McDonald’s reports October sales tomorrow morning before the market open. Consensus is calling for a sequential deceleration in two-year average global trends in October. We are expecting US comps to miss already-subdued expectations.

As we have recently written, we expect further negative revisions to McDonald's earnings estimates as several headwinds come into view. Difficult compares in the US for 4Q and 1Q, driven by strong underlying performance and favorable weather, and continuing macro headwinds in Europe, are the primary pillars of the bear case. We are looking for reasons to become more constructive but, as yet, especially given managements tone on the recent 3Q12 earnings call. Global macroeconomic factors are suggesting continuing sluggish conditions and, as we wrote earlier this week, FX headwinds are also set to impair earnings growth in the immediate-to-intermediate term.

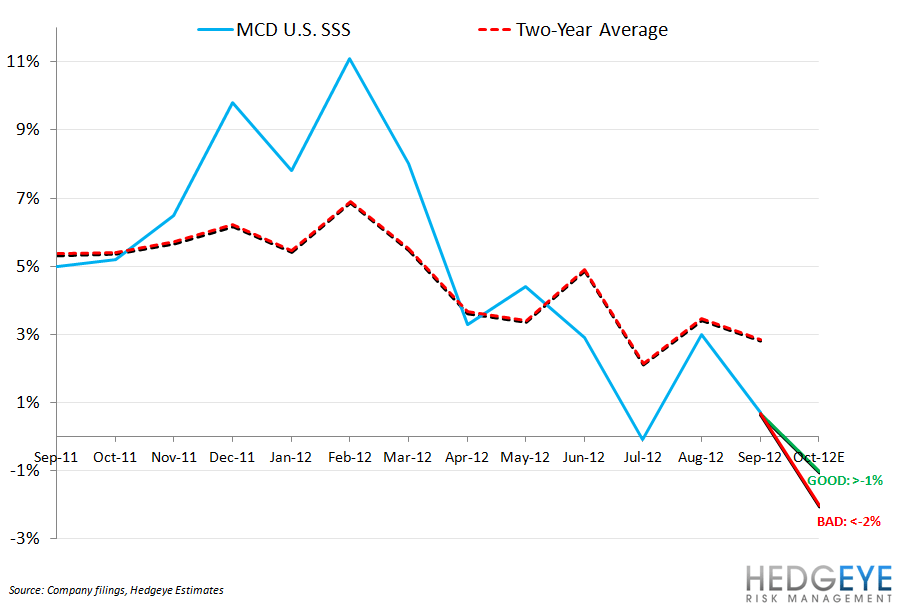

Below we go through what we would view as good, bad, or neutral comparable restaurant sales numbers for McDonald’s three regions in October. For comparison purposes, we have adjusted for historical calendar and trading day impacts (but not weather).

Compared to October 2011, October 2012 had one less Saturday, one less Sunday, one additional Monday, and one additional Tuesday. We expect this to have a positive impact on October’s headline numbers. Our estimate of this impact, on average, is -1.5% during the month of October.

United States – facing a compare of 5.2% including a calendar shift of -1.6% to -0.7%, varying by area of the world:

GOOD: A print above -1% would be received as a strong result as it would offer the best possible clarification of management’s guidance of “negative” global comps in October. While the guidance was not specific to the US, the domestic business is McDonald’s largest division and was likely trending negative at the time management provided the aforementioned guidance. It is also worth noting that guidance was offered before the onset of Hurricane Sandy and all of the resulting disruption in the North East. We are anticipating comps of -1.5% in October.

NEUTRAL: Same-restaurant sales growth between -1% and -2% would be received as neutral by investors as it would imply roughly flat calendar-adjusted same-restaurant sales and traffic growth versus August.

BAD: A headline comp of less than -2% same-restaurant sales growth would be negative for MCD, especially given that the company is taking roughly 2.7% price in the US.

Europe - facing a compare of 4.8% including a calendar shift of -1.6% to -0.7%, varying by area of the world:

GOOD: A same-restaurant sales growth number greater than zero for Europe would be deemed a positive result by investors. October is a sequentially easier compare for the Europe division versus September. We are expecting comps in Europe to come in at roughly -1%.

NEUTRAL: A print of between 0% and -1% would be received as a neutral result for Europe as it would come in close to consensus and would imply only slightly-negative-to-flat calendar-adjusted two-year average trends from September.

BAD: A result of less than -2% would imply two-year average trends, on a calendar-adjusted basis, at the lowest levels of 2012.

APMEA – facing a compare of 6.1% including a calendar shift of -1.6% to -0.7%, varying by area of the world:

GOOD: A result better than -2.5% would be received positively by investors as it would imply sequentially stable-to-improving two-year average trends even as concerns about Chinese economic growth persist.

NEUTRAL: A print between -2.5% and -3.5% would suggest a stabilization in calendar-adjusted two-year average trends within APMEA. Management highlighted the “uneven” recovery in Japan and the Chinese slowdown as negatively impacting sales for the APMEA division as recently as October 19th.

BAD: Same-restaurant sales growth worse than -3.5% would imply trough AMPEA calendar-adjusted two-year average trends in October.

Howard Penney

Managing Director

Rory Green

Analyst