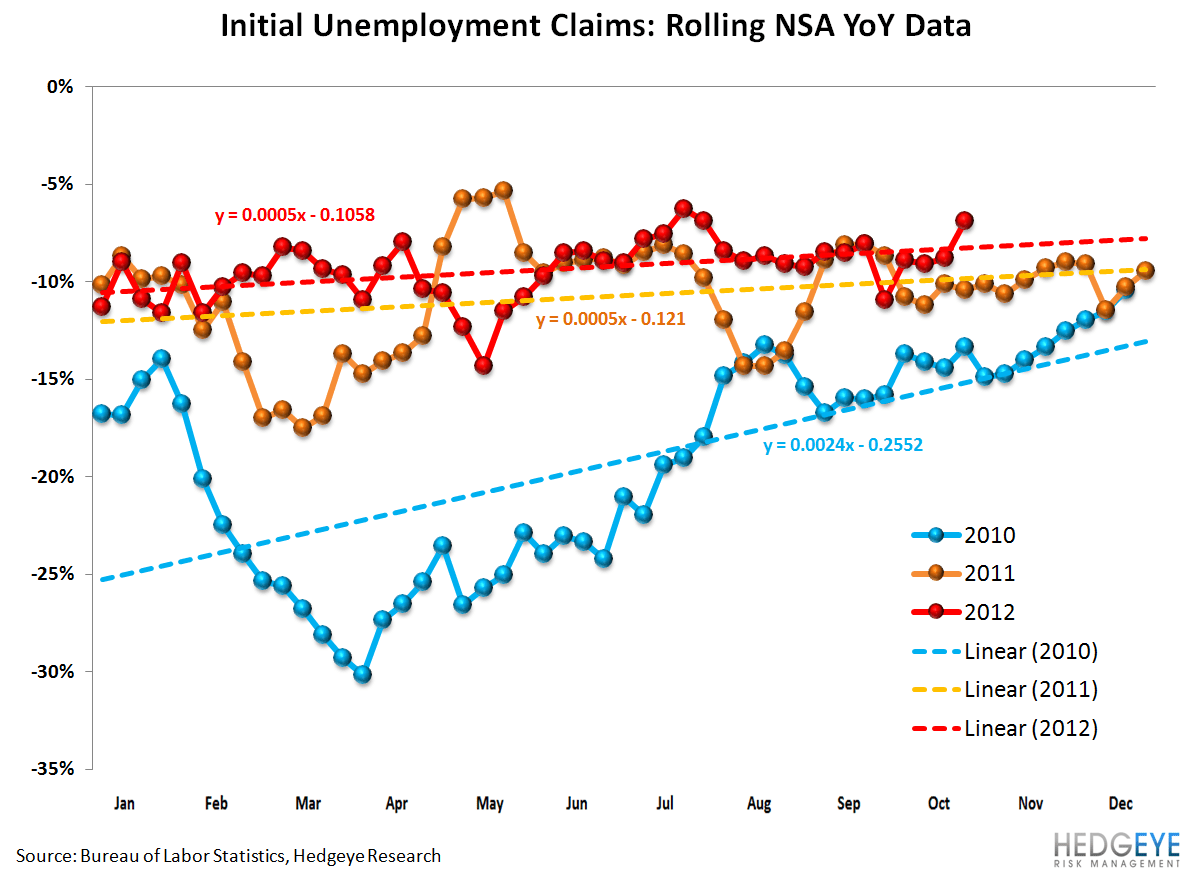

It's also worth briefly noting that strength in last month's non-farm payroll report is a statistical aberration. We note the difference in the slope of this year vs the past three. While it's difficult to forecast any one data month accurately, we would think it quite likely that the November non-farm payroll number is down MoM vs. October.

In the chart below we're profiling the YoY change in rolling NSA initial jobless claims series. Note the similarity of the slope of the trendline from last year vs. this year, and note the upward move of the last data point well above the trendline. While there have been comparable moves earlier this year, they were generally in response to aberrations in the year-earlier data, whereas this week's move is against a relatively normalized baseline.

Yield Spreads

The 2-10 spread fell 4.5 bps WoW to 137 bps. So far 4QTD, the 2-10 spread is averaging 1.45%, which is up 8 bps relative to 3Q12.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over multiple durations.

Joshua Steiner, CFA

Robert Belsky