This note was originally published November 07, 2012 at 08:20 in Early Look

“A fool thinks himself to be wise, but a wise man knows himself to be a fool.”

-William Shakespeare

Depending on your political affiliation this morning, last night was either a Shakespearean tragedy or a Shakespearean comedy. Republicans are obviously sad and Democrats are clearly quite happy. But, did anyone really win? The President was re-elected with a very small margin and Congress remains in gridlock with a Republican House and Democratic Senate.

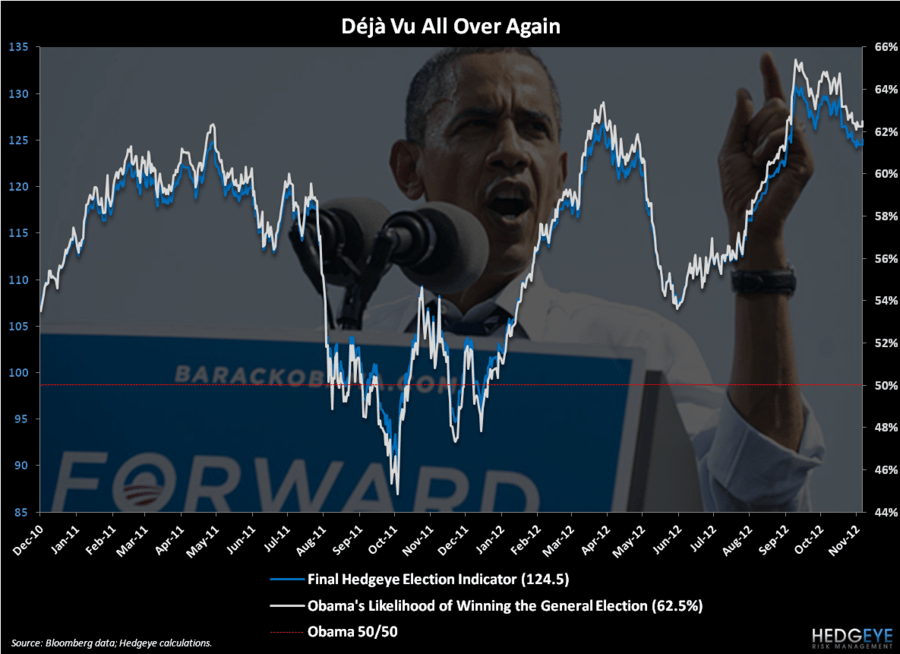

We went into this election launching our Hedgeye Election Indicator (HEI), which attempted to assign a probability to the President getting re-elected based on real time market prices. In our Q4 themes presentation, we then flagged that all the consensus polls were pointing against Romney. The key discrepancies we saw to this consensus were the potential for a relatively higher turnout for Republicans and an economy that, based on historical standards, should not have led to a re-election for the incumbent. In the end, neither Republican turnout nor the economy mattered as much as we expected.

When the political scientists write the story of this election, it will likely come down to a few failures by the Republicans. First, they didn’t make the economic case strongly or clearly enough against Obama. Second, a number of demographic groups turned sharply against the GOP, namely women.

Obama, on the other hand, did a few things very effectively. His re-election team consistently painted Romney as unfit to be President and the characterization largely stuck -- or at least stuck enough to matter on Election Day. More importantly, Obama implemented a number of policies that aided him. Indirectly loose monetary policy aided the stock market and inflated some asset classes, which as we show in the Chart of the Day of the Hedgeye Election Indicator aided his re-election chances. The second key policy was the auto bailout, which mattered disproportionately in the key battleground states.

But now the election is behind us. To the victors go the spoils, or at least the gloating tweets and Facebook status updates, and to the stock market operators comes another day of playing the game in front of us. Some questions to consider as a result of this election are as follows:

1) How will the Fiscal Cliff ultimately play out? The timing on this step up in taxes and step down in government spending is January and no resolution is imminent.

2) Will the Republicans hold the economy hostage over the debt ceiling again? Based on our analysis, the U.S. is slated to hit the debt ceiling again in early 2013. With less of a mandate for Obama, it’s unlikely the Republicans in Congress acquiesce on this.

3) Who will replace Treasury Secretary Tim Geithner? We’ve made our stance clear on Geithner, we aren’t big fans. But based on the proverbial writing on the wall, he is on his way out and who takes his spot is very much an open ended question.

4) What will Obama’s economic policy look like in 2013 and beyond? Regardless of your partisan affiliation, you must admit this was and is a very tepid recovery. Early in his first term, the President will have pressure to do more to stimulate. How will he juxtapose this with the need to cut government spending?

5) Is this Chairman Bernanke’s last term? On some level this is irrelevant in the short term as his term doesn’t end until January 2014, so we should expect to see absurdly loose monetary policy until at least then. As always though, markets will price in a new Fed Chairman before it happens, so determining Bernanke’s replacement will be key to thinking about the future of monetary policy.

We will be digging into these questions and more this morning at 11:00am with Neil Barofsky, the former Inspector General of the Troubled Asset Relief Fund. By his own admission, Barofsky is a life-long Democrat and as a former senior official in the Treasury Department will have some keen insight into the future of policy in the Obama administration.

One of our favorite quotes from Barofsky, who wrote “Bailout: An Inside Account of How Washington Abandoned Main Street While Rescuing Wall Street”, is the following:

“We need to convince those seeking or trying to retain power that they will not get our votes unless and until they commit to meaningful change of our financial system.”

Regardless of the specific policy path, it is hard not to agree with that quote.

In terms of your portfolios, the biggest immediate term factor to focus on is the U.S. dollar. As long as Chairman Bernanke is leading the Federal Reserve, monetary policy will remain implicitly dovish. This is and remains bearish for the U.S. dollar. Conversely, this is positive for those asset classes that are inversely correlated to the dollar. Chief among these is gold, which currently has a high 90-day inverse correlation to the dollar.

Dollar down and commodities up, sound familiar? As Yogi Berra famously said, “It’s déjà vu all over again.” Unfortunately for corporations and the stock markets, dollar down means increased input costs and earnings headwinds.

As my colleague Darius Dale highlighted yesterday, for the 3Q12 earnings season to-date, 59.8% of S&P 500 companies have missed on the top line and 28.7% have missed on the bottom line (388 total). That compares with 57.8% and 26.8%, respectively, in 2Q12. Similar to the political landscape, we would expect more of the same in terms of our Q4 theme of #EarningSlowing.

Our immediate-term risk range for Gold, Oil (Brent), Copper, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1701-1733, $108.46-111.44, $3.46-3.53, $80.24-80.85, $1.27-1.29, 1.67-1.75%, and 1419-1432, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research