Times are changing for Nike (NKE) as the company’s fundamentals begin to change. We believe that sentiment will turn on the margin this quarter. Nike’s stock price has traditionally been linked to growth of global futures but recently, that’s changed as you can see in the chart below. Stock growth is heading higher while Nike heads lower.

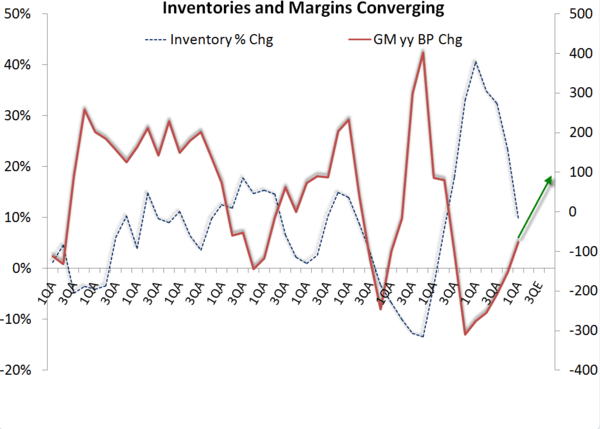

Inventories at Nike are converging with gross margins. The company’s gross margins are expected to head higher in the back half of 2012 and could be positive over the next quarter. There’s a lot of hating on NKE right now, but that could soon change.