There are a lot of reasons why we don’t like Macy’s with a 4-handle, and even have a tough time getting excited about it with a 3-handle.

The way we look at it, the best bull case is that even with EBIT down 5% next year (which we think will happen) we still get to earnings being about flat. Due to the debt tender and share repo activity, the financial engineering here rivals what we saw at GPS for much of the past decade. Tack on the potential success of My Macy’s and the Millennial Stores, and we’re looking at yet another year where M comps consistently higher, and add on 100bp leverage in gross margin as a result without commensurate SG&A spend. Add on some financial engineering… and you get to about $4.75 in 2013 earnings – suggesting that the stock is actually trading at 8.5x earnings and 5.5x EBITDA today.

Now comes the very simple bear case. Do you REALLY want to pay 8.5x/5.5x for a department store under the assumption that everything goes absolutely perfect?

This a business that has no square footage growth, no ‘birthright to comp’ in its core, struggles to consistently earn its cost of capital (what happens when lease accounting rules change and M has to account for its property?), and has zero competitive advantage in the core area that will be driving incremental consumer purchases for generations to come – dot.com. Try as they will with ‘The Millennial store’ and My Macy's, but the reality is that as they grow, our kids are unlikely to go en masse to Macy’s to buy their apparel at a rate greater than what we’re doing today. If they do, it will be the result of some considerable capital investment that we have yet to see (or model). Also, let’s not forget the risk that taking down the target age in these new store concepts has to Macy’s existing customer. They’re smarter than most retailers, but we’ve seen some of the best and brightest fire their customers with horrible circumstances.

Other thoughts to consider.

1) Estimates Are Too High. We’re modeling flattish earnings in 2013, the consensus is looking for growth of about 18%.

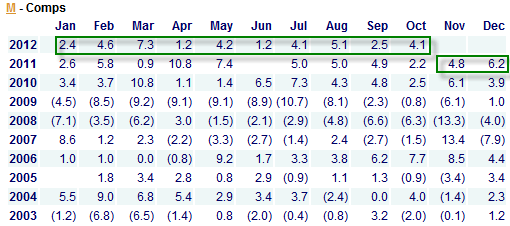

2) Can't Comp Forever. The Street is banking on another 2-3% comp for Macy’s next year. Seriously? Go back into the pages of retail history and find a time when Macy’s comped up 4-years in a row. Have fun with that research. It’ll take a while.

3) JCP Matters Now. Is anyone considering that precisely 1-year ago JC Penney started hemorrhaging revenue, and essentially handed over $3bn in sales to anyone who wanted it? We’ll give Macy’s (and GPS) all the credit in the world…they saw the opportunity, and they took it. But JC Penney is coming on strong. What people don’t get is that even if JCP fails miserably in putting the wrong higher-end brands in front of an audience who could care less, the inventory still needs to be sold…somewhere, somehow. To think that this will not come back to haunt M is being intellectually dishonest.

Macy's Definitely Saw A Lift From The JCP Debacle

4) How big of a deal is JCP? We’re talking roughly $2.8bn over four quarters if our estimates are right. To put that into context, that equates to about 10% of Macy’s sales right there. We’re not saying that Macy’s got it all – or even half (Heck, KSS comped down during this period so we know it wasn’t them). But 2-3% comp points worth? We think so. Macy’s management won’t agree with that assessment, but the reality is that there is no way for them to know why people walk into their stores, or walk right by. One fact that is impossible to argue with is that we are just beginning to start off on a period where Macy’s needs to comp against these share gains -- whatever they are. Let’s say that they are prepared…I can promise you that all of their competitors are not. Desperate competitors equals an unhealthy environment.

5) They'll Get It The Painful Way. In the end, we think that if Macy’s wants the comp, they’ll get the comp. But they’ll need to buy it. And we quote CFO Karen Hoguet…

“We’ve consciously tried to bring more goods into the stores to help us transition to the Spring and have more newness as Christmas approaches and for a post-Christmas strategy. So this is a conscious change from what we’ve done in the past.” Much like we see with JCP, the merchandise will need to be sold.

There were a couple of times during the conference call where we heard statements that encouraged us...

a) It is impressive that over 290 M stores are up and running to support the dot.com business in the same way the a DC would otherwise function. That compares to just over 20 a year ago. Definitely great execution there. We’d note, however, that at some point the dot.com focus will need to be in getting people genuinely excited about shopping on the site. That’s apparent today, but will be harder to keep it up as the business scales off of such small numbers.

b) “White space opportunity with the new model they are creating with Finish Line.” Is it any coincidence that Macy’s is doing more of these shops at the same time JCP is becoming the Shop in Shop poster child? This is likely a winner, but likely has more of an investable impact on FINL than it does on M. On the margin, it is probably a slight negative for FL to the extent that 1) it works and 2) it scales.

c) “We’re trying to see if there are ways of using technology, whether it be through mobile devices or visual or mannequins, digital mannequins and things like that…” Didn’t Ron Johnson say this a year ago? JC Penney is not exactly the beacon of excellence in this industry. These things are cool. But they cost money. It is in line with our view that the cost of growth in this business is going up.

In the end, if our numbers are right, there’s no reason why this stock deserves a double digit multiple on an earnings number that people realize is shrinking. You gotta remember, zero growth retailers have traded at 6x forwarded earnings – several times – and there’s no reason why M can’t test that again. We’ll give the best case earnings of $4.75 a 10x multiple. If you buy today, you’re playing for $7 upside. That’s good, but not when you put a 6x or 7x multiple on an earnings number closer to $3.00. That’s almost 3 to 1 downside/upside for a consensus long at a point when the competitive pressures are going to start coming on strong and M’s revenue base will be assaulted. That sounds dramatic, but we think it’s how you need to contextualize the massive move that JCP is making to kick its merchandise into high gear, and how the competitive landscape will respond.